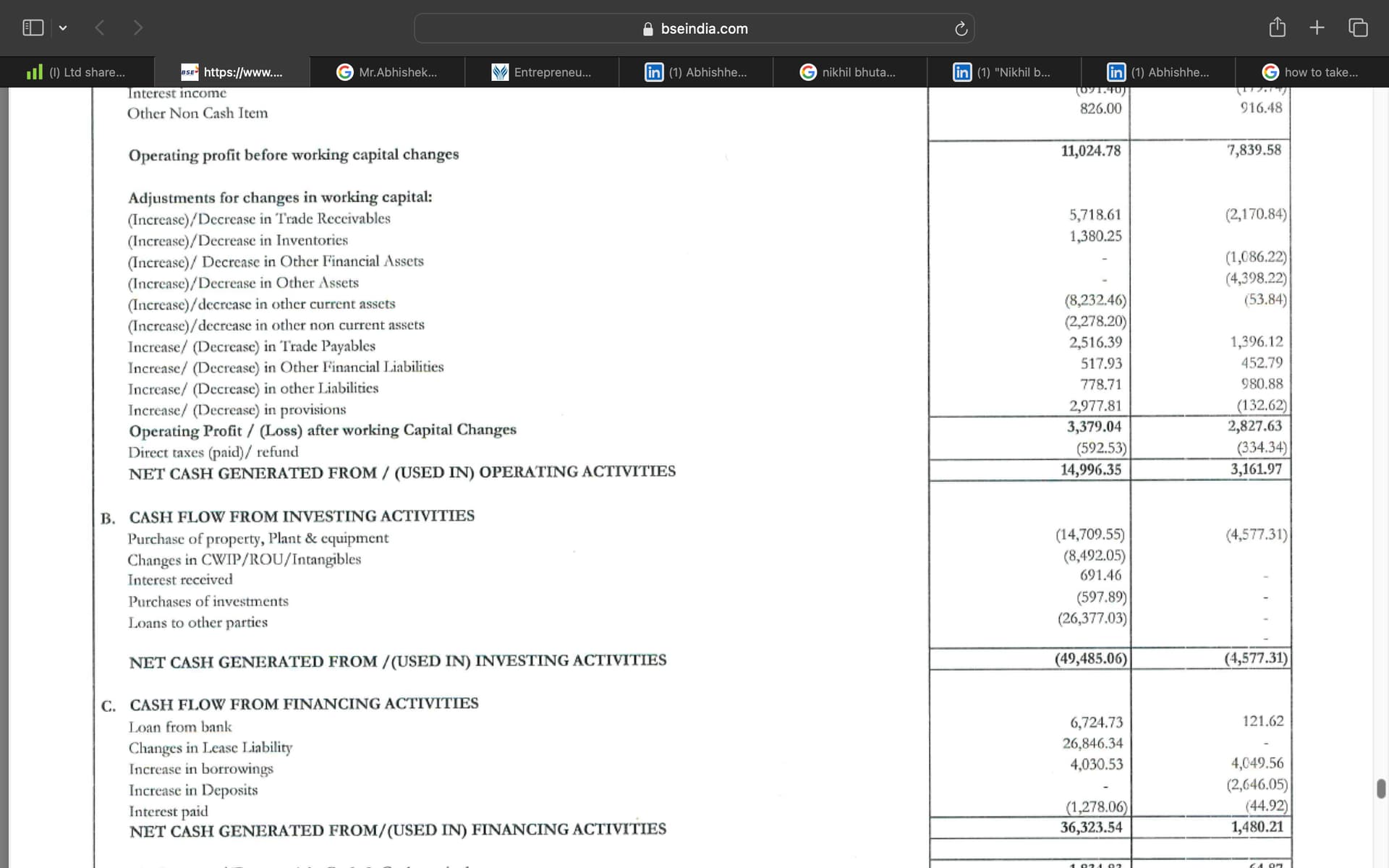

can someone help me to understand following 2 figures in cash flow statement of sept 24.

- loans to other parties – (26,377.03)

- Changes in Lease Liability – 26846.34

can someone help me to understand following 2 figures in cash flow statement of sept 24.

Sorry to keep coming with negative impressions and negative things. the management has not given rosy guidance for Q3 or Q4 either. All they are saying is it will be better than q2 25. Yhats obvious.

But consider that the credit environment is not benign and technology investments continue.

So profit will increase from Q2 25 Does not mean by any stretch of imagination that it will be more than Q3 24. in fact if you see the print of interviews it kinds of kind of hedge they are taking in their interviews, i have a bearish feeling about q3

it it only says it will be better than Q2 which is obvious.

We should not raise our expectations and scream later.

On a parallel note, I am frankly quite intrigued as to why so many of us are sitting and discussing this stock so much?

