MANAGEMENT PERSPECTIVE

As we look ahead, we foresee growing demands for our products and are confident in sustaining our current growth trends in Revenue and Profitability.

Investor Presentation is here :

MANAGEMENT PERSPECTIVE

As we look ahead, we foresee growing demands for our products and are confident in sustaining our current growth trends in Revenue and Profitability.

Investor Presentation is here :

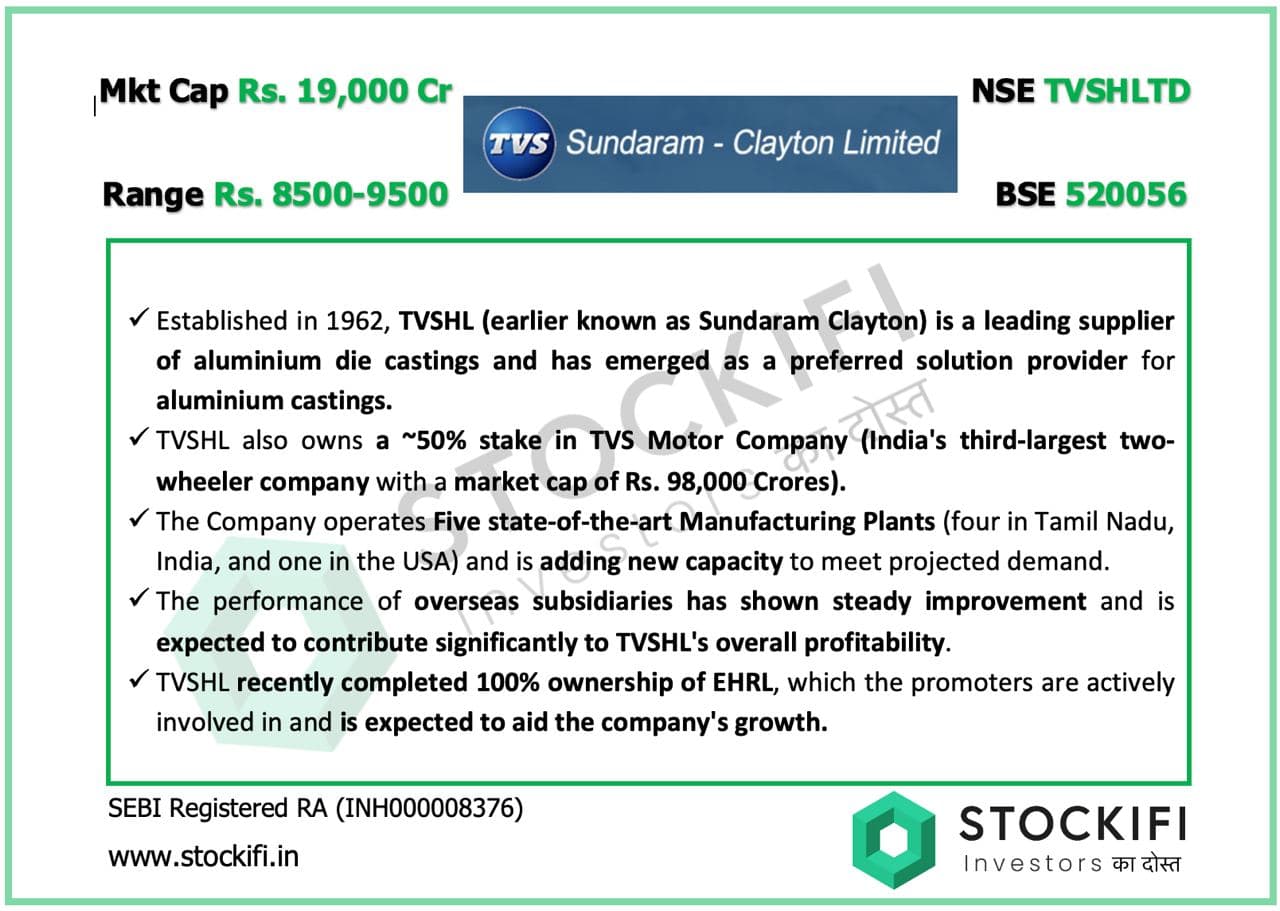

No, TVS Holdings is not involved in die casting. The aluminium auto parts business was demerged and listed separately as Sundaram Clayton.

