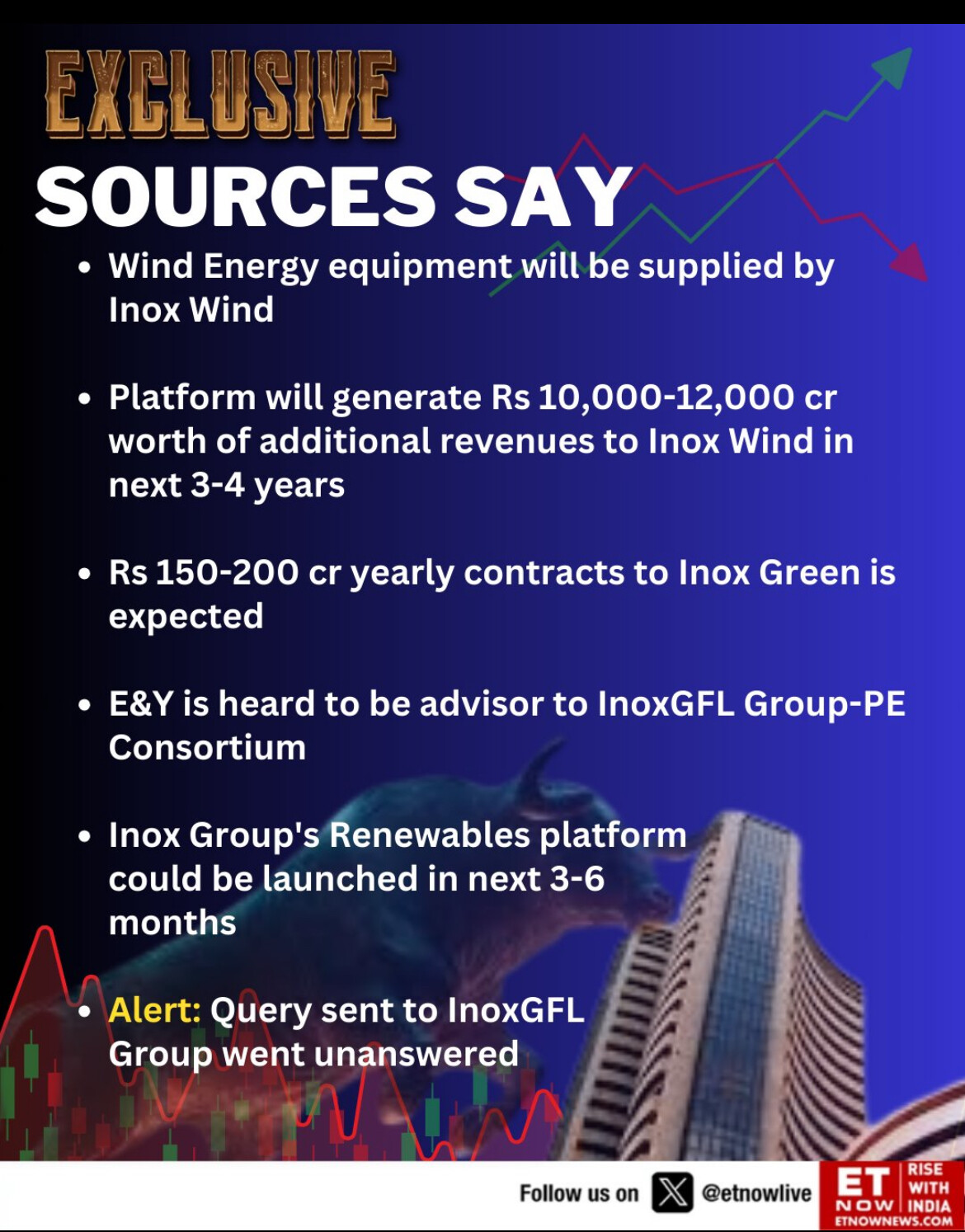

Stock reversed beautifully from the trendline as shared above. Interesting development in the inox gfl group

https://x.com/etnowlive/status/1790955498096959957?s=48&t=taDyVj4_oT168hw6IQLVFA

Stock reversed beautifully from the trendline as shared above. Interesting development in the inox gfl group

https://x.com/etnowlive/status/1790955498096959957?s=48&t=taDyVj4_oT168hw6IQLVFA

@yashchandak KRBL last few years are very turbulent. In one Quarter they were able to export high broken rice and in other quarter, very high bulk export, in one quarter they have Saudi sales starting and in other quarter Saudi sales back to zero. In one quarter, a bulk shipment is not delivered to client and revenue got deferred to other quarter.

I would recommend you read concalls of LTFOODS and KRBL for last 5 years, You will neither find positive nor negative surprises from sales perspective for LTFoods except impact of soya sale due to US anti dumping duty. But in KRBL, you will find lot of these surprise both on positive and negative side, which makes their revenue to fluctuate lot higher even after factoring rice/paddy price fluctuation, this makes their Ebitda all over place

When it comes to LTFoods margin, In presentation you can find the Rice segments margin, you will find fluctuations, but offcourse not to the extent of KRBL which is due to their own problems

Q1 – 12.9%, Q2 – 13.9%, Q3 – 14.8%

As per today concall Management has lowered the F.Y 2026 revenue guidance by 10% to 3600 cr ,earlier management guided for 4000 cr revenue and also export guidance lowered to 10% of sales instead of earlier 20% .

EPC guidance is 200-250 Cr, which will also contribute to the PAT plus this is order book as start of this year, company will get more orders eventually.

I read somewhere that this 250-300 Cr capex is aligned towards crane business , as Rahul pointed out that 100 Cr addition of gross block gives an additional PAT of 7 Cr than on an 300 Cr capex the PAT gorwth is 21 Cr . This over a base of 188 Cr – FY 24 bottomline is just 11% PAT growth – (given the utilization and yield remains at current level) in upcoming FY from the core business , EPC excluded . Can someone help me understand what am I missing out ?

ship order is all time low, and still no one is buying new assets even when crazy prices on ton mile currently. if you look at stocks like Scorpio tankers, even they are clearing debts , but no addition of new ships…as you rightly pointed 40% EPS degrowth and still stock should make decent profits plus will be zero debt shipping company…

New Product launched in Q4_2024

Disc: Invested and biased

Concall Highlights Q4FY24

@sheethal27

I am sharing my mutual funds portfolio here, but many ppl will not like this as generally ppl think 3-4 mutual funds are enough and it gives enough exposure to most companies. But my list is exhaustive, covering most types of funds available with enough exposure to Active funds, Index funds, Momentum funds and even factor funds…

Active Funds :-

Index Funds : –

Momentum/ Factor

What’s the view regarding syngene with opaque management and no so forthcoming in guidance regarding molecules in pipeline.