Good results from WIL:

https://nsearchives.nseindia.com/corporate/WHEELS_20052024144420_WILReg30PressrelaseMay2024.pdf

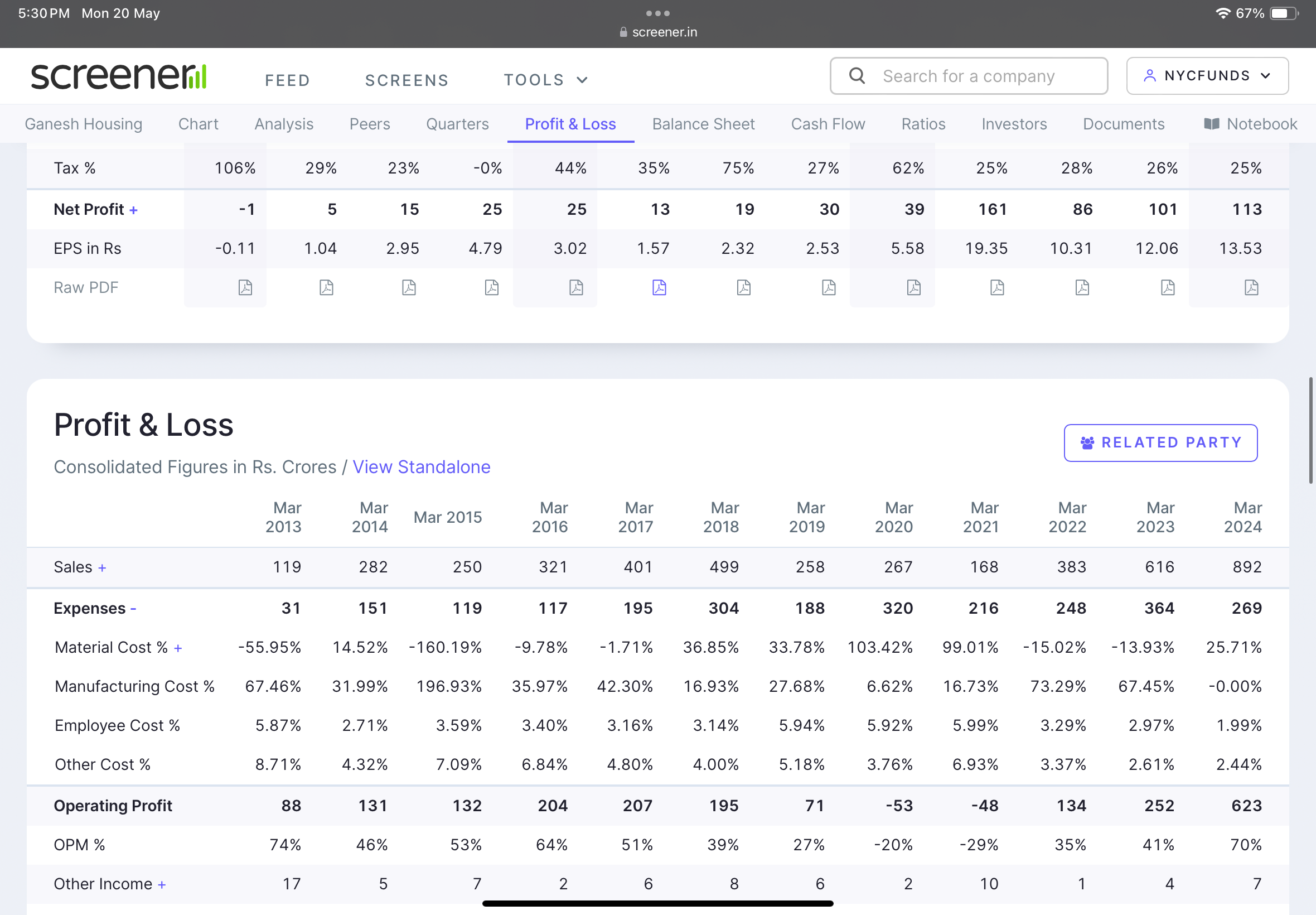

How can material cost be negative. It’s a real estate company

How can material cost be negative. Can someone please help

Hey @visuarchie How do you create a basket order, i am thinking of starting this tomorrow, with an initial investment, and I will be using angel one. Can you guide me through this?

