I used to follow same strategy only to realize that during Bull Market Idea should be to Buy at High P/E and Sell at higher. learnt this from Hitesh Sir @hitesh2710

Missed Solar Industries\Data Pattern\HBL due to this

Posts in category Value Pickr

Pragnesh’s portfolio (23-04-2024)

Pragnesh’s portfolio (23-04-2024)

I usually avoid stocks with P/E ratio>35

So, i think all above stocks except carysil are good buy at present.

You can also add

Lt foods

Grauer and weil

Pitti eng

Racl

Intense Technologies (23-04-2024)

This looks like a V Shape Recovery to me on M-o-M chart to me. Any thoughts on this recovery. Seems like a long term breakout.

Elecon Engineering Limited (23-04-2024)

Elecon provides solution to companies which are cyclical in nature steel, cement , capital goods. Growth can be very high for a couple of years followed by low growth / over capacity into these sectors. We are currently in the cycle of high growth it may last for 2-3-5 years or more no one knows. 2 years visibility is something one can have from economy perspective . With time going by further clarity will emerge. For me frankly since first buy @150 elecon has suprised quarter on quarter since last 3 years I did add post good results around 200 & topped up @370

.I continue to scout for better opportunity and may exit / trim / hold basis situation demands. Currently among top 3 holding for me

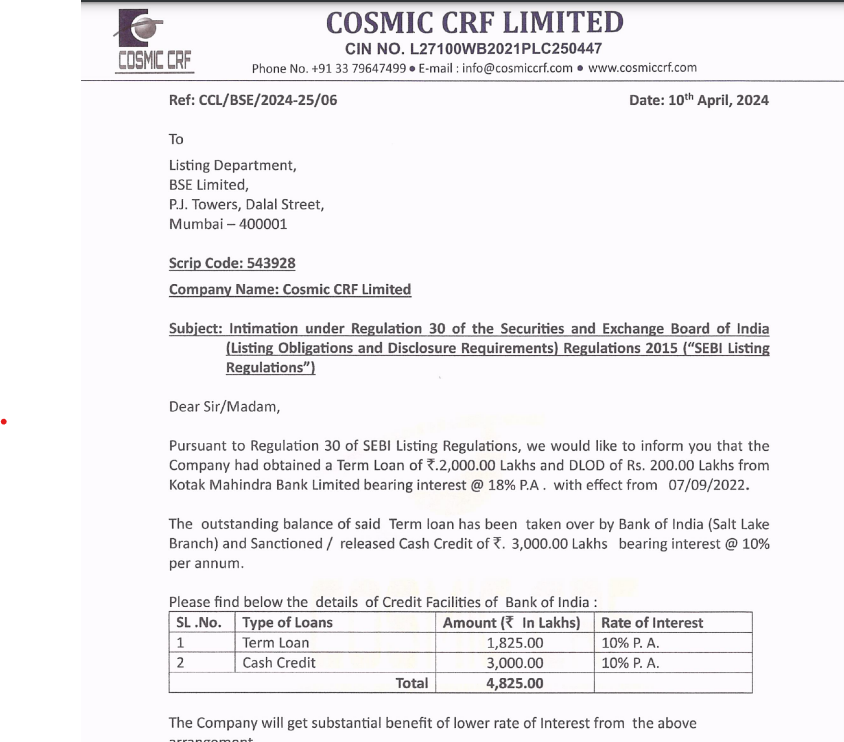

COSMIC CRF LIMITED – sme (23-04-2024)

Beneficial move by company.

Good move reflects in next result.

Amoul Portfolio (23-04-2024)

Their primary business is to tie up airport services and bundle them together in a package, and partner with banks to offer these bundled services to bank customers. They are coming with their own card-based loyalty program as well.

Motilal Oswal Initiated coverage recently you can read more about it here: https://ftp.motilaloswal.com/emailer/Research/DREAMFOL-20240227-MOSL-IC-PG032.pdf

Apollo Tyres- Do not understand the valuation (23-04-2024)

Althought very new to this sector but, across the sector the margins are around previous peak’s. From Sep 22 margins started moving upwards on the back of easing R.M prices.

Now R.M prices are moving upwards, so let’s see whether this margins sustains or not.

MCX and Financial Technologies (23-04-2024)

with new software platform stable and traded amount going up Historical Data MCX is expected to do good on earning front . infact fy25 might be best year till now

Meghmani Finechem – Underrated multibagger? (23-04-2024)

Yes, you are saying right. What I observed from analysing this company is that growth will come from the new project because Asset Turnover ratio is just 1.4x. to grow from here management have to announce new capex plan for new product or further expansion plan of the current, this will drive the revenue of the company. And in margin front we should expect 28% margin sustainable basis as guided by the management in the previous con calls. We should also see that Maulik has increased his holding by 0.11%. It shows that management has confidence in their future plans.

