am completely agree with you. I exited too

Posts in category Value Pickr

Microcap momentum portfolio (25-05-2024)

@visuarchie My list exactly matches to this. How to calculate EMA as the excel file had DMA formula. Should i change this formula?

Also when i am creating the first order (Monday 28th May) can i include the ones which is newly entered or should i stick to the list mentioned above (the ones which is still under Top 30)

Galaxy Bearings (25-05-2024)

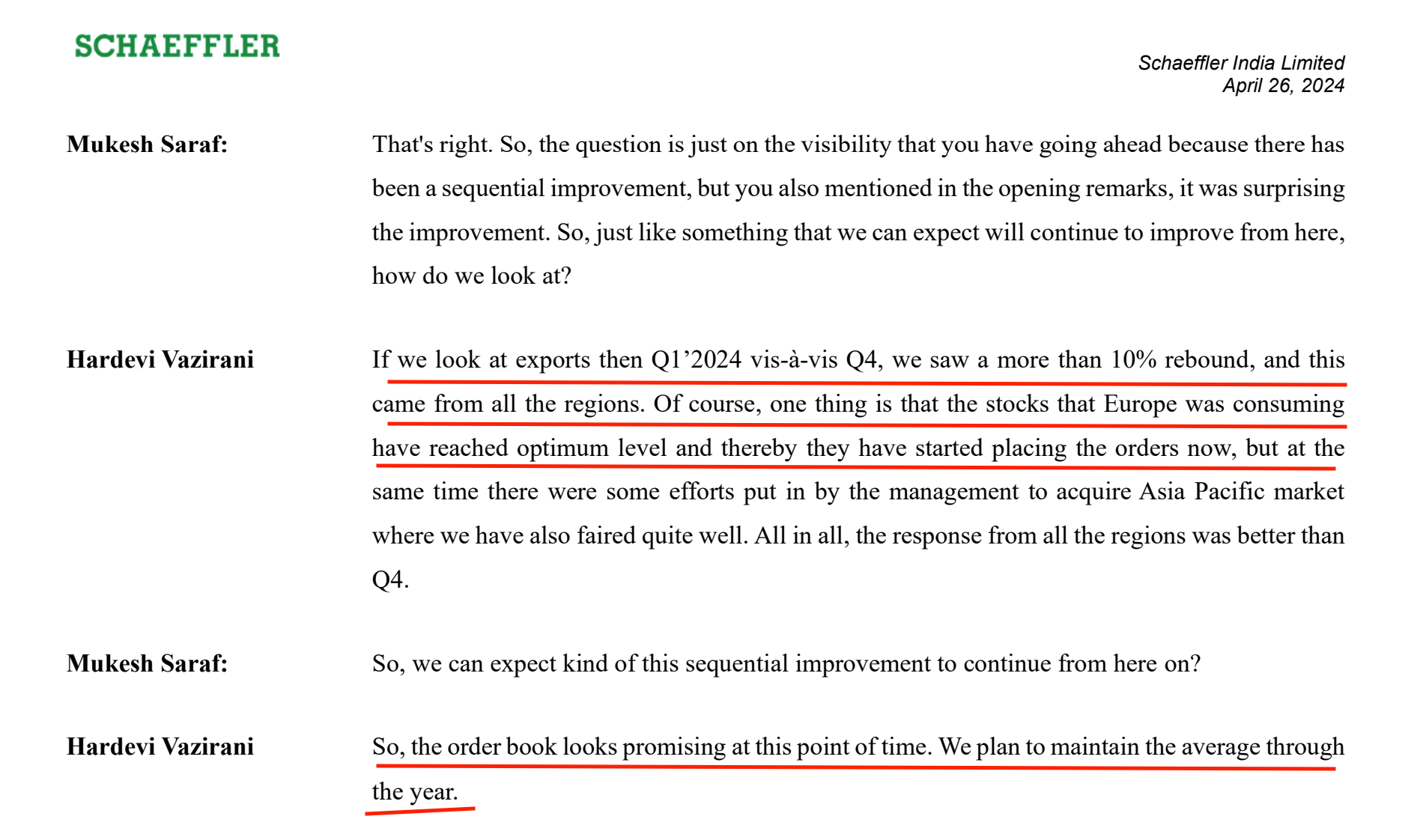

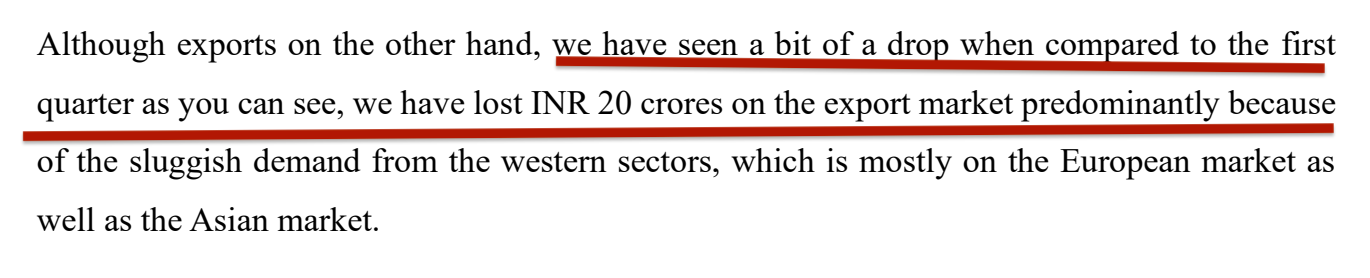

Schaeffler India Ltd saw dip in exports on YoY basis though did witness QoQ growth. Seems, uptick driven by low channel inventory and improvement in the industrial segment. Do note than Schaeffler’s FY is same as CY i.e. Jan – Mar is Q1FY24 rather than Q4FY24.

My portfolio updates and investment journey (25-05-2024)

Hello I was reviewing payment banks and got interested in fino play and digispice. Can you give your rationale of choosing fino play over other similar companies? Thanks.

Smallcap momentum portfolio (25-05-2024)

@stuti_agarwal I have talked about the rules I follow previously also.

-

Yes, the X amount that is available from exits is evenly distributed across the new entrants.

-

I do not make any changes to the stocks that are continuing from the previous week.

Every now and then, I make a lumpsum investment. At that time, my goal is to ensure equal weightage for all stocks in the pf. I distribute the amount across all stocks so that I have equal amounts in all.

Galaxy Bearings (25-05-2024)

