Hey guy. I’m Shubham Maheshwari and I’m pretty new to this journey compared to you all seasoned investors. I have been investing since my Bschool days at JBIMS-2019. I feel Investing can sometimes feel like a solitary pursuit, but it doesn’t have to be. By coming together as a community, we can amplify our collective wisdom and support each other’s growth. I see many threads here where people are forming local communities in various cities and I found one Mumbai thread as well which was closed long ago. Can we start afresh? Or if there is an active community that meets up regularly then I’d love to be a part of it. Hoping to see some positive responses.

Posts in category Value Pickr

Rural Elect Corp (02-05-2024)

Yup thats true. lets watch how future turns out.

Som Distilleries and Breweries (02-05-2024)

Agree on packaging cost he can choose not to answer…but packaging cost was the second question that investor asked…

The first question was about tax differences for which the company seemed hesitant and asked him to connect one to one and maybe because they signalled the coordinator, the coordinator abruptly asked the investor to rejoin the queue even though the investor had asked just 1 question… To which even the investor seemed surprised.

Well public meetings can be handled better if they want to win the confidence of the investors.

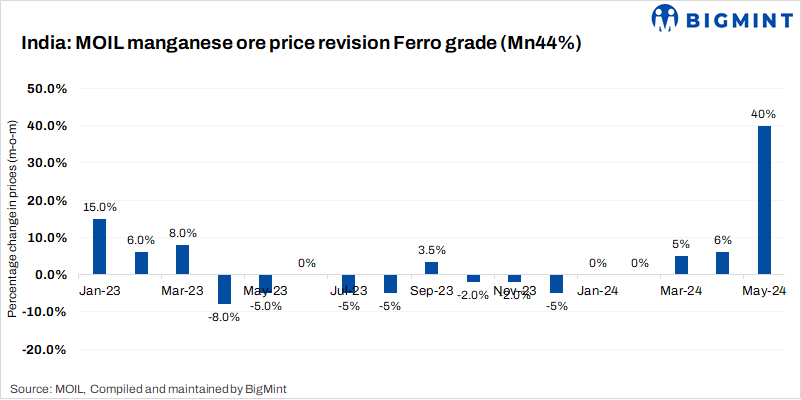

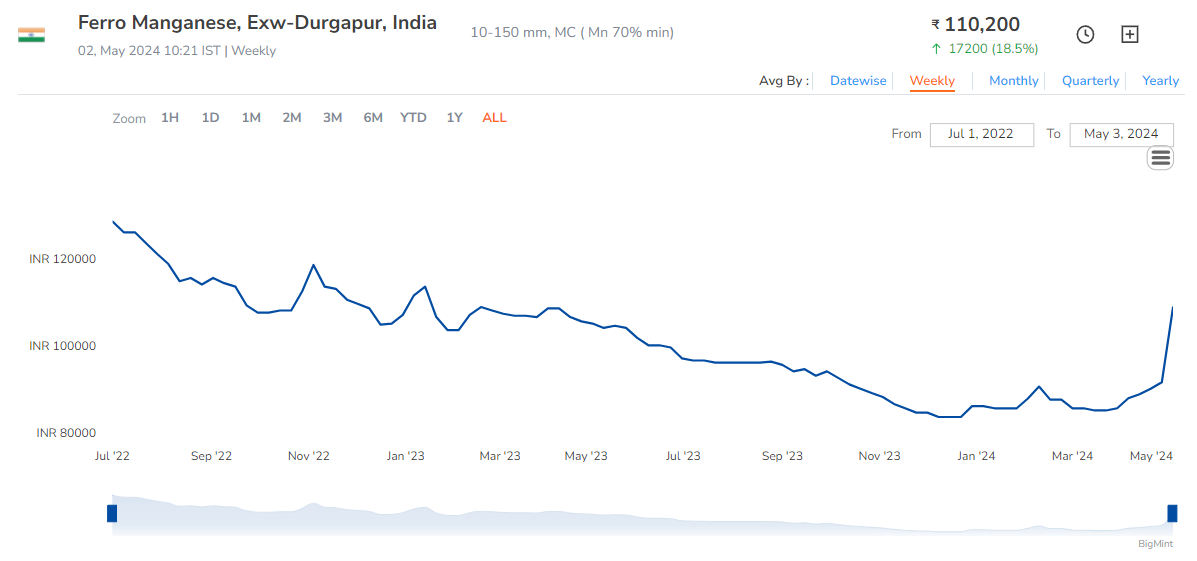

Maithan Alloys Ltd (02-05-2024)

Silico manganese prices are now at a 2-year high.

Disc: Invested

Gurugram Valuepickr (02-05-2024)

Certainly! Would be happy to join such meetings.

