Dlink Q2 Numbers

Rev at 336cr vs 308cr,

Q1 at 346cr PBT at 35cr vs 31cr,

Q1 at 35cr PAT at 27cr vs 24cr

OCF at 5cr vs 42cr

Dlink Q2 Numbers

Rev at 336cr vs 308cr,

Q1 at 346cr PBT at 35cr vs 31cr,

Q1 at 35cr PAT at 27cr vs 24cr

OCF at 5cr vs 42cr

@visuarchie

Hi Sir,

Do you have any strategies other than momentum?

If you have any ideas as well, please do share will try to build the system.

@visuarchie

Hi Sir,

Do you have any strategies other than momentum?

If you have any ideas as well, please do share will try to build the system.

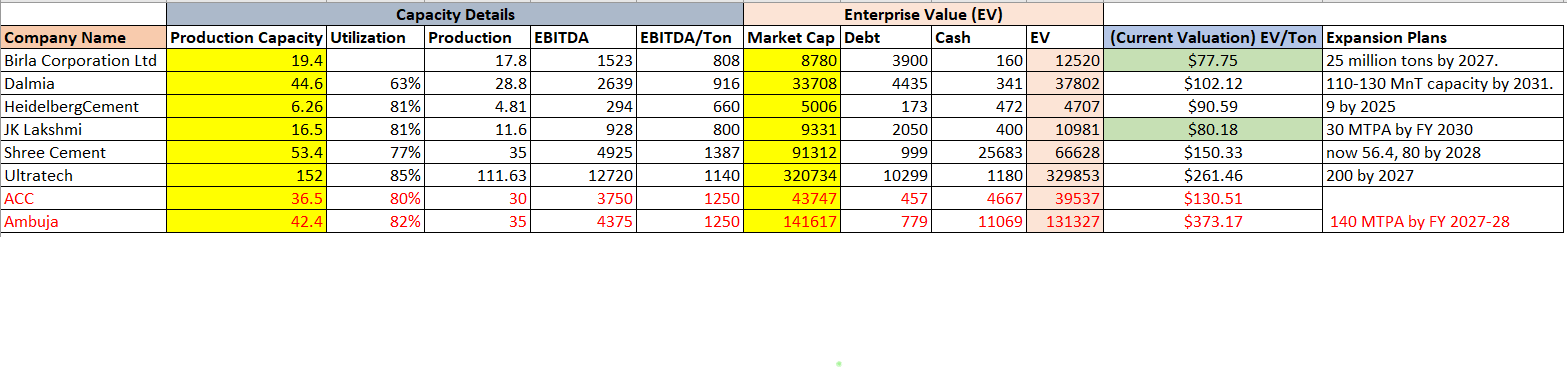

Total Installed Cement Capacity for 2024: 16.5 million tons, including Udaipur Cement Works Limited.12

% of Revenue from Cement for 2024: The sources don’t explicitly state the percentage of revenue from cement, but they heavily imply that it constitutes the vast majority. The company is referred to as a “leading manufacturer and supplier of Cement and Cementitious products” and there is extensive discussion on cement production and sales, with limited mention of other product lines.34

Utilization Rate for 2024:

JK Lakshmi Cement: 81%

Udaipur Cement Works: 80%

Production for FY 2024:

Clinker Production:

JK Lakshmi Cement: 6.996 million tons8

Udaipur Cement Works: 1.975 million tons8

Cement Production:

JK Lakshmi Cement: 9.51 million tons

Udaipur Cement Works: 2.097 million tons for the full year, with 6.42 million tons in Q411

EBITDA for FY 2024: Rs. 928 crore12

EBITDA per ton in 2024: While the provided annual report doesn’t state the precise EBITDA per ton figure, it highlights achieving Rs. 1,000 EBITDA per ton for two consecutive quarters.13

Total Debt from the balance sheet for 2024 annual report:

Standalone: Rs. 700 crore14

Consolidated: Rs. 2,050 crore14

Total Cash & Cash Equivalents from the balance sheet for 2024 annual report:

Standalone: Rs. 375 crore14

Consolidated: Rs. 400 crore14

Capacity Expansion Plans and Timelines

Durg Expansion:

A new clinker line with a capacity of 2.3 million tons per annum (MTPA) will be added at the Durg integrated unit.15

Grinding units with a total cement capacity of 4.6 MTPA will be added, including 3 split location grinding units and 1 at the integrated plant.1516

