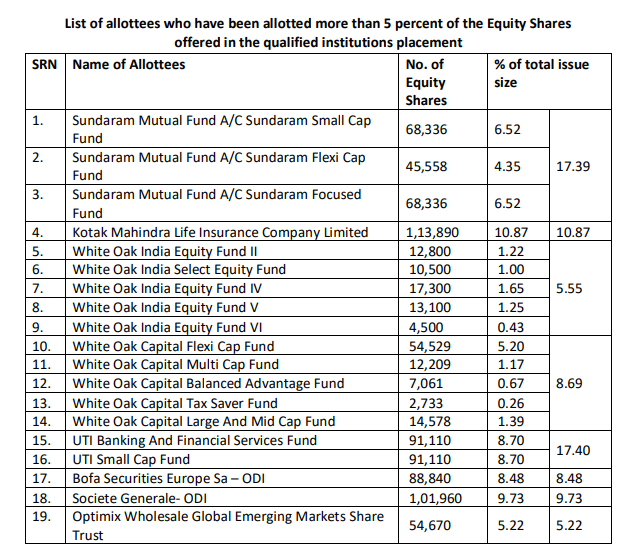

I don’t get your point. Its natural for early investors to exit to matured investors. Arman is following that cycle as it crosses 2000cr AUM. The december QIP showed interest from BoA and SocGen. Are you suggesting they didn’t do their due diligence?