There has been a whole lot of doubt around the company because of change in management. That’s why the stock has been consolidating for a long time. But this quarter has turned out to be excellent. Hope it continues the moment.

Posts in category Value Pickr

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (06-04-2024)

Notes from Gensol Credit Rating Revision by CareEdge Ratings

Summary

Rating revised from BB to BB+.

Positives (leading to upgrade):

- Strong execution in solar EPC projects.

- Significant growth in TOI.

- Improved profitability.

- Growing orderbook with strong revenue visibility (FY25-FY26).

- Successful EV leasing business with timely payments from Blu-Smart (FY24).

- Experienced promoters.

- Healthy and geographically diversified solar EPC orderbook from reputable clients.

- Structured lease rental agreement with Blu-Smart.

- Adequate liquidity.

Negatives (constraining the upgrade):

- Profitability susceptible to solar module price volatility.

- Deteriorated capital structure due to increased debt for EV leasing.

- Execution and funding risk associated with the ongoing EV manufacturing plant.

Details

Business:

-

Strong revenue growth driven by EPC and EV leasing.

Revenue FY’23 FY’24 Total Op Inc Rs cr 393 960 YoY growth 145% 144% -

Revenue shifting towards EV leasing

Revenue share FY23 9MFY24 EPC 84% 80% EV leasing 9% 16%

Strengths:

-

Orderbook:

- Rs. 1176 crore solar EPC orderbook (3.57x FY23 TOI).

- EPC fixed price contracts to be executed in 6-10 months.

- Lowest bidder for contract of Rs.520 crore in March 2024.

- Low counterparty credit risk (government & reputable clients in 7 states).

-

Experienced promoters and management

-

Improved Profitability:

- 14.89% PBILDT* margin in FY23.

- 291 bps YoY increase.

- Expected operating margins around 20% in FY24 (higher Blu-Smart lease income).

-

Structured Lease Agreement:

- No cash outflow for EV leasing (Blu-Smart covers repayments). [Facilitation fee?]

Weaknesses:

-

High Leverage:

- Overall gearing of 2.10x (FY23, deteriorated from FY22).

- Increased debt due to debt-funded EV acquisition for leasing.

- Expected further deterioration due to continued debt-funded acquisitions for leasing.

-

Delayed EV Production:

- EV mfg plant in Pune to produce Electric Cars and Electric Urban Cargo vehicles.

- Capacity: 40 units per day per shift.

- Expected project cost ~Rs 230 cr

- Expected starts of Q2FY24 delayed by year due to ARAI approval.

- ARAI approval received in Feb24. Expected start H2FY25.

Liquidity:

- Adequate liquidity with lease payments from Blu-Smart and healthy cash flow.

- Plans to raise Rs 500 crore through share warrants in FY25. [Dilution risk?]

*Profit Before Interest, Lease rentals, Depreciation and Taxation

52 week highs and all time highs strategy (06-04-2024)