During the quarter, the National Company Law Tribunal (NCLT) sanctioned the scheme of

amalgamation with Veeral Additives Private Limited (VAPL) into Vinati Organics with effect from 1st April 2021 and accordingly the comparative financial result and other financial information for the quarter, year till date, and year ending March 2023 has been restated taking into account the full effect of the merger.On a QoQ basis, the revenue from operations grew by 23% and net profit grew by 30% QoQ to ₹104 crore.

In FY24, the EBITDA declined by 18% YoY to ₹509 crore as compared to ₹620 crore in FY23.

On a QoQ basis, the company witnessed volume recovery in ATBS (2-Acrylamido 2-Methylapropane Sulphonic Acid) and butyl phenols. The ATBS sales are now normalized and de-stocking is over.

In FY24, the revenue contribution from ATBS was ~32%. The sales were down compared to last

year.The company’s global market share in ATBS remained unchanged at 60%-65%.

In FY24, the revenue from butyl phenols business was ~₹300 crore. The company witnessed good growth in this business and it was a major contributor to the revenue during the year.

During the year, the capacity utilization of butyl phenols was ~65%-70%.

The performance of Iso Butyl Benzene, Iso Butylen, and other customized products remained flattish YoY.

Over the last four years, the basket of customized products doubled in revenue to ~₹150 crore. The company expects good growth in the coming years as well.

In FY24, the revenue from the antioxidants (AO) business was ~₹130 crore. The demand for antioxidants is still going through a weak period. The company anticipates scaling up of antioxidants sales in FY25.

During the year, the capacity utilization of antioxidants was ~25%. The company expects to touch a 50% utilization level this year.

The research and development (R&D) department is also working on adding more antioxidants to its product portfolio and the long-term outlook of antioxidants remained positive.

In FY24, the company incurred capital expenditure of ~₹360 crore. Some part of the capital expenditure was incurred towards Vinati Organics for capacity expansion & addition of some new products and the balance was constituted for its subsidiary company Veeral Organics Private Limited (VOPL).

Veeral Organics Private Limited (VOPL) is a 100% owned subsidiary of Vinati Organics Limited for manufacturing niche specialty chemicals. The total capital expenditure in VOPL will be ~₹500 crores mainly consisting of anisole, MEHQ (Monomethyl ether of hydroquinone), Guaiacol, 4-Methoxyethyl phenol, and a couple of Iso Amylene derivatives. These products are used in polymerization inhibitors, flavors & fragrances, pharmaceuticals, and personal care. The asset turnover would be ~1x.

One plant of MEHQ (Monomethyl ether of hydroquinone) and Guaiacol was commissioned in March 2024. The company is still working on getting its product tested and sampled with customers. It is also working on enhancing the yield and efficiency of the plant.

The other products, i.e., anisole, 4-methoxyethyl phenol, and two more products to be commissioned in H2 FY25.

The ATBS capacity expansion from 40,000 to 60,000 metric tons per annum is proceeding well. It is expected to be completed in H2 FY25.

As of date, the company commissioned a total of ~33 megawatts of solar power plant. This will help in reducing the energy dependence on non-renewable sources.

The company expects revenue growth of ~20% CAGR over the next 3 years mainly driven by the new products and some of its existing products.

The management anticipates an EBITDA margin of ~26% on a sustainable basis.

For FY25, the company plans to incur capital expenditure of ₹550 crore including the subsidiary.

The management anticipates the demand for ATBS to remain strong and expects double-digit sales growth in the next financial year.

In antioxidants business, the company expects sales of ~₹280-₹300 crore in FY25. Antioxidants business is expected to be a growth driver for the company. The peak revenue potential of the antioxidants business is ~₹700 crore.

In Veeral Organics Private Limited, the company expects sales of ~₹50 crore in FY25. It expects some sales from its recently commissioned MEHQ and Guaiacol plant.

Velumani was interviewed toady on CNBC. As always brutally honest. Explained that the valuation that he exited on was fortunate and way above anything that will be seen by Thyro or any Diagnostic till 2028 … till then we have to wait i guess.

but i think thyro will do better and reach old valuation if API can sell their stakes and the approach current MD has to expand to new geography in Africa with reputed technology will be the way ahead.

