That’s true that NBFC shouldn’t given such high valuation. But I a more concern with the difference in valuation between competitors. So, either IREDA or Bajaj valuation should come down or REC valuation should go up.

Posts in category Value Pickr

Astec Lifesciences (01-05-2024)

So now we have a Floor Price set for this scrip – INR 1,069.75 per Offer Share.

The open offer process will take 6 to 9 months to complete at the least.

HDFC Life Insurance Company (01-05-2024)

Last week I got a call from Yes Bank relationship manager trying to pitch some savings / investment scheme of HDFC Life

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (01-05-2024)

My take away from Q4’24 and FY’24 results:

Top Line Performance:

- 10.5% Y-o-Y growth (from 95 Crs. to105.42 Crs.)

- 11% Q-o-Q de-growth (from 118 Crs. to105.42 Crs.)

There can be different perspectives on recent quarter numbers, however, personally I am looking at the performance in context of few data points

- Management shared during last concall that a) they are running at 100% CU; b) had order book of 355 Crs. as on Jan’24.

- In current quarter results, a) margins are intact and rather improving; b) have inventory buildup of ~36 Crs.

So, to me, this Q-o-Q de-growth is worth checking with management in case there is a concall (not announced yet), however, in absence of a call, should not be a real alarming situation to act upon.

Margins:

Operating margins improved to 30% as against 27% last quarter and 22% same quarter last year. Just a conjecture, is it possible that they had a little higher share of export in the mix. As management informed last time, in export they have low complexity products with higher margin. That can be one of the reasons for comparatively lower top line however improved margins. May be, may be not.

Capex:: Phase 1 looks to be progressing little behind the plan. They had 1500 MVA addition at an expenditure of ~10 Crs. with a due date of commercial production starting April 1st. As per recent balance sheet ~1.7 Crs added to PPE and ~4 Crs CWIP. Is it not that current CWIP pertains to phase 1 only and has not really got added to PPE?

Balance sheet:

On a lighter note, they have also published Balance sheet and cashflow statement along with P&L. Why no one talking about that whereas that deserves at least some bit of discussion ![]()

Cash equivalent – Moved up by 25 Crs.

bank balance – moved up by 26 Crs.

Investments – addition of ~14 Crs.

Cashflow:

Cash from operations improved despite large inventory buildup (~35 Crs.) (partially offset by increased debtor days .) Net, ~2x cash from Operations.

To sum it up, the big picture view is that they are standing at ~1% of total domestic transformer capacity (domestic capacity is believed to be ~ 4,00,000 MVA). With capex, may go upto little less than 2%. Are predominantly into 66 KV class with some presence in 132 KV class. Segment that they are serving are mostly into renewables (primarily Solar) and are into distribution transformers only. Higher KV class and generation transformers are absolute white space for them as of now.

With such healthy margins, sturdy balance sheet and velocity of cash accumulation on books (even after factoring in the recent capex of 30 Crs.), I am slightly positive that management will enough elbow room in future, should the demand situations stays strong.

Disc: Invested, had transactions in last 60 days. Things may change as part of the risk mitigation strategy or for other reasons.

Thanks,

Tarun

ITC: “Will”(s) “Gold Flake” assist “Ashirwad” to win “Bingo!”? (01-05-2024)

| Common Size Without UAA | Mar-23 | Jun-23 | Sep-23 | Dec-23 |

|---|---|---|---|---|

| FMCG | 38% | 42% | 42% | 40% |

| Hotels | 22% | 20% | 20% | 20% |

| Agri Biz | 10% | 12% | 11% | 11% |

| Paperboards, Paper & Packaging | 24% | 22% | 21% | 22% |

| Others | 6% | 5% | 6% | 6% |

| Total | 100% | 100% | 100% | 100% |

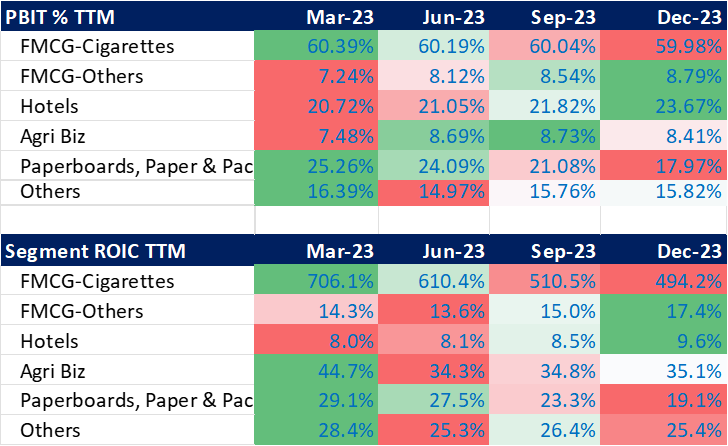

In FMCG-others segment, there is improvement in PBIT margins & ROIC.

Just making an attempt to understand the effect of demerger.

The above calculations are made using data from Segmental reporting.

Disclosure- Invested.

Krsnaa Diagnostics – what is the diagnosis? (01-05-2024)

New order for Krsnna for providing MRI and CT scan for govt. hospitals in 17 districts.

Ador Welding Ltd (01-05-2024)

More than that, yearly sales growth is only 4.76%. No management guidance on this.

Disc: invested, planning to exit if no proper reasoning provided by company.

ValuePickr Jaipur (01-05-2024)

Why don’t we start some sort of meetup at Jaipur?

Is it good if I mention fresh email-id here and those who are willing may write email to avoid spam.

Email id is: jaipurmeet2024@gmail.com

HBL POWER SYSTEMS: Booting-up for the Race of the Century (01-05-2024)

Which kind of batteries are these? I am assuming VRLA (lead acid) batteries. Haven’t heard of lead acid batteries lasting more than 4-5 years.