https://edition.cnn.com/2024/04/03/business/egg-prices-cal-maine-bird-flu/index.html

Posts in category Value Pickr

Supriya Lifescience Ltd – pure play API (10-04-2024)

Although, salaries more than stipulated limits can be paid by Special Resolutions, I will take above info as some negative flag for higher valuations and can be monitored as company progresses.

Nitta Gelatin India Ltd | A turnaround story (10-04-2024)

The alternatives to conventional sources of gelatin will not easily replace the animal source because (1) Vegetable sources are far less nutritional than animal/fish sources. The vegetable source is relatively low in vitamins and essential nutrients. (2) The application needs specific preparation. (3) They cost 3 times that of Gelatin from animal and fish sources.

Va Tech Wabag (10-04-2024)

Why is the promoter holding so low at 19%?

Please can someone shed some light on this.

Also, what is the market share between Wagah & EMS would anyone know?

Thank you

CAMS – Indirect Bet on Financialization? (10-04-2024)

CAMS gets RBI approval to operate as an online payment aggregator.

Common Man’s Portfolio (10-04-2024)

Portfolio Update and Allocation

Exits: Sold Dycons Systems after quick 28% Profit

- Credit Access(25%) After Fall in Price % has come down but haven’t sold single Share

- Shri Ram Piston(17%)

- CEInsystech(11%)

- Shivalik Bimetal(10%)

- BBL(8%)

- Nesco(5%)

- AMI Orga(4%)

- SKM Egg(4%)

- PREvest (2%)

- Intellect(2%)

- CIE Auto(2%)

- Titagarh(1.5%)

- Manorama(1.5%)

- Ganesh Benz(1.5%)

- Arham(1.5%)

- PECOS(.7%)

- Fine Org(.7%)

- Frontier Springs(.7%)

- HSIL (.7%)

- IMFA (.6%)

- Shivalik Rasayan(.2 %)

India-Middle East-Europe Shipping and Railway Connectivity Corridor: The Route to Riches (10-04-2024)

Nice analysis regarding the involvement of Indian companies. Towards construction involved in various activities, ACE, Hercules Hoist and Escort Kubota etc may be considered. Tiger logistics is the preferred logistic company for co- coordinating passage through sea, especially Defense load as seen in the recent past. The owner hails from Defense background and has availed the connections for access into the market. Armenia as of now is relying on Indian defence systems and in the future Greece

Common Man’s Portfolio (10-04-2024)

Hello, would you be able to update portfolio allocation in each of these stocks?

Indigo Paints: Upcoming Star (10-04-2024)

Hi, I came across the company recently, went through the concalls/PPTs and below are my observations.

The super high valuations of the company at the time of the IPO has not held up, and the current price has gone below IPO price and profits have increased, thus making the company relatively cheaper, hence attracted my interest.

The co. is growing ahead of the industry, margins have improved and now there is little headroom for margins to improve from here, based on A&P spends. If they continue to grow ahead of the industry, and A&P spends grow at lesser rate, then some benefits will show up in the EBIDTA, and the co. expects that it could reach 20% EBITDA margins next year. Currently their margins are second best, slightly behind Asian Paints.

The company has finished the TN capex and initiated the Jodhpur capex. Their strategy of focusing on 750 cities has resulted in growth. The mgmt is expecting to finish the year (FY24) around 1350 Cr, this is 25% growth over last year. And next year they are targeting to grow beyond 25% (their target is to grow between 30-40%), provided industry grows to its pre-pandemic levels of around 8-10%. The co. is expecting Apple Chemie also to grow to 55-60Cr, and very bullish on the subsidiary outperforming going forward.

The mgmt has, multiple times, alluded to reaching closer to #2 and #3, and if from Fy24, they grow 5x they would still not be #3 by 2029, they will be less than 7000Cr topline. Assuming they maintain their margins (10% NPM), and assuming PE multiple of 40, the mcap could reach 28,000Cr, that would be over 4x from current levels in 5 years (32% CAGR).