Maruti Suzuki – Leader in Passenger Vehicles (02-05-2024)

Maruti Suzuki –

Q4 concall and results highlights –

Revenues – 38471 vs 32214 cr

EBITDA – 5221 vs 3894 cr ( margins @ 14 vs 12 pc )

Other income – 1261 vs 850 cr

PAT – 3952 vs 2688 cr

Sales volumes – 5.84 lakh vs 5.14 lakh cars ( up 13.5 pc ). Export sales @ 78k vs 64k cars

EBITDA margins expansion led by – increased capacity utilisation, lower sales promotion expenses

Full yr sales volumes @ 21.35 vs 19.66 lakh cars ( up 9 pc )

Utility vehicles sales volumes grew by a whopping 75 pc @ 6.42 lakh cars in FY 24

Segments that de-grew include – Mini ( down 39 pc ) and compact ( down 4 pc )

Indian car mkt grew 8 pc YoY to cross 40 lakh car sales. India is now the third largest car market in the world

The shift in consumer preference towards SUVs continued in FY 24

The share of Hatchback segment is down to 27 pc, down from a high of 49 pc in FY 19

Share of CNG vehicles continues to rise. Now at 15 pc of total PV market !!!

EV and Hybrid cars currently at 2 pc mkt share each

Maruti Suzuki’s exports for FY 24 stood at 2.8 lakh cars. Company is also the largest car exporter from India. Exports grew by 10 pc YoY

Grand Vitaraa became the fastest car to clock 1 lakh car sales in the Industry

Company increased its solar power generation capacity from 26 MW to 43 MW in FY 24. Aim to take it to 48 MW in FY 25

Aim to cross 40 lakh cars / yr production target by 2030 ( almost double of current capacity )

CNG car sales for the company were around 4.5 lakh cars in FY24. Next yr, they are targeting a sales of 6 lakh CNG cars. Bulk of CNG sales come from Ertiga

First time buyers in FY 24 @ 43 pc of sales. Rest were replacement and additional car buyers

Committed to the Hybrid technology. Initially focussed on bigger cars like – Grand Vitara, Invicto. If volumes in these categories sustain, will invest in R&D to roll out Hybrid technologies in compact cars as well

Company did face supply challenges in the CNG segment in Q4 ( due some component shortage ) because of which some sales have been deferred. Current bookings / backlog of CNG deliveries stand at over 1 lakh vehicles – mostly Ertiga. Total – company level bookings currently stand at 2 lakh vehicles

Royalty payments to SUZUKI stand @ 3.5 pc of sales

Design – Launch timelines for new vehicles remain at 4 yrs

Disc: hold a small tracking position, biased, not SEBI registered

Ranvir’s Portfolio (02-05-2024)

Maruti Suzuki –

Q4 concall and results highlights –

Revenues – 38471 vs 32214 cr

EBITDA – 5221 vs 3894 cr ( margins @ 14 vs 12 pc )

Other income – 1261 vs 850 cr

PAT – 3952 vs 2688 cr

Sales volumes – 5.84 lakh vs 5.14 lakh cars ( up 13.5 pc ). Export sales @ 78k vs 64k cars

EBITDA margins expansion led by – increased capacity utilisation, lower sales promotion expenses

Full yr sales volumes @ 21.35 vs 19.66 lakh cars ( up 9 pc )

Utility vehicles sales volumes grew by a whopping 75 pc @ 6.42 lakh cars in FY 24

Segments that de-grew include – Mini ( down 39 pc ) and compact ( down 4 pc )

Indian car mkt grew 8 pc YoY to cross 40 lakh car sales. India is now the third largest car market in the world

The shift in consumer preference towards SUVs continued in FY 24

The share of Hatchback segment is down to 27 pc, down from a high of 49 pc in FY 19

Share of CNG vehicles continues to rise. Now at 15 pc of total PV market !!!

EV and Hybrid cars currently at 2 pc mkt share each

Maruti Suzuki’s exports for FY 24 stood at 2.8 lakh cars. Company is also the largest car exporter from India. Exports grew by 10 pc YoY

Grand Vitaraa became the fastest car to clock 1 lakh car sales in the Industry

Company increased its solar power generation capacity from 26 MW to 43 MW in FY 24. Aim to take it to 48 MW in FY 25

Aim to cross 40 lakh cars / yr production target by 2030 ( almost double of current capacity )

CNG car sales for the company were around 4.5 lakh cars in FY24. Next yr, they are targeting a sales of 6 lakh CNG cars. Bulk of CNG sales come from Ertiga

First time buyers in FY 24 @ 43 pc of sales. Rest were replacement and additional car buyers

Committed to the Hybrid technology. Initially focussed on bigger cars like – Grand Vitara, Invicto. If volumes in these categories sustain, will invest in R&D to roll out Hybrid technologies in compact cars as well

Company did face supply challenges in the CNG segment in Q4 ( due some component shortage ) because of which some sales have been deferred. Current bookings / backlog of CNG deliveries stand at over 1 lakh vehicles – mostly Ertiga. Total – company level bookings currently stand at 2 lakh vehicles

Royalty payments to SUZUKI stand @ 3.5 pc of sales

Design – Launch timelines for new vehicles remain at 4 yrs

Disc: hold a small tracking position, biased, not SEBI registered

Som Distilleries and Breweries (02-05-2024)

I agree too, Mr.Sethi wasn’t too open nor was he aware of the numbers to the extent that he was supposed. Coming to disclosing certain information which might pose a risk of competition, that is completely up to the company, If they feel that a figure like packaging cost is crucial they might choose not to speak about it. This is a standard practise.

Malhar’s Investing Thoughts (02-05-2024)

Have been studying BEW lately. Would love to discuss more on it.

Gurugram Valuepickr (02-05-2024)

I am also interested in F2F meeting.