Posts in category Value Pickr

Ranvir’s Portfolio (31-05-2024)

Steel Strip Wheels –

Q4 and FY 24 concall highlights –

Total manufacturing capacity –

Steel Wheels – 200 lakh @ 78 pc utilisation. This capacity is slated to expand to 270 lakhs in FY 25

Alloy wheels – 36 lakh @ 82 pc utilisation. This capacity is slated to expand to 48 lakhs in FY 25

No of manufacturing plants – 05

Sales contribution from Steel : Alloy wheels @ 72:28 vs 69:31 in FY 23 ( in value terms )

Domestic PVs mkt share @ 42 pc

MHCV mkt share @ 61 pc

Tractor mkt share @ 42 pc

OTR mkt share @ 70 pc

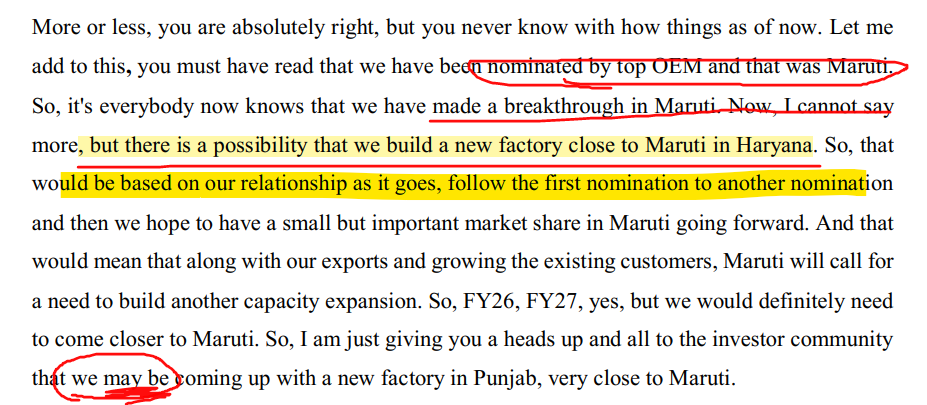

Key models to which company is supplying alloy wheels to include – Creta, Alcazar, Venue, Carnival, Sonnet, Nexon, Punch, Salvia, Astor, Verna, Aura. Company is in talks with Maruti Suzuki for supply of alloy wheels. Supplies may commence by next FY

Export : Domestic revenues breakup

@ 15:85

Export sales grew by 116 pc from 293 to 634 cr in FY 24

Q4 financial outcomes –

Sales – 1069 vs 1005 cr, up 6 pc

EBITDA – 111 vs 108 cr, up 2.5 pc ( margins @ 10.4 vs 10.8 pc )

PAT – 60 vs 47 cr

Alloy wheel volumes @ 8 vs 7 lakh

Steel wheel volumes @ 39 vs 38 lakh

FY 24 financial outcomes –

Sales – 4357 vs 4041 cr, up 8 pc

EBITDA – 465 vs 443 cr, up 5 pc ( margins @ 10.7 vs 11 pc )

PAT – 220 vs 194 cr, up 13 pc ( due lower tax outgo as the company has opted for new tax regime )

Alloy wheel volumes @ 30 vs 28 lakh

Steel wheel volumes @ 160 vs 148 lakh

Long term Debt @ 487 cr. Total Debt @ 1048 cr

( due aggressive incremental Capex and acquisition of AMW autocomponents )

Cash on books @ 31 cr

Completed the acquisition of AMW autocomponents in FY 25 ( they also make steel wheels )

Seeing slowdown in CV sales in Q1 due ongoing elections

Company looking to sell 200 lakh wheels

( alloy + steel ) in FY 25 vs 190 lakh in FY 24. Expecting 10 pc growth in the exports business. Alloy wheels export business doing well. Overall topline growth guidance for FY 25 is also @ 10 pc

Expect to start generating revenues from their Aluminium Knuckles business. SSWL is the first company in India to make Al-Knuckles. It’s an import substitute product. Have signed up with 2 OEMs for supply of these Knuckles ( mainly used in SUVs ). Expecting to do a business of around 35 cr in FY 25, 70 cr in FY 26 and around 140 cr in FY 27 from this segment

Expecting the growth rates to increase in the alloy wheels segment wef FY 25 ( that should be margin accretive )

Company did face a lot of pricing issues wrt their steel wheels business in FY 24. They r in talks with 2 major OEMs for a price revision. They r hopeful of a positive outcome in near future. Also in talks with Maruti-Suzuki for supply of alloy wheels. That may also materialise going forward. These are key positive triggers lined up for the company

The current debt figures are likely to be the peak debt figures. Not planning to take on any additional debt