There are over 3000 posts here, no other bank is debated even remotely this much

Are we getting a vicarious pleasure going through the rough and tumble of this stock? And even more vicarious pleasure watching VV struggle with a bad purchase of a bank?

on one hand they are doing brilliant things on brand technology customer service smell image, deposits, improving ppop by 30 pc cagr, etc on the other hand ppop is not even 2.5%

admitted it has come from zero to 2.5 but still 2.5 is still low compared to indusind which is say 5% (but they dont command the good smell and stature of idfcfb)

we know very well it may ttake atleast 5 more years to even get to industry benchmarks

meanwhile big banks have already been through the rough and tumble during the last 2 decades and are sitting pretty with good roe

then why are we still stuck here debating everyday.

Why are we not simply switching away to a ICICI Bank get assured increase in book value and stay at price to book of 3.5?

Why stay with the bank which will make low Roe and bet that price to book will go up? should investors not just go and purchase peace?

Somewhere I feel we are getting a kind of thrill participating with this management’s rough and tumble. Or because of personality of vv is causing this odd kind of illogical attraction in this bank?

Or are we learning from a mysterious case where there are many positives and many negatives.

We are also probably getting a pleasure watching a successful entrepreneur buying a bank and watching him going through the rough and tumble of fixing his purchase.

If we sell out we wont have any interest in the debate. We are probably enjoying the struggle of a leader who is trying to turn around his debatable purchase?

At idfc we have to depend on a low 10 pc Roe bank increase its P/B from 1.3 to 2, if so,

53×1.1×1.12×1.13×1.145×1.16 =98…

am assuming modest numbers here, and not factoring bvps increase by raising capital at a premium if any.

for 20 pc growth 16 Roe good tech peace of mind governance bank)

At p/b of 2.5

98×2.5 =245 ( 245/ 67 = 3.6 x of todays money)

At 2x p to b, it would be 98×2 =196

196/ current price of 67 = 3x

Vs

in an icici we can be assured of high Roe

Their equation would be

136×1.17×1.17×1.17×1.17×1.17 = 855 … if they retain their 3.5 crown then their stock could be 855×3.5 = 2992 so stock would be 2.2 X of today

So which is more likely

A. idfc becoming Roe of 16 and reaching 2X or 2.5X p/b where we make 3x or 3.6 x our money? Or

B. icici Compounding bvps at 17 (roe) and retaining p/b at 3.5?

If we believe B is true we should switch out of our current position

If we believe B is true we should stop shouting and calling names getting frustrated with every bad result. We should trust the capability and intent of management and live with the rough and tumble that will come with this journey

If I am unfair or made logic error or mathematical error pls point out to me I am human

After all as of today, vehicle idfc is weaker franchise has low ppop has low roa low Roe

no matter how good or worlds best management it is, even if it is VV, he can only fix roa roe slowly over time. Because he has to constantly invest into every business and go through the J curve

Meanwhile the startup bank will have thinner skin, every small change in ecosystem, change in regulation will affect thr P and L and more will give heart attacks…

why are we self flagellating and going thru all this stress? Why are we not switching over to sy an icici and be more peaceful? Please educate our psychology so that we learn about ourselves.

Icici core vehicle is stronger, has been through its rough and tumble since 2000, and has reached roe of 17. More assured to deliver good growth in bvps. Retaining p/b at 3.5? Pls guide on the probabilities

Which is more likely? What is going on?