The triggers are:

- Focus on 750 cities, increasing the tinting machines, increasing per dealer business, increasing engagement with influencers in these 750 cities

- Foray in projects business

- Foray in retail waterproofing segment

- Taking Apple Chemie’s waterproofing and construction chemicals business to PAN India level from a single state of MAH at the time of acquisition.

A big question is, will the company be able to grow as per its own expectations.

Another big risk to this thesis, and connected to the above risk will be, how Grasim executes its plan. There are fears that Grasim will alter the industry structure significantly and historical profits/returns earned by the incumbents will reduce. If that plays out, then all the parameters like growth, margins, multiples will reduce for the current players and above thesis will fail.

Disc: not invested, but interested

Chatha Foods – A proxy play for QSR (10-04-2024)

About Chatha Foods Limited

(Ref:chittorgarh.com)

Incorporated in 1997, Chatha Foods Limited (CFL) is a frozen food processor. The company offers frozen food products to top QSRs (Quick Serving Restaurants), CDRs (Casual Dining Restaurants), and other players in the HoReCa (Hotel-Restaurant-Catering) segment. Chatha Foods’ product portfolio includes Chicken Appetizers, Meat Patties, Chicken Sausages, Sliced Meat, Toppings & Fillers and more. The company produces more than 70 meat products.

The company sells products under the brand Chatha Foods and distributes through the network of 29 distributors covering 32 cities across India and catering to the needs of 126 mid-segment & standalone small QSR brands.

Chatha Foods Limited has a Manufacturing Facility, located in District Mohali, with a production capacity of approximately 7,839 MT for all the frozen food products.

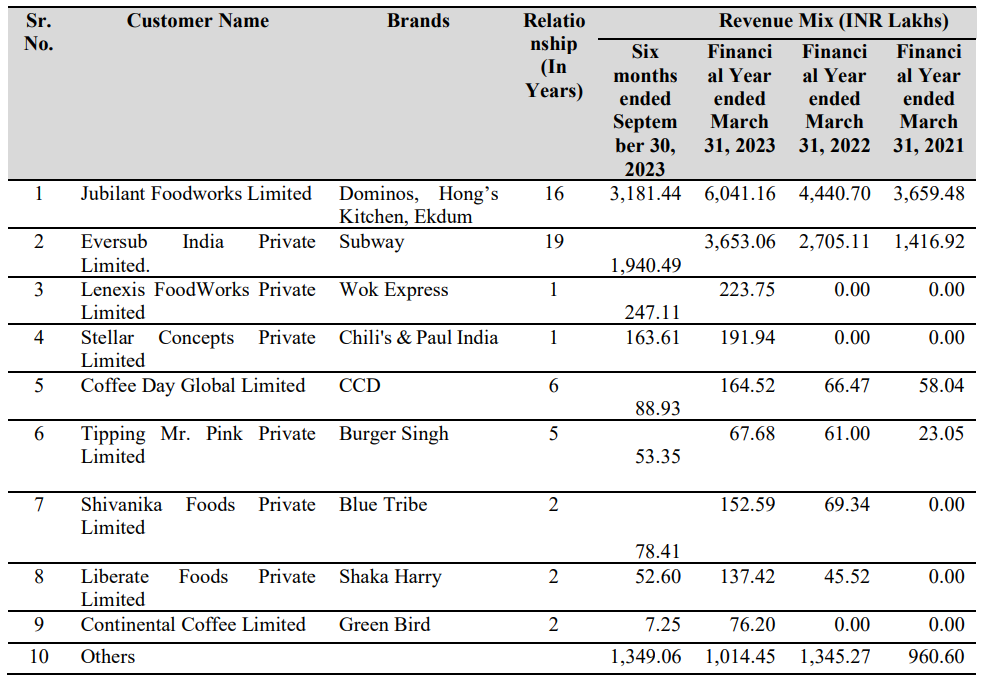

The company is serving top QSRs, CDRs and other players in the Hotel-Restaurant-Catering segment like Domino’s & Subway’s India franchise, Café Coffee Day, Wok Express, etc.

The company does not have any subsidiaries or any Group Companies.

