Someone posted their analysis of Uniparts on Twitter:

Posts in category Value Pickr

Tata Steel – Would be merger be of any value? (28-05-2024)

You might have got an allotment letter OR might get one soon about this fractional entitlement.

Usually fractional entitlement shares are clubbed together under a custodian, sold off, and the proceeds distributed among the shareholders based on their fractional entitlement. this might take upto a few months, but contact the company RTA to get exact timelines, etc.

Goodluck India Ltd (28-05-2024)

Q4 FY24 results

Rev up 18%, EBIDTA up 21% YoY

EPS at 11.3 vs 10.3 YoY

Value added products sale volumes increased

by 39% in FY24+Strong demand for critical steel bridge

+VE commentary for Defense+Aerospace arm (New facility progress under schedule)

CFO – (46 Cr) vs 65 Cr

Receivables saw a sharp hike, need to be tracked

FY24 EPS – 46.41 vs 33.31

Saw large volumes today in last 30 minutes. valuations doesn’t look stretched and with demand in future, I feel management is walking the talk.

whats everyone’s opinion on this?

Discloser : having tracking position, not any investment advice.

Tata Steel – Would be merger be of any value? (28-05-2024)

A silly doubt – Some one please clarify. There was a stock merger of Tata steel BSL to Tata Steel in the ratio 15:1 , I held 2000nos of Tata Steel BSL , hence 133.33 nos of Tata steel must be received , however i received 133 nos , what will happen to the fraction 0.33nos?

Tinna rubber – recycling a rubbery growth path (28-05-2024)

Pointers from Tinna Rubber & Infra’s Q4FY24 concall (May 28, 2024)

On capex:

- INR 35-40 crores of capex & process improvement spends expected in FY25

- Debt is being serviced in an efficient manner. Management considers debt as an excellent option for raising funds. Their balance sheet can support it and if needed they will raise debt for any capex requirements as the need arises.

- New plant at Varle can generate INR 75-100 crore topline when operating at full/optimal capacity. The Varle site (it is a 13 acre site viz a viz Chennai which is 5 acres) also has additional space to ramp up operations significantly if needed in the future

- INR 30-35 crores spent on the capex of the Varle plant. The Varle plant can crush passenger car radials which their other plants can’t do.

On growth:

- From a macro standpoint demand for all their product lines remains robust especially the infra sector.

- FY25 guidance is 500 crores (~120 crores a quarter needed to achieve the target).

- FY27 target remains at 900 crores

- 25% cagr growth quoted till FY27 can have a further upside if everything falls in place. More roads are using rubberized asphalt. If the pace of the adoption continues like the last 1-2 years there is a chance they may grow faster than projected.

On margins:

- Setting up a solar plant by Q2FY25 to save energy costs. INR 1.25 crores to be saved annually once the plant is up and running.

- Red Sea impact costs (~10% increase) being passed on to their consumers. Figuring out other ways to hedge against the cost increase.

- Margins have improved due to multiple things like, dealing with better customers – ones that value better service and delivery, better product mix and product lines and operational efficiency.

Other pointers:

- Exports as a % of revenue was 8% in FY24 (INR 24 crores)

- EPR gains first reflect in the topline and then it flows down to PBT. EPR generated for FY23 (~50,000 – 75,000 credits) resulted in sales of INR 6.6 crores in FY24. EPR for FY23 was not entirely sold. The sale that has been made is a direct sale to an OEM manufacturing tyres

- EPR for FY24 is still to be received by the company.

- Oman facility is operating at 80-85% capacity. Not much growth expected here and the business is more for generating cash flows. They may expand to other countries too if good opportunities come up

- 75-80% capacity utilization of plants for FY24

Disc: Invested as a tactical 3-year bet. The recent run up in the stock has made it a decent sized bet in my pf. Will continue to hold as the management has been executing very well.

IPO Review – Discussion until listing (28-05-2024)

Beacon Trusteeship Limited (Mumbai, Maharashtra) is a leading SEBI Registered Debenture Trustee offering technology-enable Solutions. Company provides wide range of services such as Debenture Trustee Services, Security Trustee Services, Trustee to Alternate Investment Fund (AIF), Trustee to ESOP, Securitization Trustee, Bond Trusteeship Services, Escrow Services etc.

Tune in to watch the interview with the top management of the company:

Beacon Trusteeship – Exclusive discussion with the top management | SMEmitra

Arman Financial Services Ltd (28-05-2024)

Just check the history why this PE funds not holding their stake , why they r playing the rotation game.

1St why incofin sold it’s holding when they knows everything, better than any of us.

Correct me if I am wrong but my clear perception says now it’s purely aaja fasaja scheme from both PEs side and promotors side.

I already warned about the basic principals of business…

Disc.sold earlier.

