Please find below the links for the recent con call.

Just Dial Q4 FY24 Earnings Call | Just Dial Limited FY24 Q4 Concall

Hope you find them useful

dr.vikas

Please find below the links for the recent con call.

Just Dial Q4 FY24 Earnings Call | Just Dial Limited FY24 Q4 Concall

Hope you find them useful

dr.vikas

Yes they have good order book , but they don’t give any guidance, so difficult to anticipate numbers for forthcoming quarters.

And trading at such multiples, if even growth slows gradually in forthcoming quarters stock may give steap correction.

Looks intresting but kind of afraid to build positions at this multiple

EPIGRAL LTD PERFORMANCE NOTE FOR Q4 FY24 DOWNLOAD FROM THIS LINK.

THIS IS JUST FOR EDUCATIONAL PURPOSE.

DISCLAIMER: I AM NOT A SEBI REGISTERED RESEARCH ANALYST/ADVISOR.

Team – After having gone through the Persistent Systems results and listening to the Earning Conf Call I am sharing my perspective on the results and the stocks price volume action today.

Business Performance – I see no issues in the execution by the management and company. The results have been very much in line with what has been the recent trend and expectations. In fact, I see no sign of any gloom or doom in the management commentary in contrast to the Persistent’s larger peers.

About Margins guidance going forward – The Management is indicating that the anticipated margin growth of 200-300 bps will take longer than expected. They maintain that the goal is to reach those goals in the next 2-3 years. They clearly anticipate pressure on margins and growth in the market due to macroeconomic and geo-political issues but would like to prioritise growth in FY 2024-25. Hence rather than take a hit on lower growth to maintain margins they are guiding that in FY25 they would like to prioritise growth.

Larger transformative deals they are winning involve higher upfront transition costs and require hiring of people in proximate Onshore / customer locations. The margins from these wins will improve as resourcing mix moves to more of offshore (India-based) resources.

4.They continue to spend more and double down on Sales & Business Development, travel and hiring management & business leadership talent to scale growth. This may be impacting the margins currently but, in my opinion, this is spending for the right reasons.

Stocks Price Volume action today – Persistent Systems has been no doubt an Expensive Performer compared to its peers. Many in the market who are impatient about growth and margins did not like the Management’s guidance on prioritising growth over margins in FY25, so that set of investors sold out today. Also given that the price went down by up to 10% during the day investors like me who follow automated trailing stop loss triggers got dragged along. Today was a day for a correction of markets expectations. Depending on how one sees their position in this stock – as a Investor / Trader, it is up to you to take a view and follow your systems in a disciplined manner.

Right now, I do not find any reason for concern apart from street’s built up expectations of a clockwork like progress on margin improvement and sales growth to target $2 Bn likely getting delayed.

Let us look for commentary from Analysts who track this stock closely for any other red flags or concerns before taking a view on next steps.

Once again, the usual disclaimers apply – I am not a registered analyst or investment advisor. This is not investment advice. Do your own analysis and be responsible for it.

Not a one-off. They have a huge order to fulfil in the next year.

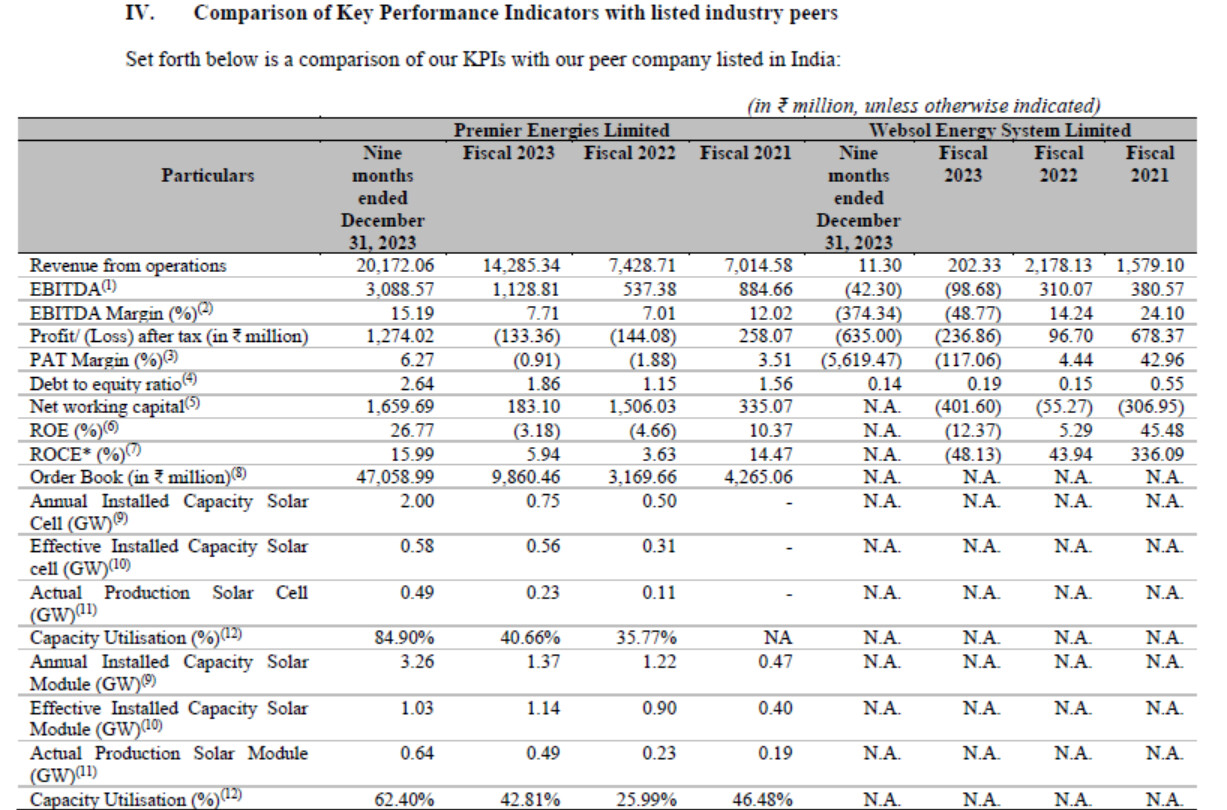

One more DRHP from another company which has presence in Cell + Module manufacturing compares KPI’s with Websol Energy. India made Solar Cell is the hottest commodity in the world now.

The Cephalosporin capex (it was small I think but don’t remember the numbers) was announced in FY22. Apart from that company has not undertaken any major capex in the last few years.

There’s a thread already existing on this.

We may take up the discussion on Swiss Military here.

The company has completed the expansion of its Cephalosporin plant in Mehsana, Gujarat, and has commenced commercial production, with sales initiated in domestic markets. Plans are underway to register the product for export to multiple countries. Cephalosporin Plant is expected to contributed sales of around Rs.150 crore in next 3 years.