Management is not good . In 2020 they cut salaries up to 70 % for a whole year.

Posts in category Value Pickr

Narayana Hrudayalaya Ltd (06-04-2024)

Yes government after 2914 is focusing on infra , road , and made in India . It takes time .

Som Distilleries and Breweries (06-04-2024)

I don’t know if you have mentioned this before in the thread, but what is your return expectancy here? CMP is 25% below the ATH. Are you looking for a multibagger here or do you want to hold for longer term, thinking of compounding?

From your posts alone, it seems there are some issues with the company. The participation from institutions, FII or DII is <1%. No MF holding here, but they hold United Spirits, United Breweries, Radico Khaitan (I have not checked others). Retail has 64% holding here.

If your had bought a lower price, as a value bet, then I guess it is fine, if not, if your purchase price is close to CMP, or if you had bought at a higher price, and are thinking of increasing position, then it can be risky. Price can double from here within 1 year, due to capacity expansion, or for any other business changes, I don’t know.

Senior and experienced investors usually stay away from such businesses, one reason being, there are many opportunities available in the market, they can dedicate their time and efforts to such businesses and increase their chance of being rewarded. As you are young, you have every right and affordability to learn and experience any which way possible. So this can be a case study for you, irrespective of the outcome.

Not invested, know nothing about the business, nothing to add quantitatively, just posting some qualitative observations and some thoughts.

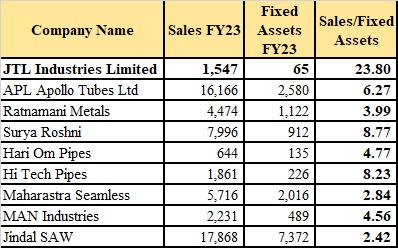

JTL Industries – Fast Grower at an inflexion point (06-04-2024)

I was comparing fixed asset turnover across the structural steel pipe industry and i got a interesting data set

the JTL has the smallest asset base and the highest fixed asset turnover but given there revenue of 1547 crores the closest player Hi tech pipe has an asset base of 226 crores and even hari om pipe with sales of 644 crores has an asset base of 135 crores so how they are able to achieve fixed asset turnover of 24x while other players are able to generate only 4-8x of fixed asset turnover

if anybody has possible reason for it or have visited there plant and knows the answer pls reply as it would be of great help.

Pennar Industries Limited (06-04-2024)

@avthakkar have you taken position in Pennar Industries? I am closely tracking this

Antony Waste – Long Term (06-04-2024)

Started reading about the company quite recently. Most of the revenues and project of the company are form municipalities means government. It is never a good idea to be in business with government as a lot of tender competitions, subsidies, corruption etc. comes to play. But will it play out in this case I’m not sure. I think the industry, company is set for exponential growth but my only problem is the one I mentioned. Can anyone who is tracking the co. and industry tell their insights and perspectives please?

Intense Technologies (06-04-2024)

What do they do??

Intense Technologies provides Customer Communications Management (CCM), Business Process Management (BPM), and Digital Experience Management (DCX)

Top use cases of CCM include driving self-help strategy to promote a company’s mobile application downloads, working with contact center analytics to reduce incoming volumes, driving brand loyalty for an enhanced customer experience, ad-space monetization for cross-selling & brand partner marketing, hyper-personalization for better customer engagement & improve overall customer experience and capturing customer interest & CTR for enhanced lead generation ensuring higher campaign success

Fortune 500s use thier Digital end-to-end CCM solution platform, UniServe NXT which is an award winning platform. It takes care of digital customer onboarding, the customer analytics aspect and the customer billing and metering accuracy.

Then they have the digital communication like your EBBP, your e-bills all of that and the B2B analytics at a high level. We are in the four quadrants of Acquire, Analyze, Engage and Experience; this is the customer life cycle.

Our list of marquee customers includes top five private banks, top five insurance service providers, and the two top telecom service providers (TSPs) of India with over 50% market share in the insurance and telecom sectors in India

What is interesting here?