Estimated cost: Rs. 2,500 crore1516

Targeted commissioning: By March 202715

Phase 1: Clinkerization and a grinding unit at Durg, and a grinding unit at Prayagraj, Uttar Pradesh, to be commissioned by the last quarter of FY 2026.1617

Surat Grinding Unit Expansion:

Capacity doubling from 1.5 million to 2.7 million tons.18

Phase 1: 0.7 million tons to be commissioned in October 2024.19

Phase 2: Remaining capacity to be commissioned by March/April 2026.19

Split Location Grinding Units:

Three units planned, with a total cement grinding capacity of 3.4 MTPA.20

Locations: Prayagraj in Uttar Pradesh, Madhubani in Bihar, and Patratu in Jharkhand.20

Timeline: Not specified in the sources.

Northeast Expansion:

Estimated cost: Rs. 1,800 crore, including Rs. 1,500 crore for the project and Rs. 300 crore as a balance payment for the acquisition.21

Capacity addition: 1.5 million tons.22

Timeline: Expected to start from FY 2027 onwards.22

Agrani Cement Expansion:

Timeline: Dependent on obtaining environmental clearance and completing land acquisition. Expected to be operational by March/April 2027.23

Overall Capacity Target: The company aims to reach a consolidated capacity of 30 MTPA by FY 2030-2033.1824

Recent Developments from Conference Calls

Cost Saving Initiatives:

The sources don’t mention specific cost-saving initiatives, but they highlight that JK Lakshmi Cement Ltd. is known as one of the least-cost producers of cement in the industry.25

The company is focused on increasing Thermal Substitution Rate (TSR) and Alternative Fuel Rate (AFR) usage to reduce reliance on conventional fuels and lower costs.17

Current Valuation: Fairly valued with $80 EV/ton

Total Installed Cement Capacity for 2024: 16.5 million tons, including Udaipur Cement Works Limited.12

% of Revenue from Cement for 2024: The sources don’t explicitly state the percentage of revenue from cement, but they heavily imply that it constitutes the vast majority. The company is referred to as a “leading manufacturer and supplier of Cement and Cementitious products” and there is extensive discussion on cement production and sales, with limited mention of other product lines.34

Utilization Rate for 2024:

JK Lakshmi Cement: 81%

Udaipur Cement Works: 80%

Production for FY 2024:

Clinker Production:

JK Lakshmi Cement: 6.996 million tons8

Udaipur Cement Works: 1.975 million tons8

Cement Production:

JK Lakshmi Cement: 9.51 million tons

Udaipur Cement Works: 2.097 million tons for the full year, with 6.42 million tons in Q411

EBITDA for FY 2024: Rs. 928 crore12

EBITDA per ton in 2024: While the provided annual report doesn’t state the precise EBITDA per ton figure, it highlights achieving Rs. 1,000 EBITDA per ton for two consecutive quarters.13

Total Debt from the balance sheet for 2024 annual report:

Standalone: Rs. 700 crore14

Consolidated: Rs. 2,050 crore14

Total Cash & Cash Equivalents from the balance sheet for 2024 annual report:

Standalone: Rs. 375 crore14

Consolidated: Rs. 400 crore14

Capacity Expansion Plans and Timelines

Durg Expansion:

A new clinker line with a capacity of 2.3 million tons per annum (MTPA) will be added at the Durg integrated unit.15

Grinding units with a total cement capacity of 4.6 MTPA will be added, including 3 split location grinding units and 1 at the integrated plant.1516

Estimated cost: Rs. 2,500 crore1516

Targeted commissioning: By March 202715

Phase 1: Clinkerization and a grinding unit at Durg, and a grinding unit at Prayagraj, Uttar Pradesh, to be commissioned by the last quarter of FY 2026.1617

Surat Grinding Unit Expansion:

Capacity doubling from 1.5 million to 2.7 million tons.18

Phase 1: 0.7 million tons to be commissioned in October 2024.19

Phase 2: Remaining capacity to be commissioned by March/April 2026.19

Split Location Grinding Units:

Three units planned, with a total cement grinding capacity of 3.4 MTPA.20

Locations: Prayagraj in Uttar Pradesh, Madhubani in Bihar, and Patratu in Jharkhand.20

Timeline: Not specified in the sources.