Velu also said that the organized diagnostic now was much better certified and quality is better.

i wish he once again buy it back …very frugal and made sure all the money spent was to achieve lowest cost

Please provide your views on the company as well as the research. I and a friend of mine have taken value investing over the last 5-6 months and this is one of the first reports I have made

LT Foods

LTF, established in 1990, mills, processes and markets rice (largely basmati). The company has established brands such as Daawat, Royal, Devaaya, Rozana, Heritage, and Chef’s Secretz, varying from basic to premium quality, both in the domestic and overseas markets. It has facilities in Haryana, Punjab, and Madhya Pradesh, with combined milling capacity of 106 tonne per hour (tph) and individual capacity of 58 tph

| Date of report: | 16-05-2024 | Competitor PE | 11 (KRBL), 9 (Chamanlal) | Sector | Consumer foods |

|---|---|---|---|---|---|

| CMP: | 229 | Current PE | 13.9 | No of Years | 34 |

| Market Cap: | 7936 | Highest PE | 20.8 (2018) | Key Products | Basmati Rice |

| ROCE / ROE | 17% / 17% | Lowest PE | 2 (2012) | Key Competitor | KRBL, C Sethia, Sarveshwar, GRM |

Business Model and Industry Analysis

Overview:

Company produces Basmati and other speciality rice (Contributing 81% of FY23 sales). They have 2 more segments, viz. Organic foods and ingredient (11% of FY23) and Ready to heat segment (2%)

Core business is working capital intensive (220-230 days is normal working capital), as rice must be purchased and aged for 1-2 years before sales. It also exposes company to price risk since rice purchased in up-cycle might be sold in down-cycle. Company appears to have managed both the risks well over time, given margin consistency and expansion

New business segments are in line with company’s current strengths and weaknesses. They use existing distribution network and cash flows to build the brand while removing cyclicity of paddy prices with branded products. Further, with increasing trend of health-conscious eating and ready to heat/cook foods with both partners working, the two segments can get good growth according to us.

Industry Growth:

India produced ~134 MnT rice in 22-23, of which 9.5 MnT was Basmati rice. 4.6 MnT Basmati was exported. Indian Basmati exports have grown by 7% over last 10 years. Iran, Iraq, UAE, Yemen and US are the top 5 consumers of Indian rice. Pakistan is the only other Basmati producing country (Owing to GI protection)

Domestic Basmati rice market is expected to grow at 1% CAGR over next 5 years, while international at 2.7%. Currently, 40% Indian market consumes Basmati (19% consumes packaged Basmati rice)

Basmati rice prices are not growing linearly, with all value growth coming from volume

Indian Basmati Export Market

| Year | FY19 | FY20 | FY21 | FY22 | FY23 |

|---|---|---|---|---|---|

| INR/Kg | 74 | 70 | 65 | 67 | 83 |

| Exports (MnT) | 4.4 | 4.5 | 4.6 | 3.9 | 4.6 |

| Value (INR Cr) | 32671 | 31185 | 30095 | 26452 | 37840 |

Capacity Utilisation:

The company has 14 facilities in India, USA, Uganda and Netherlands engaged in rice production (5), rice packaging (6), Organic foods production (2) and Ready-to-heat products (1). Its capacity utilization for FY23: 80%; FY22: 65.3%; FY21: 65.1%. Utilization is expected to go up in FY24 for rice products, given consistent increase in topline despite volatile prices. Organic facility will show drop in utilization in FY24 due to ADD in US

Opportunities:

Company is expected to grow Organic products segment (Currently contributing 11% to sales) and ready to heat segment. Both segments appear to be in correct direction, and we will monitor their execution. Further, they have mentioned no capacity expansion plans currently, and strengthening only distribution and brand in FY23 reports as well as con-calls. It seems prudent given 80% cap utilization currently

Risk:

Future Expansion:

No major capacity expansion plans currently. In terms of margin expansion, target is to expand EBITDA% by 1.5% over the next 5 years

Competion:

KRBL is the biggest domestic player, followed by LT Foods. KRBL competes only in Basmati rice. Chamanlal Setia, Sarveshwar foods and GRM Overseas are other major competitors. LT Foods enjoys dominant position against all of them in exports, and it is catching up in domestic as well. Given Basmati industry’s domestic and global growth rates, it is clear LTF is capturing market share