Further deep dive into Orbit Bearing’s numbers: Managerial Remuneration is 22 Cr which means we’re talking about an opportunity in a 27% PBT Industry.

They did a gross margin of 42% (FY23) and a pre tax RoCE of 20.30% (FY23) and 26.20% (FY22) – post managerial remuneration.

Cash Conversion Cycle seems to be 298 days for FY23 – which is what’s dragging RoCEs down despite such high margins.

Property Plant and Equipment was only 89 Cr in FY23 which means they have fixed asset turns of over 7x.

This is similar to Galaxy’s numbers where on a gross block of 20 Cr they do a revenue of 127 Cr.

Not to get ahead of ourselves but assuming a Fixed Asset Turn of even 5x (assuming land is more expensive now) – they should be able to add another 175 Cr of business with Phase 1 of this CAPEX. If we go by the capacity they’ve added, it should take them closer to Orbit Bearing’s numbers (who has a capacity of 10 Million).

Zen technologies – A micro cap in the defense space! (25-05-2024)

Management clearly stated that risk in q3/q2 concall…

Shilpa Medicare -Racing away on the Oncology API highway! (25-05-2024)

For Q4 FY24, Shilpa Medicare:dna:![]() reported the following consolidated financial results:

reported the following consolidated financial results:![]()

![]()

Net profit was 245 million rupees, compared to a loss of 81 million rupees year-over-year (YoY). Revenue increased to 2.92 billion rupees, up from 2.64 billion rupees YoY. EBITDA rose to 699.2 million rupees from 370.2 million rupees YoY, with an EBITDA margin of 23.97% ![]()

![]() , up from 14.05% YoY. The company had an exceptional item of a 61.3 million rupee loss.