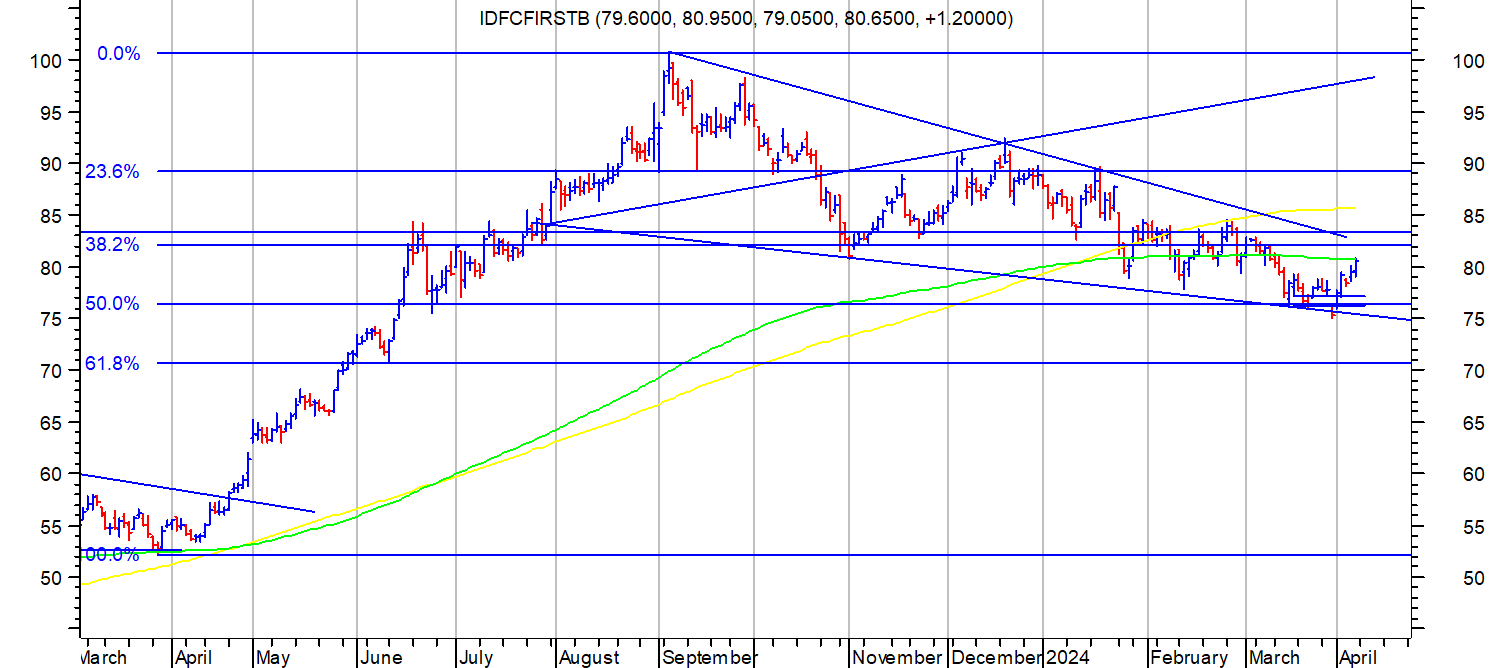

IDFC First Bank cmp 80.

Stock price rallied from levels of 53 in March 2023 to 100 in September 2023 and since then went into a triangular consolidation which has lasted for more than 6 months now. Important thing to observe that all during this correction, stock price has not gone below 50% retracement level of its previous rally, which shows some strength and resilience in a routine correction.

An interesting observation is a gap which was posted on 28-03-2024 when a big institution offloaded a big chunk of its holding in IDFC first bank. When there is a gap at the fag end of a correction, and is immediately filled in next day or few days, ( here it got filled very next day) it is an example of an exhaustion gap. This often signifies exhaustion on the part of sellers and can be a fertile ground for a change in trend.

The triangular consolidation drawn on the daily chart would end once the stock price closes above the breakout level from triangle which happens to be 83-84 currently. The prior upmove from 53 to 100 resembles a flag pole like structure and the triangular consolidation resembles a flag/pennant. Target for breakout based on this kind of structure comes to around 115-120.

For anyone wanting to do fundamental research, IDFC First is a well researched stock and company does regular presentations and concalls.

disc: invested.

52 week highs and all time highs strategy (06-04-2024)