I don’t know about the competition in auto components. Sundaram Clayton is still a high debt and low margin business.

You read it’s annual report for further details.

The recent rally in TVS Holdings is more related to new NBFC venture rather than TVS motors stake. I believe TVS Holdings currently reached the max possible discount. In general when the discount between holding company and the actual company comes close to 52-57%, you should exit, If you follow the previous cycles ( based on reading from report). However due to recent announcements ( venture into NBFC, Real estate) and uptrend in Auto sector,I continue to Hold, if you have bought previously. However, New entry is not an value buy from now as it’s like predicting the future without any results.

Hi

Yes this company can be a multibagger from this levels as now bavla facility will start production after succesful edqm inspection plus french facility for next yr will add 20million euros plus indian crams business they can reach to 40% operating margins which they used to do precovid…as pe there latest concall fy25 they can do 20% ebitda and by next fiscal they can do ebitda of 25% with 15% topline growth…company available at a mere 12pe forward fy26 earnings

Because of management issues in past, it raids and issues related to goodwill recognition of 1000 crore, edqm issues this company is not getting desired valuation but once they start showing better results with 25% ebitda there might be a rerating on the cards.

Any senior members @Lynch any updates on the it raids outcome…i couldnt found out what was the penalty levied on the company and is the matter closed or still ongoing?