Basmati and other rice products (Core operating segment)

| Growth Rate | Particulars | FY23 | FY22 | FY21 | FY20 | FY19 |

|---|---|---|---|---|---|---|

| 18% | LTF – Domestic | 1829 | 1442 | 1143 | 986 | 947 |

| 16% | LTF – International | 3812 | 2841 | 2740 | 2322 | 2103 |

| 17% | LTF Total | 5641 | 4283 | 3883 | 3308 | 3050 |

| 12% | KRBL – Domestic | 3335 | 2647 | 1992 | 2285 | 2142 |

| 1% | KRBL – International | 1931 | 1451 | 1896 | 2084 | 1843 |

| 7% | KRBL Total | 5266 | 4098 | 3888 | 4369 | 3985 |

Management:

Institutional Investor:

FII and DII continue to hold 18% (Including 9% of Saudi Arabian quasi-govt investment)

Historical Data and Financials

Profit N Loss Account:

Balance Sheet:

Cash Flow:

Valuation and future potential:

| Particular | Current | 52W High | 52W Low | Historical High | Historical Low | Industry Median |

|---|---|---|---|---|---|---|

| Price | 216 | 235 (12/2023) | 106 (5/2023) | 235 (12/2023) | 2.8 (2009) | – |

| PE Ratio | 13 | 15.1 | 10 | 15.1 | – | 12 |

| EPS | 16.5 | 15.2 | 12.3 | 15.2 | – | – |

| Price/Book | 2.4 | 2.6 | 1.7 | 2.6 | – | 1.6 |

| EV/EBITDA | 8.4 | 9.5 | 7.1 | 9.5 | – | 7 |

| ROCE | 17% | – | – | – | – | 19% |

Industry median is calculated from LT Foods, KRBL, Chamanlal Setia and Sarveshwar Foods

Valuation:

Future Potential:

Soft factors for consideration:

Disclaimer: This is a study report, not for any decision making or investment advisory.

Date:16th May 2024

Generally, the resignation of a CFO is definitely concerning. However, I’ve looked at it from a different perspective (whether it is for better or worse/ am I right or wrong, I don’t know).

Look, the company does a topline of only ~100 crores and has a market cap of ~200 crores. If as a working professional I get a chance to move to a bigger, better company with a more challenging role and better monetary benefits, I’ll take it. Then what stops someone else from doing the same? They may do it either for their personal ambition or for the welfare of their family or maybe both. When I worked at a company doing a topline of INR 30-40 crs, my goal was to move a bigger company, I did eventually end up working with a company doing a topline of INR 80,000 crores. For me the reason was two-fold, making better money and cutting my teeth with the best, maybe it is the same situation here or maybe it isn’t, we will never know. The management isn’t going to tell us for sure.

If it is of any solace, I have met a bunch of seasoned micro-cap investors and they rate Dr. Sane highly and don’t find anything amiss. Furthermore, the company has some seasoned and successful investors as Mukul Agarwal invested in it. Dr. Sane and the seasoned investors have far more to lose than I do, so I’m comfortable holding my position here (for now!). Also, overall the stock has been butchered and has fallen 51% from its 52-w high. It only needs a flicker of some positive news to take it up.

Though, in all honesty I’m more concerned about the management missing their guidance for FY24. In their last con-call Dr. Sane had suggested they’ll “very easily” grow their topline by 20% and also show margin improvement. However, in the last call with Arihant Capital it turns out the topline promised for FY24 has now conveniently moved to FY25. This to me is rather concerning for a company this size. I will try to attend the con-call and check with the management the difficulties they’ve faced in meeting their guidance this year.

Apart from the above, the stock continues to be a hold for me and I’ll continue to monitor their execution over FY25.

@LarryWink The daily moving averages are more about closing prices (rather than volumes).

Even DMA or EMA that we plan to use is still a lagging indicator. It will not be able to spot a change in direction before it happens, but it can tell you quickly that it has changed. Further, EMA may be better than DMA as it will give more importance to recent data.

There are some other leading indicators like RSI, but my understanding is that they can generate a lot of false indications.