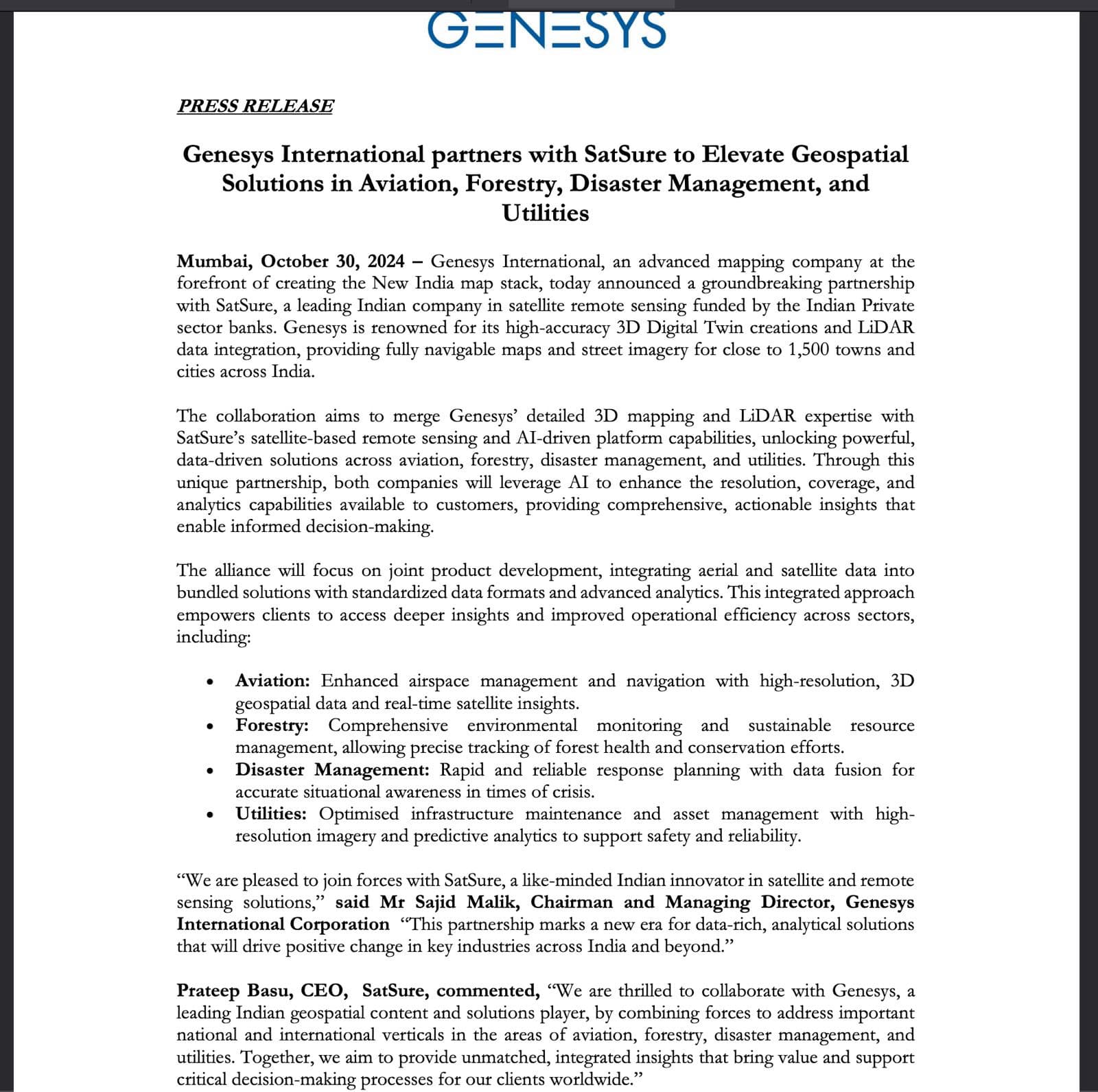

“The collaboration aims to merge Genesys’ detailed 3D mapping and LiDAR expertise with

SatSure’s satellite-based remote sensing and AI-driven platform capabilities, unlocking powerful,

data-driven solutions across aviation, forestry, disaster management, and utilities.”

Hi,

Thanks for highlighting most of the positives. However the real problem is the revenue itself. The slowdown in CV and tractor segment has impacted the sales and management expects the same to remain in near future. They have also curtailed some earlier planned investments. So no real revenue growth to be seen in near future.

And another major contributor in profit growth is optimization of internal controls like cost and production not from improving product mix only which is kind of one time event and cannot be improved beyond certain point.

In my view above points have resulted market disliking the result.

Thanks,

Deb

But they are not sure whether other value chain products will be under this company or other listed entity.

Can you please share the link sir @visuarchie .

At last company managed to post good results even in the tough grain inflatory environment by using some wet maize procurement at lower price in Q2, but it’s not the case in Q3.

Expecting crop in RJ, PN & JH which may cool off current maize price ~ 25/- to some extent.

As per management current margins can be sustainable in Q3 & Q4.

Capex:

75KLPD bio diesel plant can comission in Q1FY26.

150KLPD batinda expansion can be commissioned in Q3/Q4 FY26.

250KLPD Goyal distillery equipment finalization is under process, exact time line of comission can be known after equipment order placement. If ever thing goes well then we can get this on stream by FY26 end or else spill over to FY27. Funding route is yet to finalized for 350Cr acquisition.

From the current 700KLPD to 1175 KLPD by FY26 end or mid of FY27 i.e 68% jump in capacity in 1.5 to 2 Years.

Edible oil:

Exit from this segment could be Q4FY25/Q1FY26.

Even though top line would be impacted meaningfully 800-1000Cr but impact on the bottom line would be < 20Cr, which can be compensated by biodiesel plant.

WC finance cost would also decrease after exiting from the edible oil.

Over all down the line 5-6 quarters numbers would be similar to Q2 results, I am not expecting any good jump in numbers unless there is substantial reduction in maize price or increase in ethanol price . FY27 would be good year as all capacities would be on stream

can either of you share the correct video link of Rakesh Pujara please? Thx

Interesting article about the Wallenberg family who own / have stake in the likes of SAAB , ERICSSON, ASTRA ZENECA, ABB, SKF, ATLAS COPCO,EQT, NASDAQ among others. Corporate structure has strong parallels to our own Tata group.

They have been declared as the successful bidder. If they just bid for the hospital, they wouldn’t have issued a press release haha