Big Investments

- Negen Undiscovered Value Fund → ~10.43%

- Persistent Growth Fund-Varsu India Growth Story Scheme 1 → ~3.65%

- Aurum Sme Trust → ~1.73%

Financial Information

Figures in Rs. Crores

| Mar 2019 | Mar 2020 | Mar 2021 | Mar 2022 | Mar 2023 | |

|---|---|---|---|---|---|

| Sales + | 91 | 85 | 61 | 87 | 117 |

| Expenses + | 81 | 80 | 63 | 83 | 110 |

| Operating Profit | 10 | 5 | -2 | 5 | 7 |

| OPM % | 11% | 6% | -3% | 5% | 6% |

| Other Income + | -0 | -0 | 0 | -0 | -0 |

| Interest | 2 | 2 | 1 | 1 | 1 |

| Depreciation | 2 | 2 | 3 | 3 | 3 |

| Profit before tax | 6 | 1 | -6 | 1 | 3 |

| Tax % | 29% | 27% | 27% | 36% | 27% |

| Net Profit + | 4 | 1 | -4 | 1 | 2 |

| EPS in Rs | 3.50 | 0.83 | -3.23 | 0.54 | 1.98 |

| Dividend Payout % | 0% | 0% | 0% | 0% | 0% |

Industry and Competition (Ref: Chatha Foods RHP)

Market overview

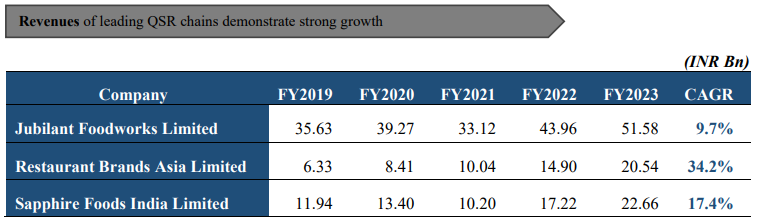

The global QSR market was valued at INR 25.05 Trn in FY 2022. It is expected to reach INR 54.53 Trn by FY 2027, expanding at a CAGR of ~17.41% during the FY 2023 ─ FY 2027 forecast period. The requirement for a wide variety of fast-food items and the growth of the market both contribute to the quick-service restaurants market’s expansion globally. The QSR market in India was valued at INR 171.90 Bn in FY 2022. It is expected to reach INR 431.27 Bn in FY 2027, expanding at a CAGR of ~20.47% during the FY 2022 ─ FY 2027 forecast period. The current decade is overseeing a shift to a larger organized sector. Customer retention and a higher range and depth of offerings are new goals among the organized market players of QSR.

QSR Market in India

• The QSR market in India was valued at INR 171.90 Bn in FY 2022. It is expected to reach INR 431.27 Bn in FY 2027, expanding at a CAGR of ~20.47% during the FY 2022 ─ FY 2027 forecast period.

Major quick food-service chains, such as McDonald’s, Burger King, and Domino’s, among others, are

deepening their reach in India’s smaller cities and benefiting from a younger demography, thereby further aiding the growth of the market.

• The QSR segment will see its next big growth come from consumers in tier II and tier III cities. Annual spends on eating out at QSR chains in non-metros are expected to surge 150% to INR 3,750/- per household over the next three years.

Competition

Our industry comprises of both organized and unorganized players, therefore we face competition from both small players who belongs to unorganized sector and big players who have better resources availability.

Promoters

Promoters are Paramjit Singh Chatha, Gurcharan Singh Gosal, Gurpreet Chatha and Anmoldeep Singh.

Paramjit Singh Chatha aged 55 years, the Chairman and Managing Director of the Company and a member of the Promoter Category, has founded the Company. He was appointed the Managing Director of our Company, w.e.f. April 01, 1998. He has been actively involved in business planning, strategy development and expansion activities since the inception of our Company. He has an experience of 25 years and has been instrumental in expanding the operations of our Company. His leadership has contributed to the growth of our business and the establishment of long term relationships with our customers. As the Managing Director, Paramjit Singh Chatha is responsible for

developing and maintaining the company’s vision, mission statement, and strategic plan. He reviews financial statements and other reports to evaluate the Company’s performance. Furthermore, he identifies new opportunities for revenue growth, such as the introduction of new products, new customers and new businesses. He effectively communicates with employees to ensure they understand the Company’s goals, objectives, and policies.