In FY 25 – growth is mainly gonna come from tractor wheels, exports and alloy wheels business – all these r margin accretive ( vs domestic steel wheels business for PVs + CVs ) – this is likely to have a positive impact on EBITDA margins. Plus there r fair chances of breakthrough on the price negotiations that the company is having with OEMs for domestic steel wheel pricing

Company’s main competitors for exports are based out of Malaysia, Vietnam. However, they do have a higher freight disadvantage vs an Indian manufacturer

Disc: holding, biased, not SEBI registered

Microcap momentum portfolio (31-05-2024)

Here the idea and focus is not on a single stocks, hence there is no search for multibaggers. A portfolio of trending stocks is followed here, and as such, this is a CAGR/XIRR game. And as there are no fundamental checks involved, many stocks hitting stop losses and exiting the PF happens, which may not necessarily the case with individual picks. One can add more when the price falls, there need not be a stop loss as such, in the first place.

Allocation, even if increased to an existing position which has been performing for months, may not add great value by itself, as there will be many other stocks which will have more impact, on both sides.

This is more a process driven, passive approach, practiced over lengthy periods.

Shivalik Bimetal Controls Ltd (SBCL) (31-05-2024)

Can this Bring back the EV Charm and incentives by Govt ?

Shivalik Bimetal Controls Ltd (SBCL) (31-05-2024)

Why is the comapny doing CAPEX in electrical contacts if the space is highly competitive and even after CAPEX they will get a maximum 14% EBIDTA margin as mentioned in Q3FY24 concall

My portfolio updates and investment journey (31-05-2024)

Depreciation increasing means the company is capitalising more assets and they probably haven’t gone to full production (depends on where they are in the go live cycle and industry). Short term it will drag PAT down but long term it has potential to grow topline as utilisation increases. Is it good or bad depends on your time window (short or long), company prospects and many other parameters.

Coal Gasification with Carbon Capture could be a game changer for India-Shifting Coal from an Energy Commodity to a Chemical Feedstock (31-05-2024)

Coal India incorporates new subsidiary for Coal Gasification and Coal-to-Chemical business

The newly formed subsidiary firm, would be known as Bharat Coal Gasification and Chemicals Ltd (BCGCL) for undertaking a coal-to-chemicals business.

Coal India (CIL) holds a majority 51 per cent stake in the new entity while the remaining 49 per cent is owned by BHEL.

Steel Strips Wheels Limited – Attractive Valuations (31-05-2024)

Some keys variables to track –

-

Management guides to improve the EBIDTA per wheel for its steel wheels (bread and butter business as it is called). EBIDTA per steel wheel was Rs 253 per wheel similar to previous year. Steel wheels is 72% of full FY24 revenue. The expectation is see positive side correction on 72% of the business as per the management.

-

Knuckles revenue shall doube from 35 cr to 70 cr and then 4x

-

Co may consider to do a greenfield expansion very to the Maruti plant based on how the relationship with Maruti goes. (REMEMBER- “may consider”)

-

Uno minda is making a greenfield investment in alloy wheels. 1.44 Million capacity per year. Below image from UNO Minda,

-

Guidance of 4800 Rev for FY25 with 0% growth in CV and no revenue contribution from AWM

Narayana Hrudayalaya Ltd (31-05-2024)

Following is the reply I have got from Ishmohit (founder of SOIC). I am enrolled into his course and it has been a fantastic learning experience till now. He has replied beautifully (like always):

- For a hospital to grow, Capex needs to be done. NH is adding 50% additional beds over the next 3 Years in its Capex cycle. Lets look at the industry demand: https://www.business-standard…

India needs an additional 2.4 million (24 lakh) hospital beds to reach the recommended ratio of 3 beds per 1,000 people, fuelling the demand for healthcare-related real estate space, according to Knight Frank. “India’s existing bed-to-population ratio is 1.3/1000 population (both private and public hospitals included), and there is a deficit of 1.7/1000 population. To cater to the existing population, there is an additional requirement of 2.4 million beds,” the consultant said.

-

Thus, there is enough demand.

-

Most important Question, How is NH going to grow?

NH is doing Greenfield Cape’s in same cities such as Bangalore, Kolkata, & Cayman Island. ROCE on existing assets is 25%+. They are going to invest 1650+ crores in FY25. This is needed for Hospital to grow beyond 2-3 years.

In a stable growth industry like Hospitals, there will be cycles of investments and phases of reaping rewards. NH is somewhere in the middle as majority of the investments will break even in 2 years. This is a business which requires FY27-28 type of thought process to compound the money well

Cigniti Technologies – Global Leader in Software Testing (31-05-2024)

Just wanted to understand from community here if there was any special opportunity with the merger with CoForge in terms of valuation difference? Currently it is trading at 1310 and merger is at 1415 following which there will be share swap. Possibly the swap might give an opportunity to enter coforge at a price lower than current market?