Disc

Recently added and looking to add more in current volatility

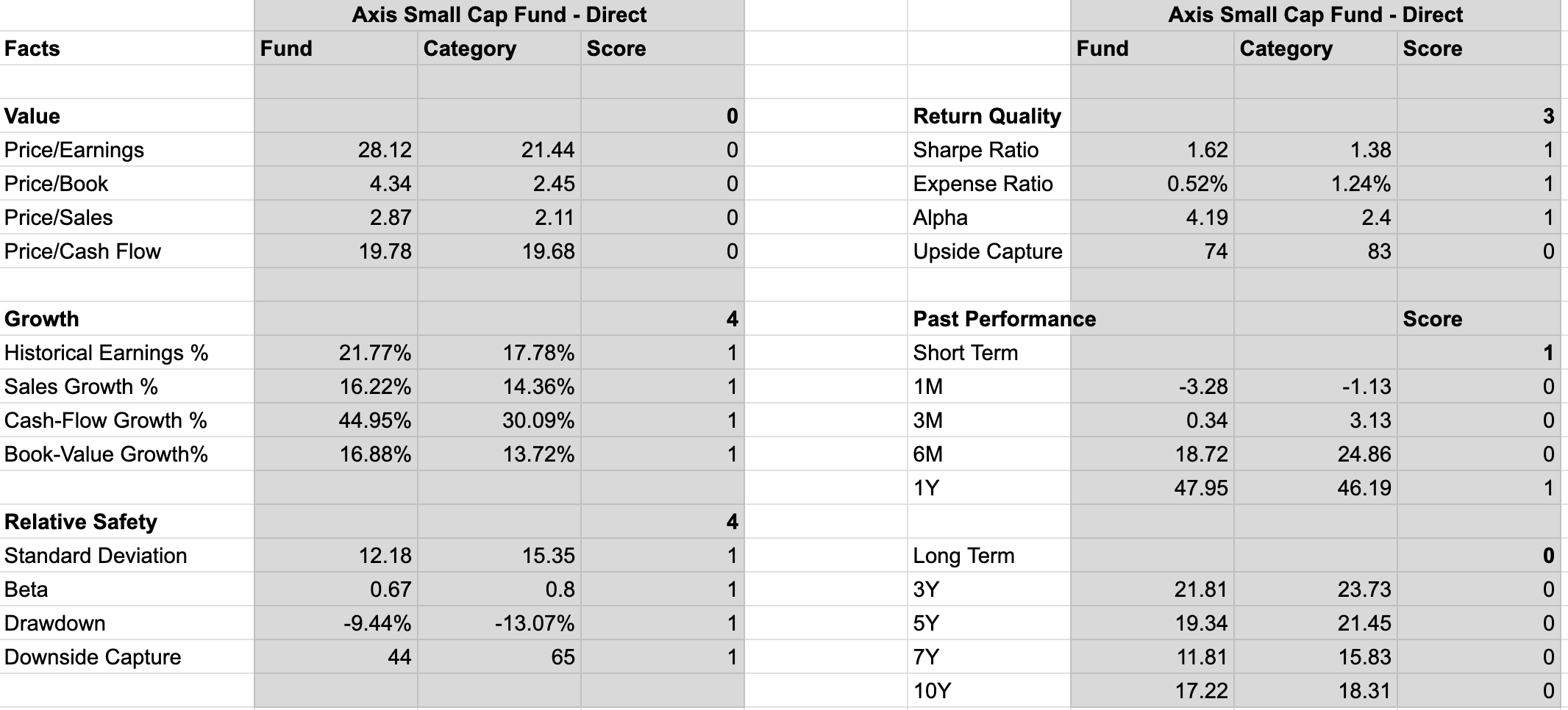

Hi all, I am currently trying to develop a framework for analysing Equity Mutual Funds.

As of now, I’ve narrowed the following metrics that I will be looking at:

Attached is an image of how I’ll be scoring and going about these metrics.

Would love to know if there are any additions/ changes I should be making to the model.

Hi Kandukuri,

I recently came across a report (publicly available) stating that TVS Holdings is a leading supplier of aluminum die castings. My understanding was that TVS Holdings had transitioned into a core investment company (CIC) and no longer directly manufactures auto parts.

Could you please clarify whether TVS Holdings is still involved in die casting or the auto parts business?

Considering TVS Motors market cap 99241cr – 50.26% value of holding is 49.8k cr. Currently trading at 57% which can only be a trigger for TVS holdings to rerate?

will you be able to share your code?

Because Ujjivan Financial Services is being merged with Ujjivan Small Finance Bank. You will be getting shares of 11.6 shares of Ujjivan SFB for every share you used to hold in Ujjivan Financial Services.

These shares of Ujjivan SFB should be credited to your demat account in next 20-35 days and get listed and start trading in 30-45 days

During a period of higher capex, FCF will look negative, that is the case for most small cap companies. I think OCF to ebitda is a better metric suggesting whether the company is able to recover money from its day to day operations, and a 5 year average of 95-100% pre tax suggest a very good operating business

Couldn’t export as PDF. Same content sourced from another website.

Points for importance

Page 3 & 4/24 on commentary page: Water Projects

Furthermore, we are looking forward for partners with strong background with credentials to cover the technical eligibility for strategic partnerships for breakthrough projects in water sector.

Page 5/24, HAM Project and monetization plan

The total equity requirement of 10 HAM projects is about INR1,461 crores out of which we have infused INR694 crores in this financial year and INR545 crores is estimated to be infused in FY ’25. Let me give the glimpse of the status of the monetization of 4 HAM projects. First tranche on the 3 projects which we have sold in the last year, 3 SPV is Gurgaon Sohna, Rewari Ateli, and Ateli Narnaul. They have been completed on 21st of March – 21st November 2023, with 100% SPV shares transferred from H.G. Infra to Highway Infrastructure Trust. We have received INR315 crores as of now, and INR60 crores will be released on the receipt of approval from NHAI for GST changed in law claim. It is expected to be received by June 2024.