It is surprising that Valuepickr forum has closed the thread for Nuvama and do not allow any posts there. Nuvama’s mkt cap is now three times that of Edelweiss!

Posts in category Value Pickr

Oil India- has its time come? (09-04-2024)

Thanks Hemant & LarryWink for valuable inputs.

I do Respect your views.

Whether a stock is overvalued or undervalued is subjective- views vary – it is the way in which you look at it.

Adani green for example carries a 12 months trailing P/E of 185. Fully debt ridden with 8 debt to equity ratio. No cash balance is possible after servicing the debts for next 1 decade or so. But for every trade , there is a buyer and there is a seller. only time can say who makes money!

Similarly Energy PSU’s like Oil India and ONGC trades at a P/ E of 7 to 8 with a debt equity ratio of 0.5. So , i am comfortable to buy at this price , though it is trading a higher than its historical average P/ E of 3-4. But when I compare with PVt players , I find there is a further scope of re-rating in PSU with down ward risk remaining limited.

Yes, PSU’s past was not so good and I guess history remains as history.This govt is trying to do something to build the economy as we can see from the results…whether it is railway, defence , or energy basket – Govt’s heavy capex plans and under Atma Nirbhar Bharat theme. PSU’s seem to be showing a good turn around and so also Mr market has given s thumbs up … energy transition being planned all over the world in a big way and in India it is the cash rich PSU’s who are leading the charge.

Having said that , i would keenly watch the election results and policy continuance and take a further call on buy sell or add to positions… For now I am comfortable holding my positions, though I have pruned my % position to reduce overall portfolio holdings.

Regarding the views on crude …I agree … it has been the integral part of our daily life …primary source of energy , Pharma, petro chemicals , fertilisers and the uses are endless.

But when the world has decided to do away with it …substitutes are already there. For example Hydrogen from electrolysis of water by solar wind is not only the primary sources of feed stock for power plants , but it is going to be the primary source of energy for transport sector – Automobiles ,trains and aeroplanes.

Starting from hydrogen and with help of carbon , all chemicals can be manufactured- Hydrogen can be an input in processes to produce chemicals such as methanol, ammonia, ethanol hydrogen peroxide, hydrogen chloride, aniline, cyclohexane, TDI and oxo-alcohols.

And TDI (Toluene diisocyanate) is commonly used as a chemical intermediate in the production of polyurethane foams, elastomers, and coatings; paints; varnishes; wire enamels; sealants; adhesives; and binders. It is also used as a cross-linking agent in the manufacture of nylon polymers.

And starting from Ammonia , you can produce a series of fertilisers such as ures, DAP, Ammonium nitrate, Ammonium sulphate , SSP. etc.

I am sure science is working to make it possible to produce everything you need from Hydrogen. And I guess the science was always there …but now these are being rediscovered and pursued rigorously – the only target is to tacke climate change , reduce carbon foot print

And as per latest development , synthetic e diesel / e-fuel can be manufactured out of hydrogen.

Delta Corp – A huge but risky opportunity (09-04-2024)

Good. Ist point is very disappointing for me. My conviction was on Online gaming and Casinos . May be I have to shift my funds to Nazara Tech? will look for related thread.

Sunteck Realty – Quality Real Estate Company (09-04-2024)

Pabrai is exiting India completely as per recent news report

See the bright Sun: Aditya Vision (09-04-2024)

d2cfb97c-d9ec-440a-8261-6755d1f900bb.pdf (313.4 KB)

Raid at their warehouses in UP

The Anti-Portfolio (09-04-2024)

@vikas_sinha – Firstly, congratulations on achieving 33% CAGR over almost 7 years, that quite an achievement. Do you mind sharing why you think Beta Drugs is a mistake? Would like to understand your anti-thesis on it. Per me, it has the following things going for it:

Strong R&D setup in place

Indian Oncology Drug market is on the rise

It is a net debt free company

High ROE and ROCE business and steady operating margins of 18-19%

It’s expecting 290cr+ revenue for FY24

And I also believe you have been tracking Arman Financials for a while now, what according to you is the hold up with it? Is it the recent increase in NPAs or is there more to it? It’s been consolidating for a year now, which I think is good. But when it comes to triggers which will make it regain its upward trajectory again, what do think those are?

Thanks in advance !

Suryoday small finance bank (09-04-2024)

The bank has reported advances of Rs 8,650 crore for the quarter ended March FY24 (including inter bank participatory certificates (IBPC) of Rs 400 crore), growing 14 percent over the previous quarter and 41 percent over the year-ago period. Disbursements at Rs 2,340 crore increased by 31 percent QoQ and 39 percent YoY, while deposits grew by 20 percent QoQ and 50 percent YoY to Rs 7,775 crore for the quarter. The CASA ratio has improved by 1.6 percent QoQ and 3 percent YoY to 20.1 percent in Q4 FY24. The disbursements in FY24 of over Rs 6,900 crore increased by 36 percent compared to FY23 on continued momentum in Vikas Loan as well as retail assets disbursements.

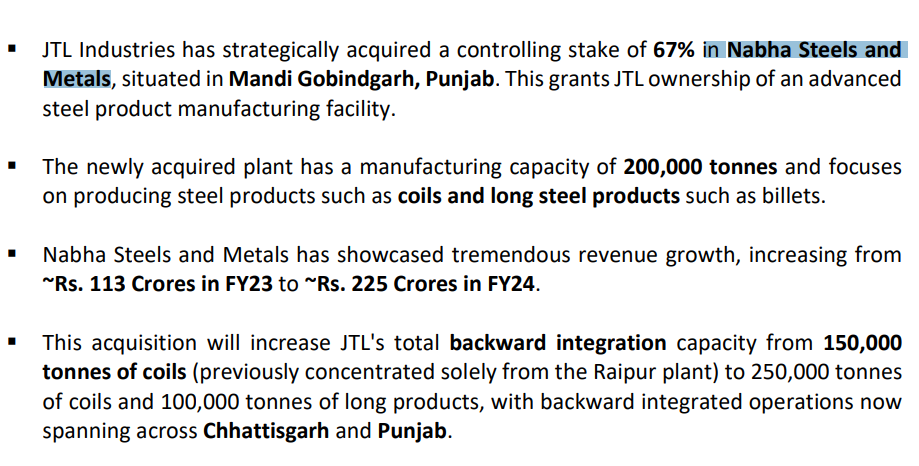

JTL Industries – Fast Grower at an inflexion point (09-04-2024)

JTL has announced acquisition of 67% stake in in Nabha Steels and

Metals for Rs 70 Crore

One thing which looks little bit weird here is that the company is just 3 years old & doing turnover of Rs 225 cr.