Additionally, he evaluates new technologies and business practices to assess their potential impact on the Company’s operations and effective marketing strategy to promote the products offered by the Company.

Product Categories

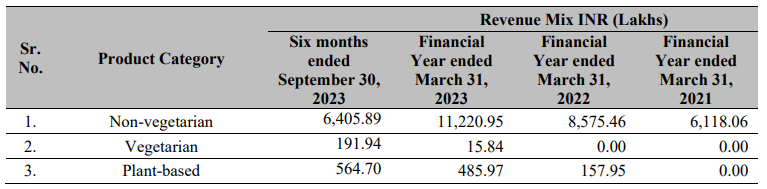

(a) Non-Vegetarian: We manufacture and sell non-vegetarian products such as pizza toppings, sandwich fillings, burger patties, snacks and more to leading QSR’s, CDR’s and other HoReCa segment players.

(b) Vegetarian: We manufacture and sell vegetarian products such as pizza toppings, sandwich fillings, burger patties, taco fillings to leading QSR’s, CDR’s and other HoReCa segment players. We ventured into vegetarian products in the year 2022.

(c) Plant-Based: We manufacture and sell plant-based products such as plant-based sausages, salami, pepperoni; Indian snacks like kebabs, tikkas & samosas; plant-based nuggets & burger patties, grilled burger patties to certain QSRs, CDRs and other HoReCa segment players. Additionally, we supply our products to larger conglomerates and other companies under their own brand names, including Bluetribe (Alkem Group), Shaka Harry (Liberate Foods), Green Bird (Continental Coffee), Plantaway (Graviss Group), and many others. We ventured into plant-based mock meat products in the year 2021.

Revenue Mix

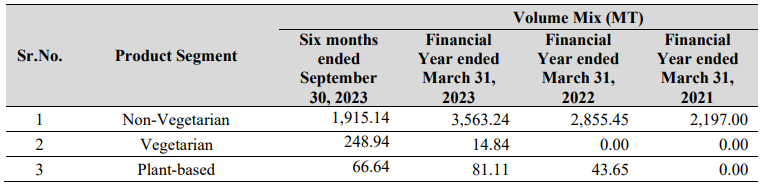

Volume Mix

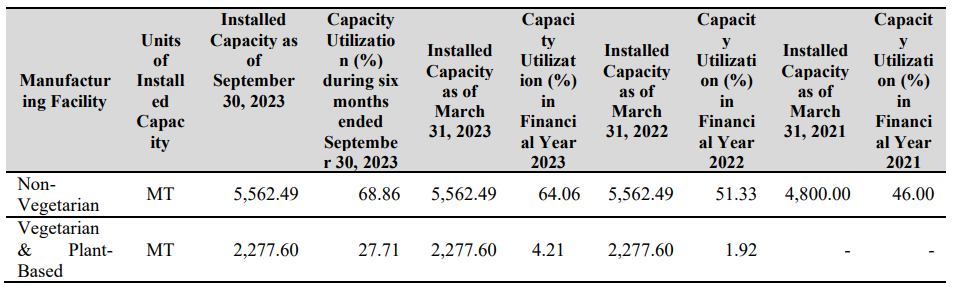

Installed Capacity

Key Customers

Ratios

Figures in Rs. Crores

| Mar 2019 | Mar 2020 | Mar 2021 | Mar 2022 | Mar 2023 | |

|---|---|---|---|---|---|

| Debtor Days | 37 | 26 | 39 | 32 | 30 |

| Inventory Days | 27 | 34 | 33 | 38 | 39 |

| Days Payable | 55 | 59 | 64 | 59 | 48 |

| Cash Conversion Cycle | 9 | 1 | 7 | 11 | 21 |

| Working Capital Days | 3 | -5 | 4 | -1 | 15 |

| ROCE % | 10% | -16% | 7% | 15% |

Disclosure: Have taken a small tracking position in last 10 days.

Thanks,

Dhaval Patel (SMEmitra)