So they do licensing and then provide AMC as well. Right now 60% to 65% of their business is AMC. AMC business is like a perpetuity business which grows at 15% to 20% every year and the rest of the business is lumpy licensing, where every year they have to find new customers and sell licence

So they should be at least growing by 9% to 12%

This is from one of NEWGEN very old concall

As per Gartner and Forrester peer insight Intense technologies has the best product , better than Adobe, Oracle, Newgen etc check it out on the link below

https://www.gartner.com/reviews/market/customer-communications-management-software

There are various market intillegence report which say the same like spark matrix, aspire leaderboard etc etc

The point is despite newgen having an R&D team of 300+ people and intense entire team size being around 500 they have a better product in the same category + intense has clients from fortune 500 so, at least we know the product is great.

From an old con call of newgen just to understand their CCM %

So What is the problem with intense??

The above cut out is from one of these market intillegence report and you would see many times in the con call as well the promoter says we are weak in sales and marketing. Also I have noticed in various market intillegence quadrants that they are horizontally ahead which shows product capability but vertical they are always behind newgen which shows execution capability.

Why has it been like this and what is different now??

My understanding of a product company is you have a fixed cost, in their case it is 50-55cr (it would be more now this is old data) so as a company you need to have a particular sales to have some flexibility to experiment new things, which they did not have + they had a very bad time because of a BSNL order in past.

Now they being at 2x their cost I think the company is having enough room to take those risk to get new sales.

Are they taking the risk/experimenting then??

One of the reasons for the increase in cost is that they purchase hardware and give it to clients so it is like trading but you can see a 30% growth in employee exp. In a product company you don’t have to grow so much on the employee front.

This is from EPFO, as on august 2023 their strength is 570

My understanding is that this is a 30% margin business, I mean there is no significant expense in 60% of their maintenance business but you can see this year their cost have significantly increased. IT infra up 3x, they are at 20% margin now and these are the cost which would get them sales.

The started PROJECT BUTTERFLY in december 2022 which is like an internal thing

Their sales growth and margins for last 3 qtrs

Recently they have opened a new office

https://twitter.com/in10stech/status/1776262640203084252

Back in 2016 and 2017 they had like 2 sales guys now I am just going to quote them from one of the con call

“”In business development, we have added about 12 resources. In sales, we have added about five new sales. “” Q4FY23

“”In fact, as a matter of fact, even this quarter we added four additional sales personnel with pointed focus around being able to cross-sell, up-sell these new revenue streams that we’ve added. Q2FY24””

The CFO is also a new addition just added about a year back

https://www.linkedin.com/in/nitin-sarda-06260538/?originalSubdomain=in

The point is that there have been multiple actions which have been taken in the last one year or so and we can also see the results, now how long can they achieve this is a key thing to observe.

Other developments/ initiatives/Points

- They are now focusing more on Saas and recently their flagship products has been hosted in AWS in the global marketplace. This would reduce the lumpiness from the licence business which is like a one time revenue but I think they would have to forgo AMC as you won’t charge that on saas. Q3FY24

- They have tied up with Natsoft to be their strategic partner,to take their products and solutions to the market. But from a strategic perspective not a financial investment

- Current cash position and receivable as on dec 2023

So we can safely say that cash + receivable is about 100cr and they are available at 300cr mcap. They would definitely do something with this cash, if they acquire some company which would definitely be in their cards that would be a major trigger

- 20% is from international business and they are trying to get into the US markets now

- “”If you really look at it, from employees, directors and promoters put together, we are around 35.4% as a holding”” quoted from concall.

I am trying to meet the management, if not I would ask questions in the con call, I am attaching the list of questions I have in my mind, would love if anybody can answer them.

