That data also highly likely has some problem. Company did 80 cr. revenue in full year of FY23, highly unlikely that 72 cr. of that was done just in Q4’23.

Posts in category Value Pickr

The Anup Engineering Ltd – Can it scale up? (09-05-2024)

Another such opportunity?

Which one? Envisol?

Manappuram Finance (08-05-2024)

General information of current state of affairs. Applies to NBFCs Mannapuram & Muthoot.

Route Mobile – Internet, Mobile & Telecom (08-05-2024)

luckily these indian hype men tend to not speak much english

Macfos Limited- A niche E-commerce Company (08-05-2024)

Examining the annual results for 2023 reveals sales of 80 Cr and a profit of 7 Cr. However, when focusing solely on the March quarter, sales and profits are reported as 72 Cr and 7.93 Cr respectively. This scenario seems implausible as it suggests the company generated nearly all its sales and profits within a single quarter, which is unlikely. Therefore, it appears that the data presented by the screener is inaccurate. Despite this discrepancy, the company has demonstrated decent growth, evident in its annual performance.

Investing Basics – Feel free to ask the most basic questions (08-05-2024)

There are various scenarios exist not one exact can be derived unless you give the whole picture, this stays good in all stock analysis, although I try to give you the possible 4 reasons

- Aggressive accounting practices: The company might be managing its earnings through aggressive accounting methods, which inflate CFO relative to PAT.

- High depreciation or amortization: If the company has significant non-cash expenses like depreciation or amortization, it could lead to a higher CFO/PAT ratio.

- Tax management: Effective tax planning strategies could also influence the CFO/PAT ratio by reducing the tax impact on profits.

- Capital structure: If the company has substantial non-operating income or expenses, such as interest income or expenses from investments or financing activities, it could affect the ratio.

The ideal CFO/PAT ratio varies across industries and depends on factors like capital intensity, growth prospects, and business models. Generally, a higher ratio suggests better cash flow conversion from profits, but a sustainable and stable ratio is often preferred over extremes. For instance, a ratio between 0.6 and 0.8 is often considered healthy, but it’s essential to compare it with industry benchmarks and historical performance for a meaningful analysis.

DCX Systems Ltd (08-05-2024)

Nomura has initiated on the India Defence space, with DCX mentioned.

Anyone know where one can access the complete PFD copy?

Dharmaj ready to benefit from high demand for agrochemicals (08-05-2024)

On a conservative side 13 % would be bit difficult in dharmaj but the growth prospects looking good

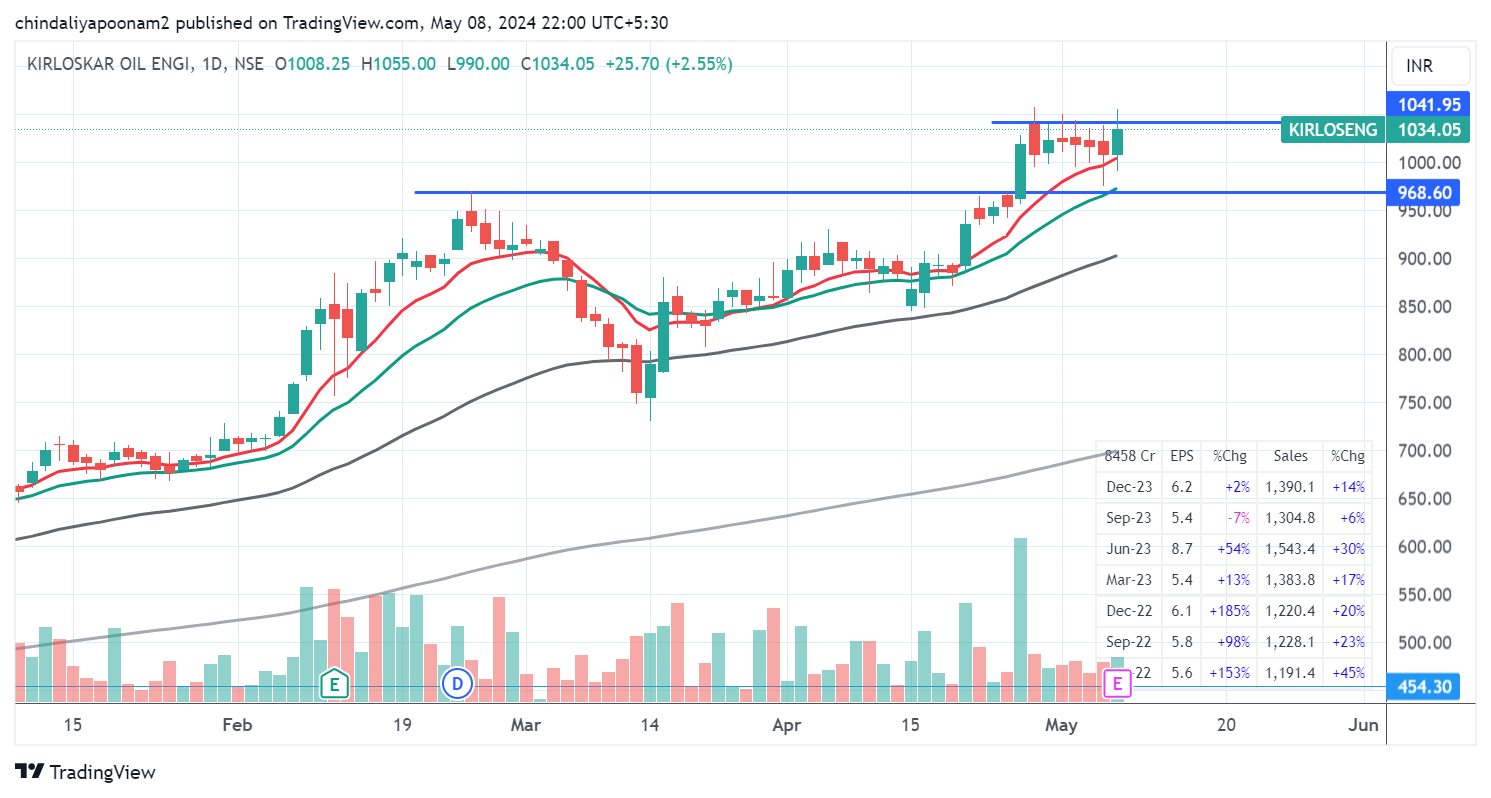

52 week highs and all time highs strategy (08-05-2024)

Kirloskar Oil Engine looking good on charts… Stock gave breakout with good volumes, now consolidating near ATH

Macfos Limited- A niche E-commerce Company (08-05-2024)

The result shown in the screenshot above compares the result of two quarters a year apart. So Jan-March 2024 has been compared with Jan-March 2023. Taken that way the company has experienced de-growth, which is bad.

Comparing the previous quarter (Q3FY24 vs Q4FY24) within the same financial year, the company has done good. But this is seasonality at play. Majority of the companies especially manufacturing companies, post their best quarter as Q4 of a financial year. Although, Macfos is not a manufacturing company.

As far as financial year comparison is compared i.e. FY23 vs FY24 is concerned, the company has done good and grown.

As an investor the de-growth that the company has experienced compared to last year’s quarter is a fly in the ointment, given that it is a microcap, expected to grow exponentially.