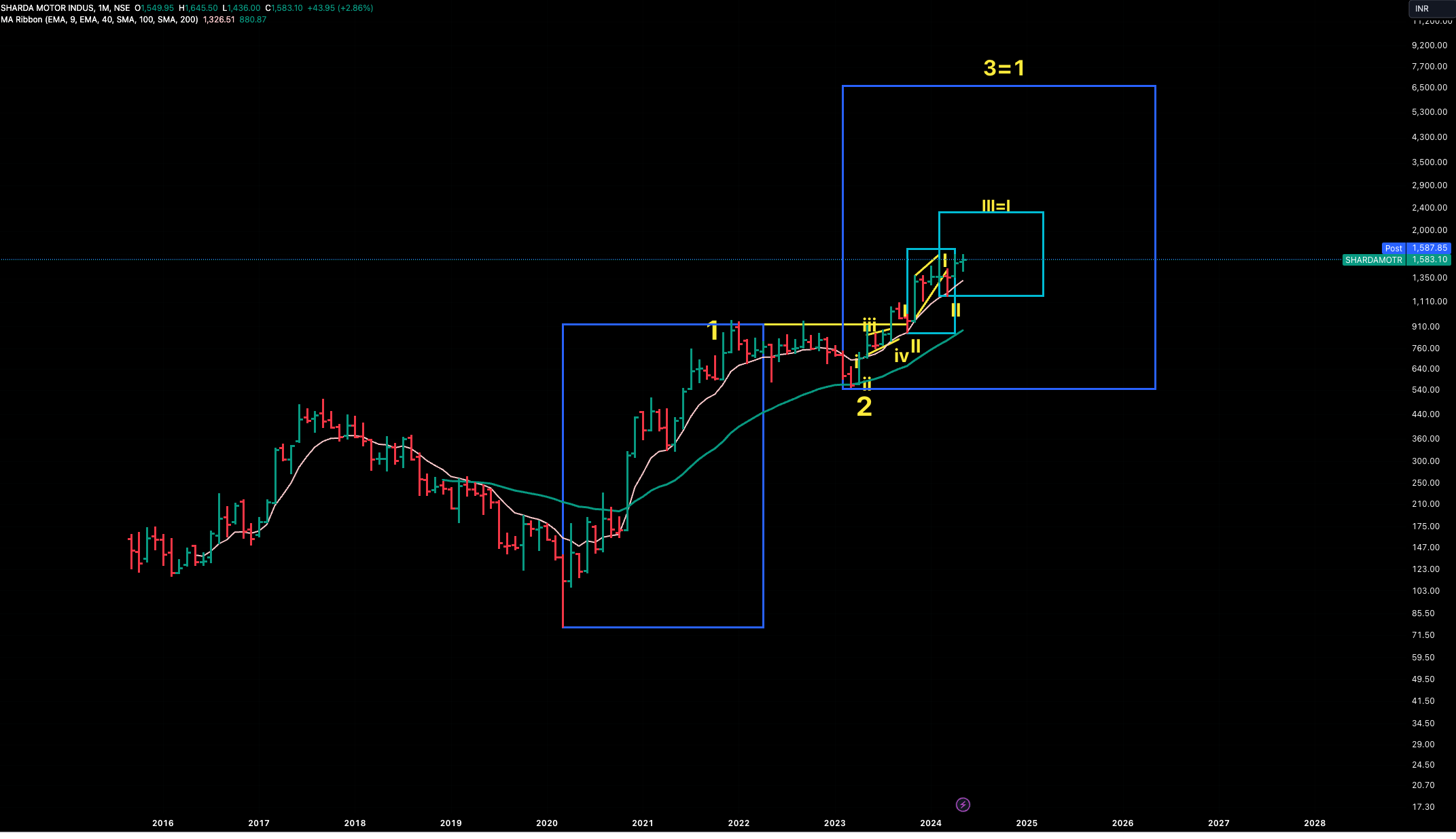

StageInvesting +Elliot Waves (28-05-2024)

Sharda Motors

CMP 1583

We’re big fan of @phreakv6 . Tried to do wave count on Sharda Motors as he has posted about it few months back.

Here is the long term chart , Keep in consideration that monthly charts take months to play out.

Disclaimer : Views are personal. No buy/sell recommendations. The projection is based on our technical -probability study methods and chances of success/failure depend upon various factors.

Godawari Power – Any Trackers? (28-05-2024)

Somehow the no’s of LLoyds seems not comfortable, the CFO/EBITDA seems very high and atlease from screener, they are not paying any direct taxes. not sure why

Megatherm – Mega Opportunity (28-05-2024)

Q4FY24

YoY

Revenue +18%

Net profit +87%

HoH

Revenue +8%

Net profit +55%

Expected better revenue growth but the bump in Profits/OPM made up for it.

https://nsearchives.nseindia.com/corporate/FINANCIALRESULTS202324_28052024132456.pdf