Northeast Expansion:

Estimated cost: Rs. 1,800 crore, including Rs. 1,500 crore for the project and Rs. 300 crore as a balance payment for the acquisition.21

Capacity addition: 1.5 million tons.22

Timeline: Expected to start from FY 2027 onwards.22

Agrani Cement Expansion:

Timeline: Dependent on obtaining environmental clearance and completing land acquisition. Expected to be operational by March/April 2027.23

Overall Capacity Target: The company aims to reach a consolidated capacity of 30 MTPA by FY 2030-2033.1824

Recent Developments from Conference Calls

Cost Saving Initiatives:

The sources don’t mention specific cost-saving initiatives, but they highlight that JK Lakshmi Cement Ltd. is known as one of the least-cost producers of cement in the industry.25

The company is focused on increasing Thermal Substitution Rate (TSR) and Alternative Fuel Rate (AFR) usage to reduce reliance on conventional fuels and lower costs.17

Current Valuation: Fairly valued with $80 EV/ton

Source: Axis Securities

Skipper is doing a fund raise of 600Cr so essentially, they are going to be debt free post fund raise which means earlier they were paying high interest costs(50% of EBIDTA) which will now flow directly to bottomline also capex can be funded through internal accruals, reduction in working capital cycle means less money stuck in inventory and receivables and thus no need of bill discounting . Now as pace of order execution increases their margins can expand to 11% due to operating leverage.

Source: Axis Securities

Skipper is doing a fund raise of 600Cr so essentially, they are going to be debt free post fund raise which means earlier they were paying high interest costs(50% of EBIDTA) which will now flow directly to bottomline also capex can be funded through internal accruals, reduction in working capital cycle means less money stuck in inventory and receivables and thus no need of bill discounting . Now as pace of order execution increases their margins can expand to 11% due to operating leverage.

Good results posted today by Kitex, Net profit 37 Crs compared to 27 Cr in Q1 and 13 Cr yoy… if Q2 is this good then Q3 Dec quarter should be blockbuster…lets see…

Total Installed Cement Capacity for 2024 : HeidelbergCement India Limited’s total cement grinding capacity stands at 6.26 MTPA as of the end of FY24.12

% of revenue from Cement for 2024 : Approximately 98% of revenue came from cement sales. This is calculated by dividing cement sales by the total revenue from products: 21,570.1 / 22,009.5 = 0.98.3

Utilization rate for 2024 : The sources indicate that HeidelbergCement India was “almost running at 80% plus capacity utilization” in FY24.4

Production for FY2024 : The company sold 4.81 million tonnes of cement & clinker in FY24.5

EBITDA for FY2024 : EBITDA for FY24 was INR2,941.4 million (including other income).6

EBITDA per ton in 2024 : The company reported EBITDA of INR659 per ton, a 16% year-on-year increase.7

Capacity Expansion Plans :

Clinker Debottlenecking Project : This recently announced project in Central India will increase clinker capacity to 3.3 million tons, resulting in an additional cement volume of 200,000 tons per annum. It is expected to be completed in Q1 of the 2025 calendar year.789

Gujarat Expansion : Plans for a grinding unit expansion in Gujarat are on hold pending environmental clearance (EC) from the government.1011 The company has not announced a timeline for when it expects to receive the EC.10

Total Debt from the balance sheet for the 2024 annual report : Total debt from the balance sheet is INR1,737.8 million. This is calculated by adding the non-current borrowing amount and the current portion of the non-current borrowing: 1,108.3 + 629.5 = 1,737.8.12

Total Cash & Cash equivalents from the balance sheet for the 2024 annual report : Total cash and cash equivalents are INR4,729.1 million.12

Recent developments from conference calls, including cost-saving initiatives, capacity expansion initiatives with timelines and milestones :

Cost-Saving Initiatives : The company is focusing on cost reduction and improvements in efficiency parameters.13 Specific cost-saving measures mentioned include:

Alternative Fuels (AF) : HeidelbergCement India is continuing to invest in alternative fuel projects to optimise variable costs and reduce carbon content. They are currently in the third phase of these projects.14

Green Power : The company has signed a long-term Hybrid PPA for 8 megawatts Wind and 8 megawatts Solar, which will start in the current quarter (likely Q2 FY25). They expect this to reduce power costs by around 30-35%.15

Capacity Expansion Initiatives :

Clinker Debottlenecking Project : See above for details.

Gujarat Expansion : See above for details.

The management stated that they would only hold conference calls once a year unless there was something substantial and material to announce.

currently decently valued at $90 EV/ton.

(post deleted by author)