Q4 results seem very bad. We may need to check the management commentary.

Posts in category Value Pickr

See the bright Sun: Aditya Vision (31-05-2024)

Valuation seems ok to enter now considering Q1 results going to be very good because of the extreme heat conditions which may have expected to rake in more & more ACs and ancillary appliances in the consumer households.

MTAR Technologies – A wager on innovation meeting economies of scale (31-05-2024)

Even though the co has very small listed history, it has been a growymtg co based on management guidance (for me). The guidance was alwats based on existing order book and ongoing talks with the customers.

Now, for any co, even the management doesn’t have much capability to predict about the deferment of orders. That’s okay the management couldn’t predict and do missed on the guidance

The risk that has played out is the customer concentration risk. If, the customer concentration risk weren’t there, the management wouldn’t have missed the guidance by so much margin.

What could be the way forward

- Bloom evergy coming back with orders and taking deliveries. But, when will this happen

- Revenue from other verticals increasing, which reduces the dependence on single customer. A major risk would be eliminated

- Penalty clause for future orders, contracts. But, I believe the co. doesn’t have enough power for a customer to agree to such deals

Disc: No personal investment currently

Nuvama Wealth Management: Proxy to Affluent India (31-05-2024)

@Mudit.Kushalvardhan @fuzzhead It’s at 50EMA right now. On what bases does it look stage 3 to you? Calling it a stage 3 is way too premature. It’s at stage 2 acc to me.

See the bright Sun: Aditya Vision (31-05-2024)

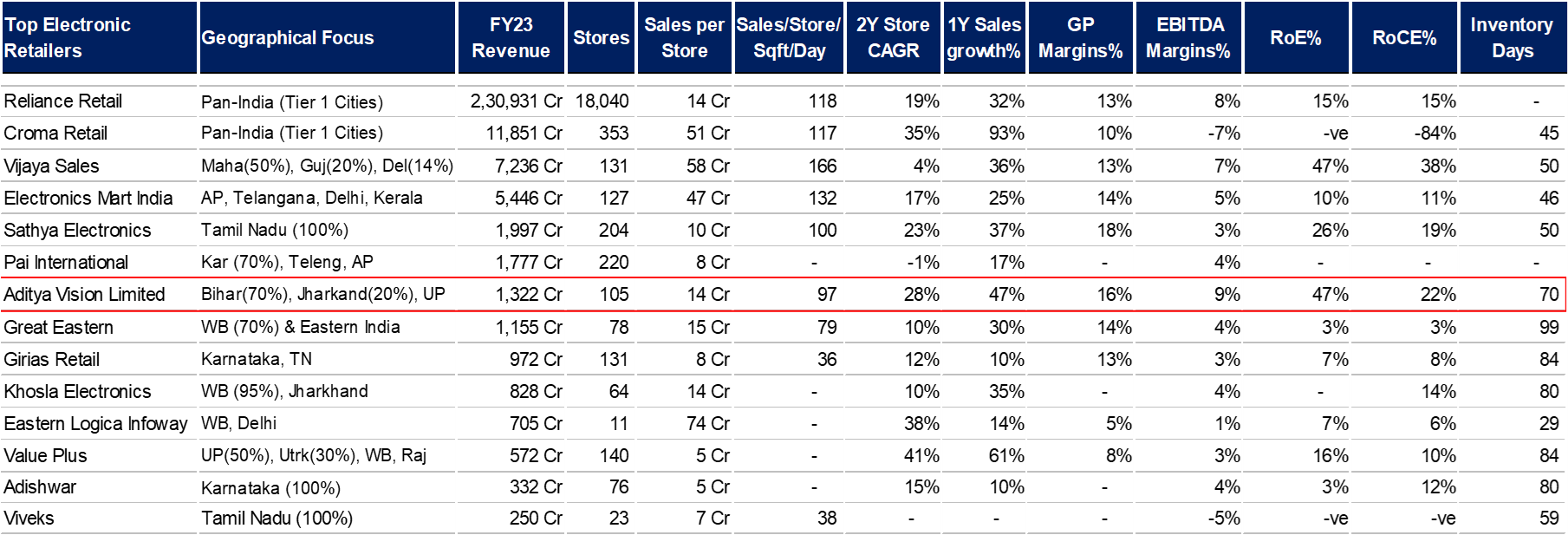

Created a comparison of all electronic retailers:

a) AVL has one of the highest gross margins, which is attributed to volume discounts from OEMs, premium pricing & better product mix

b) Better EBITDA margins are led by lower rentals and labor cost. Rental costs are lower than other retailers, as they are located more in Tier 2/3 cities and prefer opening stores in high streets rather than in malls.

