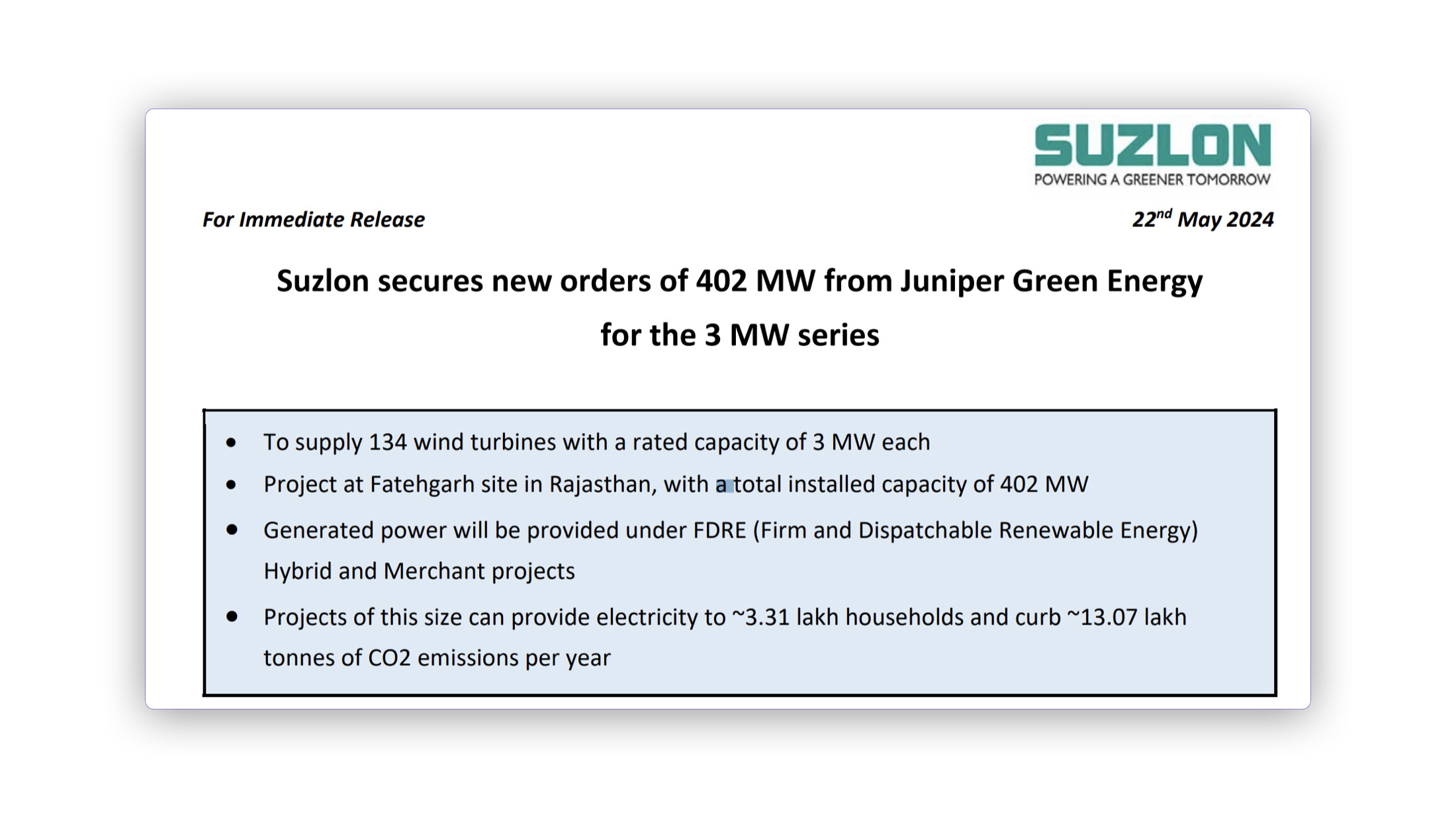

Another Large Order. Can’t wait for them to actually Execute these orders ![]()

Unlike in the past where they’ve stated by when the order is to be executed, there is no mention of the timelines in this press release. No Wonder.

Another Large Order. Can’t wait for them to actually Execute these orders ![]()

Unlike in the past where they’ve stated by when the order is to be executed, there is no mention of the timelines in this press release. No Wonder.

Summary of presentation – slide 9:

Going forward, in the first few months of FY25, muted growth is anticipated due to the general election and upcoming monsoon season. At the current juncture, 15-20% revenue growth expected for FY 25

Link: FY24 presentation

As per PPT – https://www.bseindia.com/xml-data/corpfiling/AttachLive/f0ce5213-df5c-4d98-a57e-6c840b6364ab.pdf

Slide 17 – targeting to achieve ~15% revenue growth with sustained improvement in profits.

On congervative if we consider 15% revenue growth with same profit margin of 22%, EPS of FY 25 is 127.6, with that EPS forward PE comes to 28. Seems cheap with PI quality.

Disc: Invested and views are biased.

Decent set of numbers from PI given the inventory build up and competition coming in key products. In the investor presentation, management has guided 15% growth, reducing from 18-20% being mentioned earlier. Looks like there will be slower growth for the next few quarters, need to wait for the con call tomorrow to get further details.

disc- invested and remains one of my top 3 holdings

ESOP Filing Company has Employee Stock Options (“Options”) plan with a exercise price of Rs.1450/share, 1/3rd vesting every year. Interesting to see which level of employees this is being offered to. My understanding is that Employees will find this interesting/profitable if the price remains above (hopefully significantly) Rs.1450 (during each exercise period i.e. May 2025/26/27), since they have to pay the exercise price.

Maybe a indicator of mgmt expectation of company performance (indirectly translating to stock price) in coming years.

Link : ESOP Announcement

Hello everyone,

I am also interested in joining the group. I have recently started and hoping to connect and learn from fellow value investors

Key takeaways from Q4FY24 Concall from own notes and screener:

Financial Performance:

Operational Efficiency and Cost Optimization:

Capex and Investments:

Business Trends and Outlook:

Customer and Industry Dynamics:

Biosecure Act and Industry Changes:

The concall was led by Saharsh and Sucheth (sons of the founder). After attending the last few concalls, I have noted that they are smart, realistic and down-to-earth management. They paint a very realistic picture of the future growth of the company and are very honest about what the company can and cannot do. They stayed away from speculation (especially around the Biosecure Act) and gave very practical answers based on their internal research and company’s expectations

Disc: Invested since much lower levels and plan to hold due to honesty and integrity of management.

Any one tracking konstelec Engineers?

Agree with you completely. It’s a very good bet on the Indian space.

One doubt though, how do you evaluate the Indonesian business and its scope in the future? It’s clearly the one that’s dragging the business down. Its revival can lead to RBA finally breaking out

First, Haldiram was in talks to acquire the majority stake, then Bikaji and then rumours about ITC being in talks for 47% stake purchase but company clarified it was never in talks with ITC. For Haldiram and Bikaji, as it turns out, the valuation didn’t come through. Can anyone tracking for longer time give any more insights?