The way Shilchar and TRIL are moving in tandem every day (5% Upper Circuit last few days) and today both at 5% Lower Circuit, without any apparent reason, I am beginning to feel these are operator driven? I know the long term story (at least till the end of the current cycle) is intact but this ‘every day circuit’ business looks a bit suspicious.

Posts in category Value Pickr

PVR Ltd.- Play on increasing disposable income (24-04-2024)

Disclosure: Invested

PVR Ltd.- Play on increasing disposable income (24-04-2024)

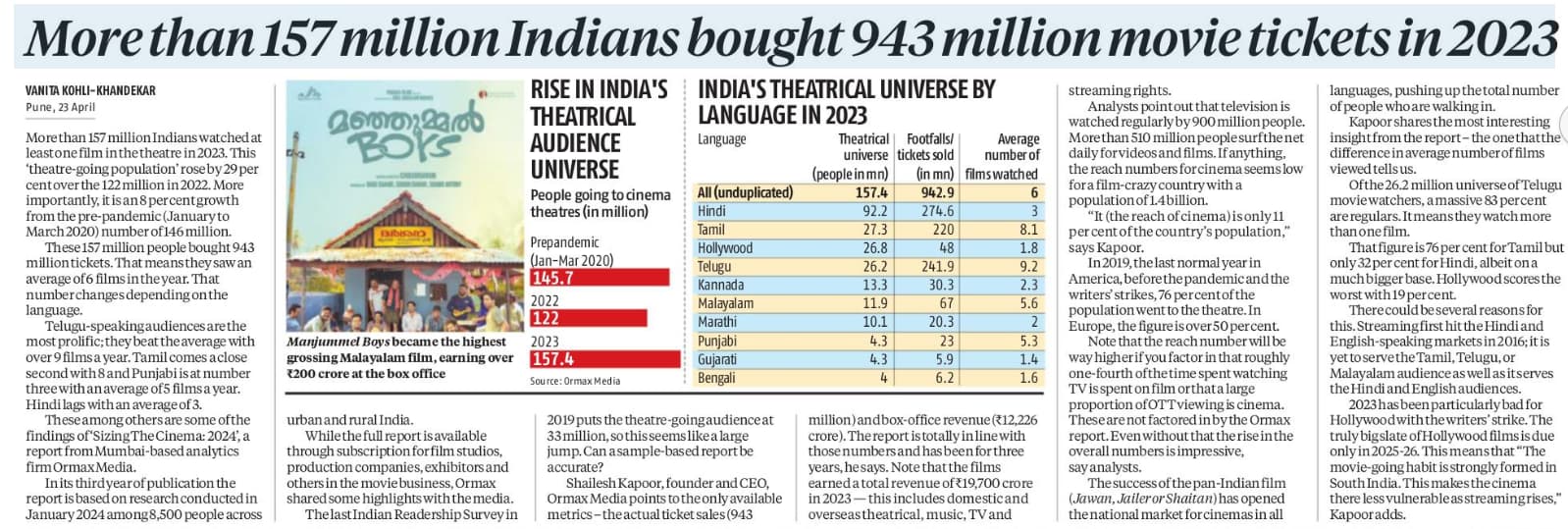

Relevant article with key data points. Looks like the content from Hollywood movies may not add much value in FY24-25. PVR’s strategy to therefore focus more on South aligns with the movie watching trend of South. Muted Hollywood content will therefore continue to challenge potential growth opportunities. Will Indian movie content alone uplift revenue opportunities?

Angel One: Metamorphosis into a Fintech? (Previously Angel Broking) (24-04-2024)

So then are we saying that the client funding book is the value of the shares pledged by the clients who do margin trading ? That figure is 1777 crores ?

MCX and Financial Technologies (24-04-2024)

Given the business model of MCX, one shouldn’t look at qoq numbers as top line will not always be linear quarter by quarter due to changes in market sentiments and volatility levels (in both equity and commodity) which in turn drive the volumes. Annual revenue growth is a better indicator of market participation which has been on a continuous uptrend.

Force Motors – racing ahead! (24-04-2024)

any idea where this export sales is coming from?

IPO Review – Discussion until listing (24-04-2024)

Emmforce Autotech Limited, a leading drivetrain parts manufacturer, is coming up with a SME IPO from April 23, 2024 to April 25, 2024.

Tune in as the founder and promoter Ashok Mehta shares insights about the company.

Exclusive Interview with the Chairman and MD of Emmforce Autotech – Mr. Ashok Mehta | SMEmitra

Hindustan Unilever (HUL) (24-04-2024)

All earnings are not same. Needs to be seen in context of cash flow as well as return ratios.

At end of the day any business needs to valued only on basis of all cash flows till eternity.

Most of the valuation of a company is dependent on terminal value. Something like L&T EPC would start seeing a lot of degrowth a decade down the line vs HUL. India’s population is likely to remain around current population till end of century thus providing long runway for FMCG companies.

Hindustan Unilever (HUL) (24-04-2024)

Thanks for the details & your perspective. Last I had checked, current PE is around 50 for HUL. I maybe wrong.

Again, I have some doubts although cannot say for sure, but HUL was around 50 since a long time.

Regarding NIFTY PE vs HUL PE…I think in addition to EPS CAGR, what matters is the longevity & relative surety with less relative risks & variables for achieving that EPS CAGR.

I am not justifying the high PE nor have any opinion about it…just trying to see that if a relatively risky infra/defence/cement/power etc. can trade at “x” valuation, what can an FMCG trade at.

Of course with digital era there have been disruptions in terms of D2C, retail private labels & ecommerce…this is according me a defining decade in progress for what will be about to come…whether the delta to X would sustain or not…how rural, rurban & urban would behave and which FMCG firms are able to work their way around it & how soon & how efficiently…

INOX Wind (24-04-2024)

This is not an NCLT approval order. Steps 4/5 have been initiated, approval is step 15.