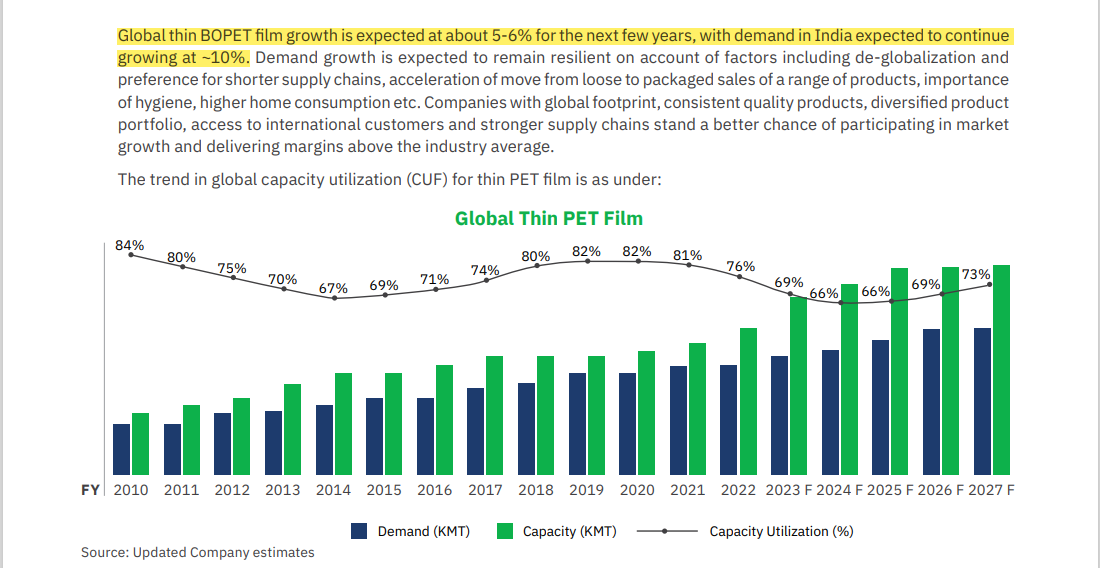

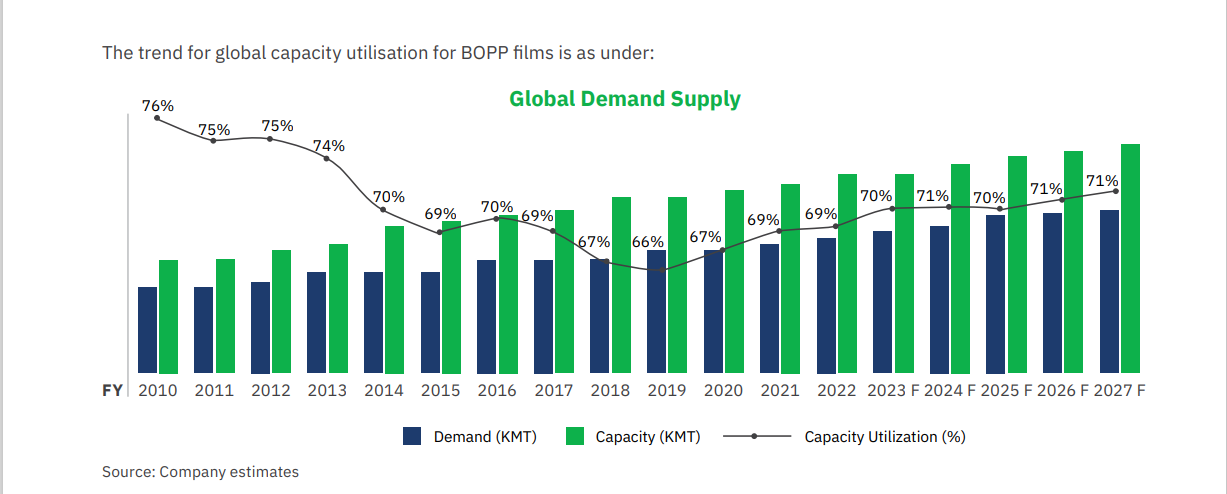

“Polyplex Corporation “ Are Good Days Ahead? (23-04-2024)

Wanted to undesrand how Supply-Demand looks going ahead, found this from Polyplex A.R, But this data is from A.R Of FY 2023.