, up from 14.05% YoY. The company had an exceptional item of a 61.3 million rupee loss.

Shilpa Medicare has achieved significant financial improvement, transitioning from a net loss to a net profit, with notable increases in revenue and EBITDA.![]() Seems to be a turnaround candidate getting ready within next 2-4 quarters. Company sitting on a huge operating leverage it can start kicking in numbers after 2-3 quarters anytime. Keep an eye on this. I guess this is the sixth consecutive quarter where the numbers have been improved.

Seems to be a turnaround candidate getting ready within next 2-4 quarters. Company sitting on a huge operating leverage it can start kicking in numbers after 2-3 quarters anytime. Keep an eye on this. I guess this is the sixth consecutive quarter where the numbers have been improved.

Pharma || Hospitals || Diagnostics : Industry perspective (25-05-2024)

Alembic Pharma –

Q4 and FY 24 concall and results highlights –

Q4 outcomes –

Revenues – 1517 vs 1406 cr, up 8 pc

EBITDA – 260 vs 204 cr ( up 29 pc, margins @ 17 vs 14 pc )

PAT – 178 vs 153 cr, up 17 pc

FY 24 outcomes –

Revenues – 6229 vs 5653 cr

EBITDA – 932 vs 682 cr ( margins @ 15 vs 12 pc YoY )

PAT – 616 vs 342 cr

FY 24 Sales breakup –

India branded – 35 pc – 2200 cr ( includes the Veterinary business ) – grew by 7 pc in FY 24

US generics – 28 pc – 1730 cr – grew by 10 pc in FY 24

RoW formulations – 17 pc – 1052 cr – grew by 23 pc in FY 24

APIs – 20 pc – 1246 cr – grew by 7 pc in FY 24

India business –

Has grown at 11.4 pc CAGR for last 4 yrs

15 pc is under NLEM

Company’s 4 brands have sales > 100 cr

Total MRs @ 5000 +

16 pc of India sales come from Veterinary segment and 30 pc from acute therapies

Alembic is 18th largest Pharma company in India

Veterinary business ( operating in livestock and poultry segment ) has grown at a CAGR of 25 pc for last 4 yrs – now @ 355 cr / yr

US business –

7 products launched in FY 24 taking the total products launched to 147

25+ product launches planned in FY 25

No major Capex planned in next few yrs

Company’s base US business is about $ 200 million. Aiming to build up on this base

RoW business –

Has grown @ 21 pc CAGR for last 4 yrs

Company exports to – Europe, Canada, Australia,Brazil and South Africa

Currently ramping up operations in Chile, Middle East

APIs –

Supplying APIs to 60+ countries globally

( however, main focus is on regulated markets )

Has grown @ 15 pc CAGR for last 4 yrs

Future capacity expansion is on track

R&D expenses for FY 24 @ 480 cr @ 7.6 pc of sales

Current manufacturing base –

5 facilities – Formulations

2 facilities – APIs

Gross Debt now at 430 cr vs 620 cr on 31 Mar 23. Cash on books @ 120 cr

Company’s domestic business growth was mainly led by – gynae, veterinary, opthal, metabolic, GI, Cardio segments

Growth in anti-infectives, respiratory were tepid in the domestic mkts – pulling down overall domestic growth for the company

Expecting good ramp up and operational efficiencies to kick in for the US business in FY 25

Expecting strong growth momentum to continue for RoW business ( ie > 20 pc growth or thereabouts )

Confident of outgrowing the IPM for FY 25

Capex plan for FY 25 @ 300 cr or so – mainly towards de-bottlenecking and maintenance

As US business ramps up, company level EBITDA margins may to go 20 pc kind of levels due better utilisation of facilities ( provided there is no steep price erosions in US )

Disc : looking for dips in the stock price to start accumulating, biased, not SEBI registered, not a buy/sell recommendation