How would you go about negotiating an NCD on platform such as Indiabonds.

Posts in category Value Pickr

Burger King ~ Whopper of an Opportunity (18-05-2024)

Yes, in the recent con call, it was mentioned that RBI sits on board of RBA and owns a stake in RBA

Ranvir’s Portfolio (18-05-2024)

I think, ADF foods at CMP is a descent buy

Disc: its just my personal opinion, have bought recently, like the company and recent business momentum

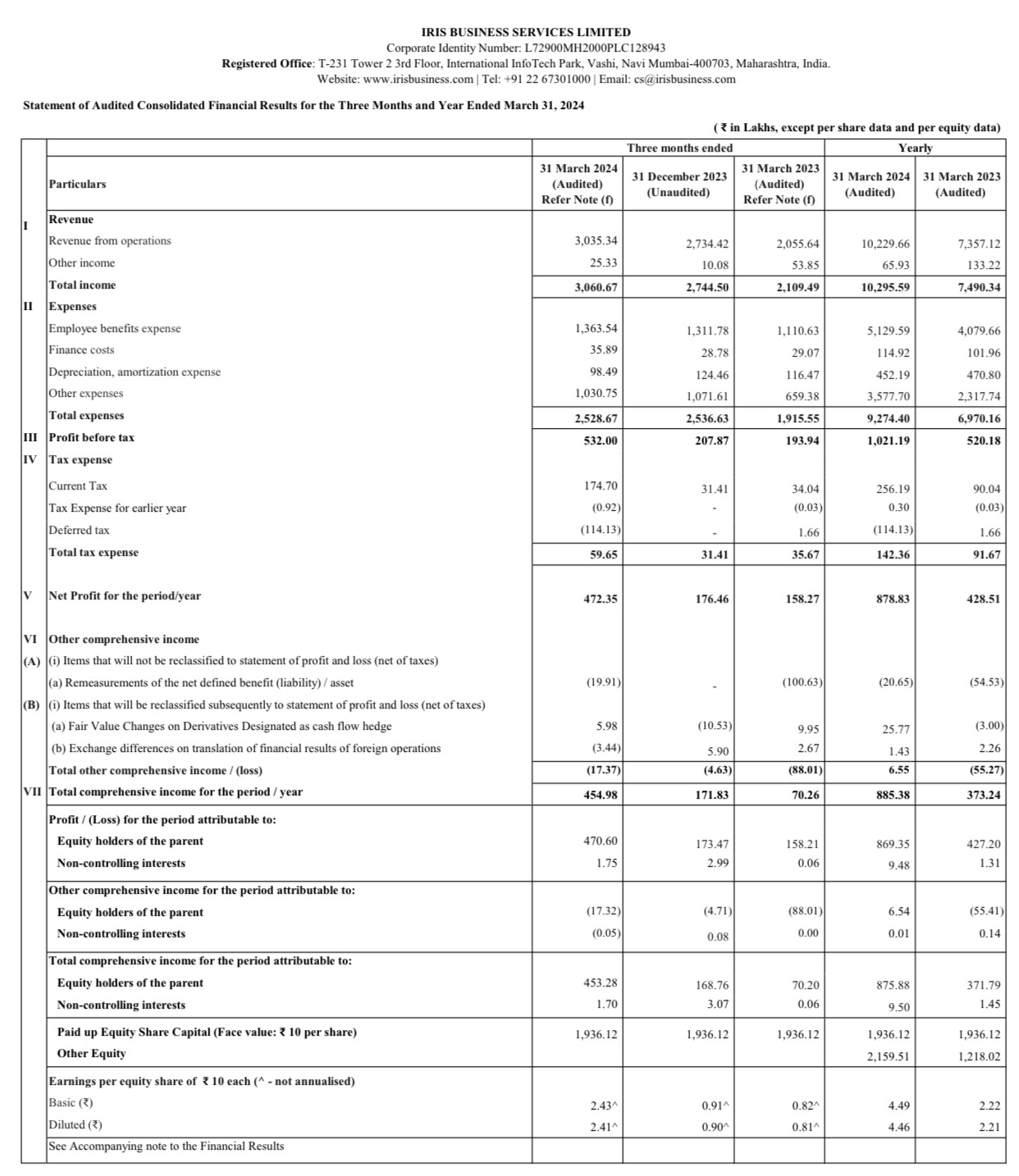

Iris Business Services – Emerging SAAS Microcap (18-05-2024)

Superb results from IRIS business services.

PAT zooms 66% YOY

Lincoln Pharma … the next mid-cap pharma in the making …? (18-05-2024)

Company had their first conference call ever – which is a good sign!

There were few inconsistencies in the answers given by management. I hope they come better prepared next time around.

Few notes:

Company mentioned Rs 1000 Cr revenue target in next three years from current 581 Cr. That is ~20% cagr.

At some other time, they mentioned 15-18% growth year-on-year going forward.

(in previous quarterly ppt, they had mentioned Rs. 750 Cr revenue target by FY26).

Let’s see where they land in coming years.

But main message is, in any scenario, company is confident of >15% growth conservatively.

They are trying to improve the business in export markets and also in domestic market. Reaching out directly to doctors, increasing MRs etc.

New “Cephalosporin” capacity to generate 55-60Cr revenue in FY25. That alone would be 9-10% growth over FY24 revenue. Cephalosporin could generate ~150Cr revenue when utilized fully.

Company’s capex in FY25 & FY26 to be driven from internal accruals. So expect them to remain debt free.

There were questions regarding loans to promoters – which could be a red flag. Needs to be checked in annual report.

Lastly, they invited investors to come and meet them in office and also for the factory tour! Seems like the company is trying to get investors attention.

Overall, company still looks decent with 12x-13x PE, debt free status and quite grower without much hullabaloo in the current multi-bagger mania.

Disc. Invested

Lincoln Pharma … the next mid-cap pharma in the making …? (18-05-2024)

Company had their first conference call ever – which is a good sign!

There were few inconsistencies in the answers given by management. I hope they come better prepared next time around.

Few notes:

Company mentioned Rs 1000 Cr revenue target in next three years from current 581 Cr. That is ~20% cagr.

At some other time, they mentioned 15-18% growth year-on-year going forward.

(in previous quarterly ppt, they had mentioned Rs. 750 Cr revenue target by FY26).

Let’s see where they land in coming years.

But main message is, in any scenario, company is confident of >15% growth conservatively.

They are trying to improve the business in export markets and also in domestic market. Reaching out directly to doctors, increasing MRs etc.

New “Cephalosporin” capacity to generate 55-60Cr revenue in FY25. That alone would be 9-10% growth over FY24 revenue. Cephalosporin could generate ~150Cr revenue when utilized fully.

Company’s capex in FY25 & FY26 to be driven from internal accruals. So expect them to remain debt free.

There were questions regarding loans to promoters – which could be a red flag. Needs to be checked in annual report.

Lastly, they invited investors to come and meet them in office and also for the factory tour! Seems like the company is trying to get investors attention.

Overall, company still looks decent with 12x-13x PE, debt free status and quite grower without much hullabaloo in the current multi-bagger mania.

Disc. Invested

Deep Industries (DIL) (18-05-2024)

(post deleted by author)

Deep Industries (DIL) (18-05-2024)

(post deleted by author)