Does anyone know when is the concall scheduled for BFS? Couldn’t find it in NSE website.

Posts in category Value Pickr

Sirca Paints India Limited (07-05-2024)

high gambling going on ( pump and dump scheme )

-

many previous comments are deleted , one of comments contained 3 mutual funds doing interview with sirca

-

my comments are also deleted , one of the line in paragraph comments contained there was no reason for sirca to go 304 to 350 , i publicily commented on this forum

these gave me insights Mutual funds or High HNI Trader or gambler is playing pump and dump scheme to fool the market and investors also smart money is buying sirca

because HDFC mutual fund were the ones who interviewed ,

Mark my words , sirca will not fall till 295 or 250 , why i am saying 250 , because gamblers are fool and can do anything with money

Paints sector is weak but this fall is not justified ,

example

i have learned my lesson from FCL , i commented on valuepicker why FCL is on 205 from 340 or 400 52 high price ,gamblers pumped up price , even promoters bough it ( promoter buy was fair buy but gamblers bought after my comment )

now just wait and watch the show on sirca paints what they are doing

because fundamental investors there is no need to worry

thanks to aayush mittal for teaching me learning fro failures or mistakes why stock is not running

first time , there was no reason to sirca to go 304 to 350 at that time

now , sirca was now fairly valued , so gamblers have brought price to 309

if we all agree , 309 is fair price , then it should not break 295 or 250

it all is game of fair value and margiin of safety

All these topics comes under value investing ( note for admin to not delete the post _)

i am not sebi registered analyst , please do own research before investing, above all comments are biased opinion , as i am already investor in sirca

thanks to gamblers , we can buy more sirca or average it

2 types of ending

If it is fundamental mistake

We will know the real reason for in coming concalls and stock will be fall and averagely priced

Or

Sweet Concall would be happened , price will rise

now just wait and watch the show on sirca paints

Sona Comstar BLW – Direct EV Play (07-05-2024)

They can win more orders in the years to come and that too perhaps at higher value. For instance they won order worth of 5100cr in the last fiscal, when the EV and overall automotive market was slow. I believe when the EV adoption is accelerated, the order wins for Sona will be more.

Sona Comstar BLW – Direct EV Play (07-05-2024)

If they can maintain the run rate of 25% CAGR then order book will be consumed by FY28, in between they can secure few more orders for new products and high torque motors which are under development can be used in E-buses and trucks.

India it self is a big market interms of E-buses in the next 4-5 years.

HIL – Eco (onomic) friendly way to play rural prosperity in India (07-05-2024)

HIL LTD Q4FY24 CONS

NET LOSS OF 0.11 CR VS 4.6 CR PROFIT (YOY), Q3 7 CR LOSS

REVENUE 852 CR VS 863 CR ( YOY), Q3 784CR

EBITDA 17 CR VS 37 CR (YOY), Q3 2 CR

EBITDA MARGIN 2% VS 0.37% (YOY), Q3 2%

Bottom line affected due to 158.44 cr worth they purchase share in

Crcstia Polytcch Private Limited,

Topline lndusuies Private Limited,

Aditya Polytechnic Private Limited,

Sainath Polymers,

Aditya Industries

CO RECOMMEDNED DIVIDEND 22.5 RS PER SHARE

Need to listen the concall now to get more understanding on the outlook moving ahead, Anyone tracking this company in the forum?

SmallCap Hunter : Trying to find the dark horses with triggers (07-05-2024)

any updates on subex??

Manappuram Finance (07-05-2024)

Asirvad operates as a fully-owned subsidiary of MF. In my view, shareholders of Mannapuram Finance might not receive any shares from the IPO listing since it is not a demerger. Nevertheless, if you’re interested in the microfinance sector, you could consider applying for the IPO or acquiring shares from the open market. Please feel free to correct me if I’m mistaken

Disclosure: I have invested.

Punjab Chemicals & Crop Protection Limited (PCCPL) A Clear Runway Ahead! (07-05-2024)