c) Efficient store economics and higher margins translate to a superior RoCE and RoE for the company

d) Store Sales/sqft/day remain low at ~INR 97, compared to peer’s ~INR 115-125, due to aggressive store expansion over the last 3 years. Similarly, inventory days are inflated at 70 days (vs ~40 days in FY18-20)

e) The avg. store size of AVL is 50% smaller compared to its peers, as most of the stores are located in Tier 2/3 cities.

f) AVL generates ~40% of revenues through the financing option (low compared to listed competitor, Electronic Mart, which generates 55%+ of its sales via financing). A store typically pays ~25% of the financing cost (subvention cost).

g) While the giants Reliance Digital & Croma have store only in Tier 1/2 cities like Patna, Gaya, Jamshedpur, Ranchi, etc. both are now focusing on increasing presence in Tier 2/3 cities & have recently opened stores in smaller cities like Vijayapura, Vadodara, Solapur etc. Reliance/Croma aims to add 3,000+/100+ stores each year, majorly in these smaller cities

Jagran prakashan (31-05-2024)

Let’s see. DB Corp has been quite cagey about reporting digital revenues. I suspect the reported profitability of JNM on the digital side, but even if they are profitable, remains to be seen how much more they can scale and monetize going forward. I have my doubts.

Cash on books is good, agree, and yes, I wish it would be valued higher. But the market doesn’t seem to see it that way.

Sandeep Kamath Portfolio | Momentum Investing (31-05-2024)

So the pre-election volatility is all done without inflicting any damage or even changes in the portfolio. Portfolio stays the same but maybe the 1st real test will be the next 2-3 months ( more so if election results are against what the market has priced for )…Lets see.

Portfolio start date → Jan 23, 2024

Total returns → 26.4%

Wealth creation strategy using options with minimum risk (31-05-2024)

Has anyone here any experience dealing with finideas.com? They are a sebi registered investment advisory. Recently, I came across a video where one of their founders explains their strategy to create wealth by buying a long term put option. The strategy is very simple:

They invest your capital into nifty (etf or futures) and buy a long term put option expiring in December. So when the market goes down you make money in your put options which is then reinvested into your existing portfolio consisting of nifty instruments at a low price as the market has gone down. When the market goes up your overall portfolio goes up resulting in a profit. The only time you make a loss is when the market remains flat as you tend to lose the premium you paid for the put. The founder claims the maximum drawdown on the investment is only 4 to 5 percent of your capital which is basically the premium paid. He claims his strategy has given around 19 cagr over the years.

In the video he complicates the strategy a bit by investing 30 percent of the capital into synthetic futures and the rest in bharatbonds to take advantage of the low cost of borrowing in futures. He compensates for the cost of borrowing which is around 5 percent by gaining 7 percent in bharatbonds. So the net profit is 2 percent which helps to reduce the cost associated with the premium of the put option. Here’s the video for reference:

Options से Long-Term Wealth कैसे बनाएं ? Profitable Trading Strategy ! #Face2Face with Govind Jhawar

SKM Egg Products – thinking out of the shell (31-05-2024)

Charts are for SKM Egg products

IDFC First Bank Limited (31-05-2024)

As per bank’s disclosure submitted to exchanges,

After allotment of preferential shares, the book value per share for the period 31 MAR 2024 will increase from 45.49 to 47.36 . An increase of 4.11%.

Effective price to book at today’s price (76.40 / 47.36) = 1.61

This P/B ratio is looking reasonable , assuming 20% -22 % loan growth for the next 5 years and with superb asset quality.