So to summarise, 60-65% is an annuity business which is growing at 15%, so worst case a 10% growth business available at 17 times PE and promising for 30% growth. Currently doing about 20% margins being a 30% margin business and also having about 50cr+ cash assuming if they collect receivable then about 100cr and they have a solid product

Technicials

RISK

If you read the above thread then this stock was a pump and dump stock, If not the entire thread I would encourage everybody to read this post

Shrihari has made 8 PARTS so please read all of them, Promoter integrity is questionable in this company

DIsc – invested, small position less than a 1%, will increase once I get more clarity

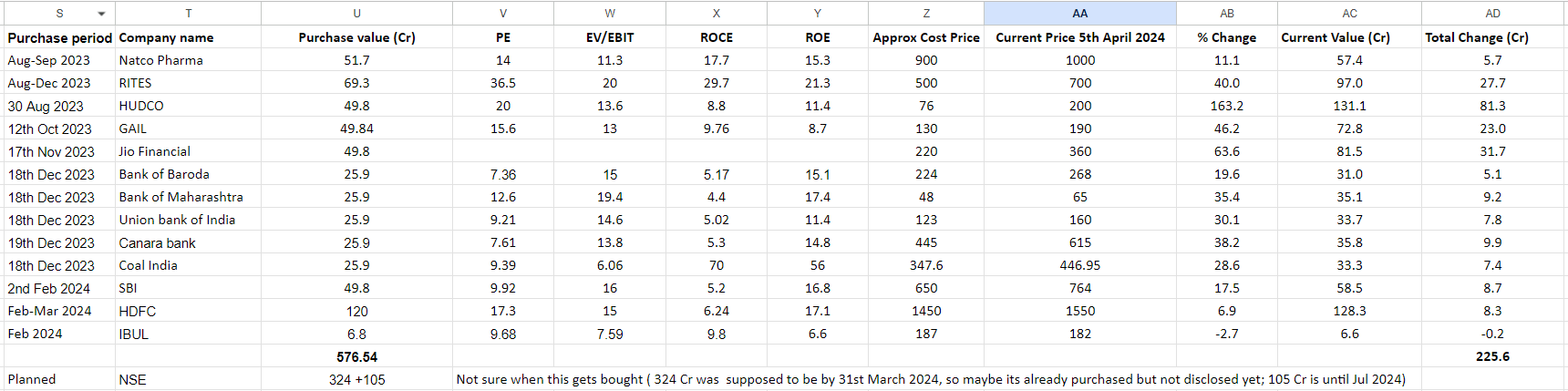

Maithan Alloys Ltd (06-04-2024)

These guys are really killing it with their equity investments. They have invested abour 564 Cr over the last 8 months or so (Excluding the investment into NSE) and they have had about 50% absolute returns so far, excluding dividends.

I think the last quarterly report only showed the income statement. I wonder if the equity investments is really getting priced in. Does anyone know if the book value on screener etc would be adjusting for the equity investment gains? If not, I expect a nice pop when the balance sheet does get disclosed.

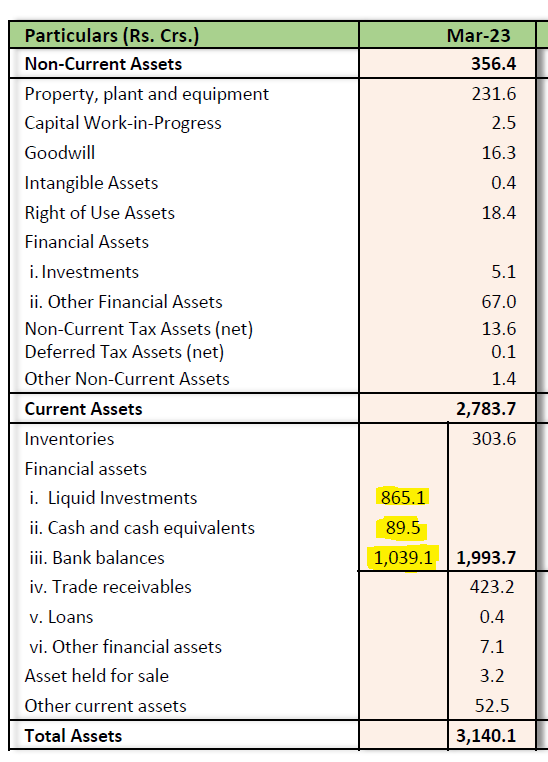

This is the last balance sheet from 31st March:

Add about 250 Cr of earnings over th last 4 quarters to the current assets of 1993 Cr, 225 Cr of equity gains, at least 30-40 Cr in interest on bank deposits, and you get to 2500 Cr of just cash + equity.