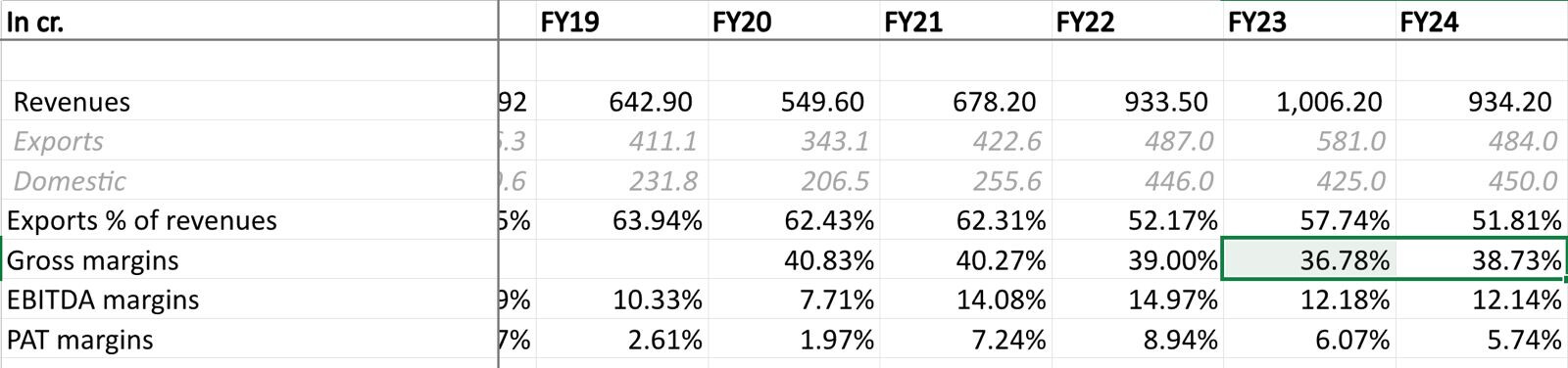

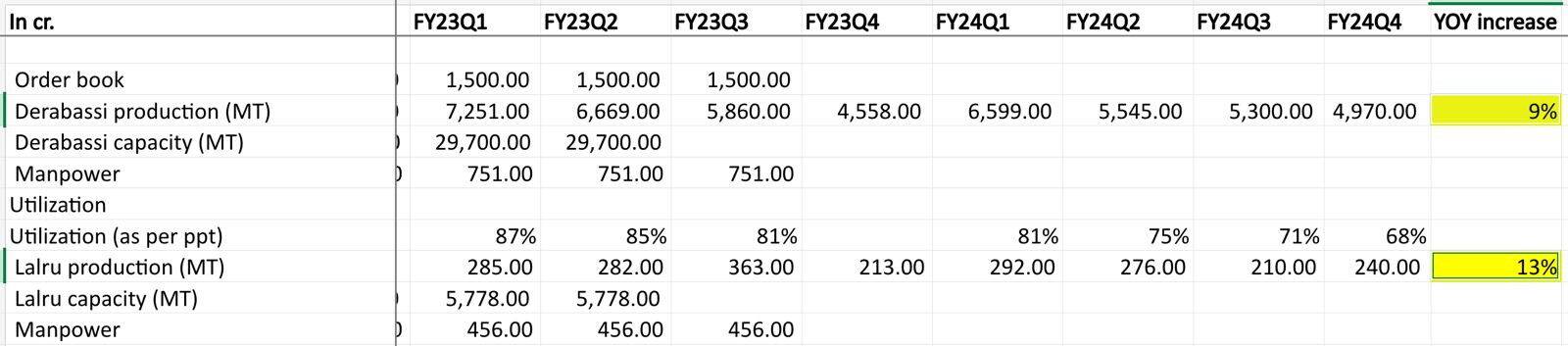

Punjab came with flattish numbers (1% sales growth, -25% EPS decline). The good thing about FY25 was their numbers were way better than most other technical manufacturers, they improved gross margins while seeing margin decline in sales (-7% in FY24) in a very tough year.

Volume growth is coming back and they expect complete revival by H2FY25. Management is also guiding for doubling of sales in 1-3 years. Concall notes below.

FY24Q4

-

Seeing demand offshoots and expect recovery in second half of FY25

-

Freight costs have increased significantly for certain routes (e.g. Europe, USA). 1.2 cr. increase in freight + higher CSR costs + certain one-time costs which have resulted in EBITDA margin decline despite maintaining gross margins

-

Have received commercial orders for new molecules (both in agchem and specialty chemical)

-

Receivable increase is temporary and because of domestic receivables being stretched from 90-100 days to 120-130 days. This has started coming back to normal in May

-

Capex

-

FY25: 50 cr. in existing sites (1 new manufacturing block + maintenance)

-

Continue scouting for new production sites and want to time it to industry revival

-

Expect 1000-1200 cr. additional revenues in next 1-3 years. 10-15% of this will come from existing products and remaining from new products. This will require 250-300 cr. capex (3.5-4x asset turns) at existing sites and can be done from their existing plans

-

-

New products

-

New product contributed 7% to revenues

-

1 product has global sales potential of $100mn, another one has $20-25mn

-

Producing 2-3 products every 6 months, should commercialize 2-3 new intermediates in next 6-months

-

EU commercialized product should reflect in next 6 months because of high current inventory

-

-

Business mix: 70% Derabassi, 15-18% Lalru, 12-15% Pune

Disclosure: Invested (position size here, no transactions in last-30 days)

Action construction equipment ltd (07-05-2024)

From LinkedIn it is evident they’ve sold about 25 backhoe loaders as of Sep’23 i.e. in H1. I’ve got not clue as to the how much each of those contribute to revenues though ![]()

Indian Defense Sector (07-05-2024)

Mishra Dhatu Nigam Limited has executed a joint venture agreement with four other companies to incorporate a Section 8 Company under the Defence Testing Infrastructure Scheme. The proposed company will be named ‘Advanced Materials (Defence) Testing Foundation’ and will focus on indigenous research, development, and manufacturing in the defense sector.