Here is the latest investor presentation by JustDial

https://www.bseindia.com/xml-data/corpfiling/AttachLive/aaf155c8-d501-413a-998b-36fbc96f3b1b.pdf

Hope you find it useful

dr.vikas

Here is the latest investor presentation by JustDial

https://www.bseindia.com/xml-data/corpfiling/AttachLive/aaf155c8-d501-413a-998b-36fbc96f3b1b.pdf

Hope you find it useful

dr.vikas

You can’t really value a aggressively growing company with an existing metric. If you do, it always looks like overvalued.

That is why you look outside the company and how it impacts future of the company(revenues, sales etc)

Superb results again

for a company which is

99% dependent on service fees charged from customers, and all revenue only from Airlines

Losing market share the moment they started charging service fees

Easemytrip will have disastrous Q4 results, would be losing market share.

I think we are few decades away from that situation, with much smaller economy and long runway for growth.

Me too. This is risky

Nothing to write home about in the price action for the moment, positive or negative. I don’t think think they would have disclosed pre sales numbers at the meet. I think the Q4 pre sales of 678cr is decent, albiet slightly lower than the projection. Lower collections is not ideal, and hopefully will pick up in Q1. Will have to be tracked.

I’m most interested in whether the Naigaon rveenues reflect in Q4 or if we have to wait for longer. Right now I think the stock will perform when general retail perception improves as it has a relatively low free float, and retail perception deoends largely on reported P&L numbers.

I’m waiting, and adding on dips to 400.

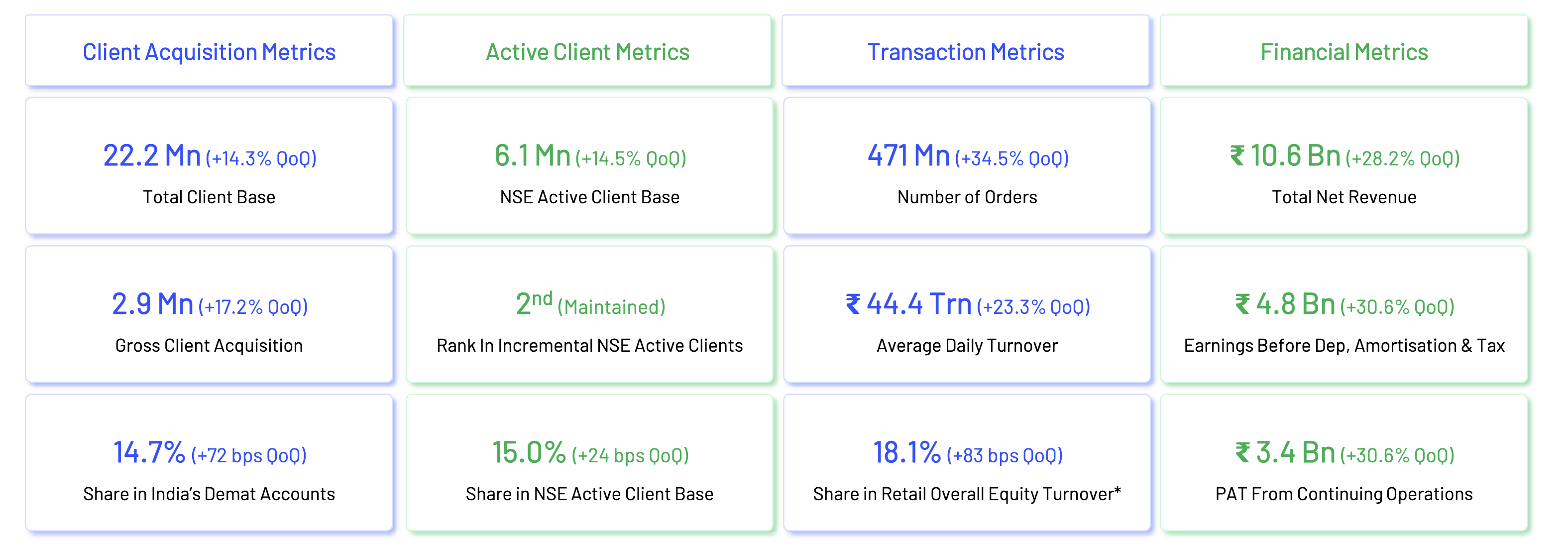

In there investor presentation, they say that they stand 2nd Rank In Incremental NSE Active Clients.

Do we know who is the first? Also are there any public and listed digital brokerage firms like Angel?

Hey @thakurvi

Like most on here its been a good run so ive nothing to post really. Ive held strong through the drawbacks and rises… Only major change is im no longer putting money into small or mid caps but targetting the large safe laggards… as mentioned above ive built a big position in hdfc bank. Since then ive been building positions in Kotak, Sbi cards and HUL near 52 week lows for both me and my wifes PFs. With HUL especially Im hoping i get atleast a year to build a huge amount at these valuations with a nice dividend of around 2 percent as a bonus. Can see some really good safe , low downside moderate low teens cagr long term here. Some good compounders available for cheap at present but i dont track infosys