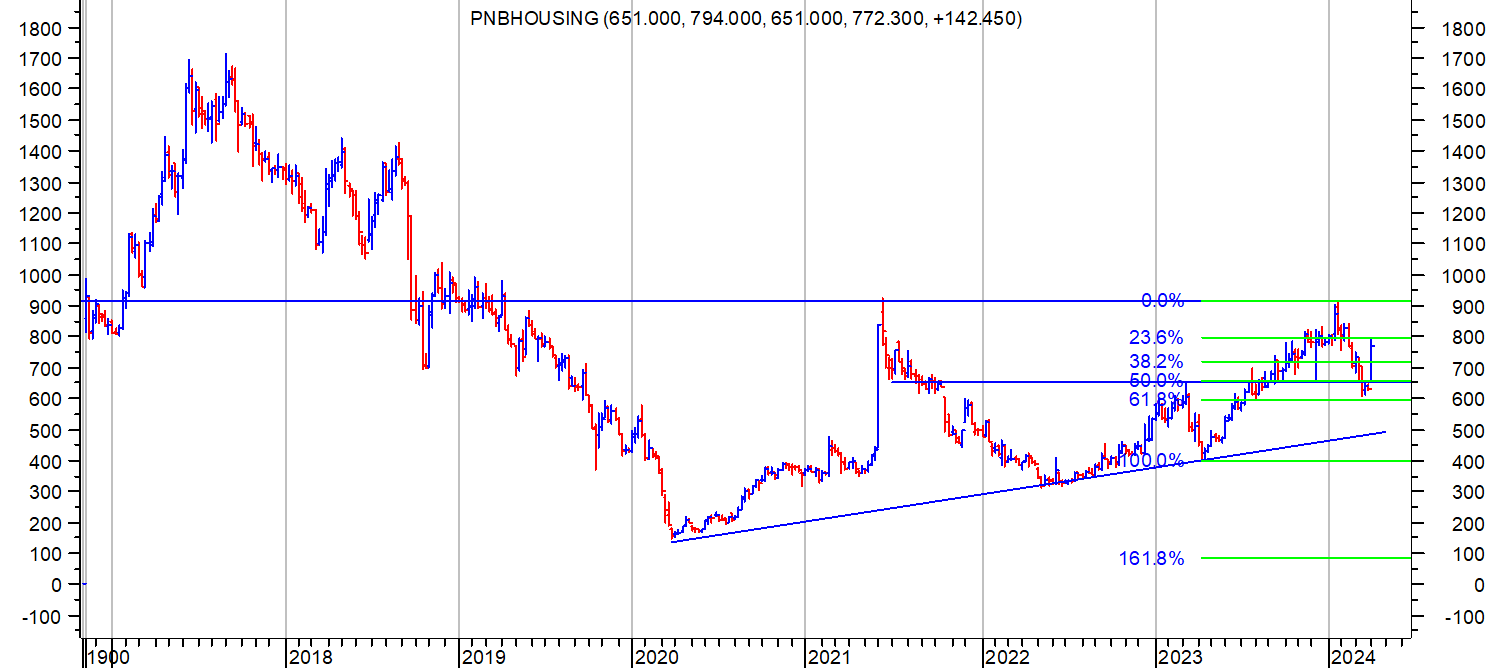

PNB HF. Cmp 770. Stock price corrected from resistance at 720 and in line with overall market went down to retest key support zones. It went below 30 WEMA briefly and retraced 61.8 % of its previous upmove (marked on charts) and then last week gave a big bullish close. An ascending triangle is marked on the weekly charts.

Overall structure is that resembling a rounding structure with top near 1700 levels. Fundamentally company has now regained its growth focus under new CEO Girish Khousgi and asset quality has shown sequential improvement. For those who want to do detailed research, company provides presentations and does regular concalls.

disc: invested recently.

52 week highs and all time highs strategy (06-04-2024)

PNB HF. Cmp 770. Stock price corrected from resistance at 720 and in line with overall market went down to retest key support zones. It went below 30 WEMA briefly and retraced 61.8 % of its previous upmove (marked on charts) and then last week gave a big bullish close. An ascending triangle is marked on the weekly charts.

Overall structure is that resembling a rounding structure with top near 1700 levels. Fundamentally company has now regained its growth focus under new CEO Girish Khousgi and asset quality has shown sequential improvement. For those who want to do detailed research, company provides presentations and does regular concalls.

disc: invested recently.

Sterling & Wilson Solar Ltd. – Will the Sun Keep Shining? (06-04-2024)

Their khavda project is facing major cost pressures…next few quarters to be muted

Sterling & Wilson Solar Ltd. – Will the Sun Keep Shining? (06-04-2024)

Their khavda project is facing major cost pressures…next few quarters to be muted

IDFC First Bank Limited (06-04-2024)

1 crore penalty for loan non compliance imposed by RBI.

IDFC First Bank Limited (06-04-2024)

1 crore penalty for loan non compliance imposed by RBI.

Deepak Fertilizers and Petrochemicals (06-04-2024)

i think TAN business is what looks more lucrative to me as mining as a theme will rise in india their tan facility and Consultancy services which they are providing, as discussed in latest concall will be of key competitive edge.

post demerger things will be interesting & i am looking forword to it.