Will China pull ahead with battery technology? | Transforming Business

Posts in category Value Pickr

Adani Ports – Leader in ports (31-03-2024)

9 Months update:

Total Income: Rs 21010.04 Cr

EBITDA: 12917.75

PAT: Rs 5887.11

EPS: 28.10

Estimated EPS, based on Q4 as compared to good quarter : Rs 11.5/- per shares

Estimated EPS (E) : Rs 39.60/-

Chaitanya’s Portfolio (31-03-2024)

The stock price of kotak mahindra has been in a consolidating phase for the past five years. I would like to know, if the company is a consistent performer why has it not reflected in the stock price.

Akash Portfolio (31-03-2024)

can you pls elaborate what is family portfolio and your own portfolio…do you maintain two seperate to save tax? Is family pirtfolio a joint portfolio or its on name of family…like a trust etc?

Selecting a broker (31-03-2024)

Does anyone have account with HDFC Sky? How is the interface and glitches if any?

Linde India Ltd. – A Case Study by a Newbie! (31-03-2024)

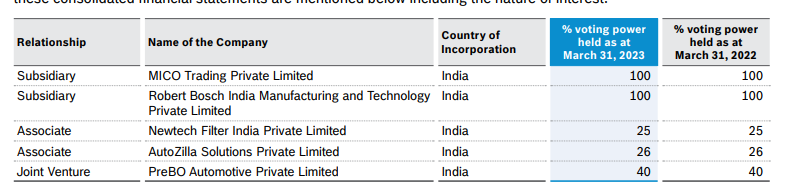

This is what i could find under listed firm…Bosch Limited – and TRobert Bosch

India Manufacturing and Technology Private Limited,

In Unlisted it is as below. Now some of this maybe JV or Associate firms but need to check.

Sterling & Wilson Solar Ltd. – Will the Sun Keep Shining? (31-03-2024)

Anyone have further information on the much anticipated ‘turnaround’ ?

Basis scuttlebutt – legitimate & well respected PMS players have been adding for their clients across the past 2-3 weeks and positions have been made.

Would appreciate any information from those closely tracking.

Invested & sized at 50% for now.

Route Mobile – Internet, Mobile & Telecom (31-03-2024)

MAKE A CASH OFFER TO ACQUIRE UP TO 1,64,05,338 (ONE CRORE SIXTY-FOUR LAKH FIVE THOUSAND THREE HUNDRED AND THIRTY-EIGHT) FULLY PAID-UP EQUITY SHARES OF FACE VALUE OF ₹10 (INDIAN RUPEES TEN) EACH (“OFFER SHARES”), REPRESENTING 26% (TWENTY-SIX PER CENT.) OF THE EXPANDED VOTING SHARE CAPITAL (AS DEFINED BELOW) IN ACCORDANCE WITH THE SECURITIES AND EXCHANGE BOARD OF INDIA (SUBSTANTIAL ACQUISITION OF SHARES AND TAKEOVERS) REGULATIONS, 2011 AND SUBSEQUENT AMENDMENTS THERETO (“SEBI (SAST) REGULATIONS”) FROM THE PUBLIC SHAREHOLDERS (AS DEFINED BELOW), AT A PRICE OF ₹1,626.40 (INDIAN RUPEES ONE THOUSAND SIX HUNDRED AND TWENTY-SIX POINT FOUR ZERO) PER EQUITY SHARE (“OFFER PRICE”) ALONG WITH THE APPLICABLE INTEREST (AS DEFINED BELOW) OF RS. 18.27 (INDIAN RUPEES EIGHTEEN POINT TWO SEVEN) PER EQUITY SHARE, THEREBY AGGREGATING TO ₹1,644.67/- (INDIAN RUPEES ONE THOUSAND SIX HUNDRED AND FORTY-FOUR POINT SIX SEVEN) PER EQUITY SHARE, PAYABLE IN CASH, IN ACCORDANCE WITH THE PROVISIONS OF REGULATION 18(11) AND 18(11A) OF THE SEBI (SAST) REGULATIONS

Any idea when does the tender period start?

Don’t see anything under Corporate Actions tab in Zerodha

Varun beverages fast growth duopoly business (31-03-2024)

I would like to draw your attention towards the Pepsi’s largest manufacturer and distributor in India – VBL!

Few things to keep in mind:

- With 25+ years of operations, Varun Beverages or VBL is Pepsi’s top 3 franchisees in the world outside US.

- The company operates in three broad segments:

- -Carbonated Soft Drinks which contributes to 71% of the portfolio volume. Products include: soft drinks (e.g., Pepsi 7Up) energy drinks (e.g., Sting), club soda and carbonated juice drinks

- -Non Carbonated beverages which contributes to nearly 25% of the portfolio volume. Products include: fruit-pulp drinks (eg., Tropicana), ice tea (under Lipton brand), sports drinks (e.g., Gatorade), packaged drinking water (e.g., Aquafina) and in-house dairy based drink (under the Creambell brand).

- Food Products. Products include: Kurkure Puffs in India and Lays and Doritos in Africa.

- With BevCo’s acquisition, the firm will get access to four new product lines. Products include: Caffeine drink – Refreshhh, Energy Drink – Reboost, Carbonated Drink – Coo-ee and Alternative Drinks -JiVE

- It has 42 manufacturing facilities (36 in India & 6 in International territories). Also, the firm completed a capacity–driven capex of 2100 cr. in 2023 and has planned for 3600 cr. in 2024 of which 600 cr. is earmarked for international markets. As per the management, with new plants, the revenue potential will double in the coming years.

- In terms of geography, Indian business contributes to 80% of overall sales. Within India, it operates in 27 states and 7 UT. Remaining sales are international, from Nepal, Sri Lanka, Morocco, Zambia and Zimbabwe.

- Varun Beverages is part of the $15B + Jaipuria Group. The group runs the listed firm Devyani International (KFC India, Pizza Hut) and Pearl Drinks, manufacturer of PET bottles. Almost a vertically integrated ecosystem for Pepsi.

- The firm has had a long history with Pepsi. It has grown from 26% contribution to sales in 2011 to 90% contribution in Pepsi sales in 2023. It has the ‘right to manufacturer Pepsi in India’ till 2039 so unlikely to have another firm break this space.

- With over 39 manufacturing facilities, 120 depots, owned fleet of 2500 vehicles, over 2400 primary distributors, 35 lakh outlets and 10 lakh Visi-coolers, VBL’s on ground infrastructure remains a key driver for company’s growth.

- Varun Beverages Limited (VBL) reported a 20% growth in revenue with an 18% volume growth YoY in Q4 CY23. Despite the increase in cost of sugar, the company still ended with improved EBITDA margin. This improvement was due to softening bottling costs and operational efficiencies

- Net debt increased to Rs 4,700 Cr in 2023 from Rs 3,400 Cr in 2022, an increase of 38% due to growth Capex. But, given this is for capacity expansion, the debt is good as long as it can remain controlled. The interest coverage is 11.4x which means firm can pay back interests for this year

- And finally, with my valuation models (both DCF and relative) the stock is highly overvalued so it is not a value play at the moment. However, equity research analysts are claiming a median rise of 1490 (Sharekhan, Motilal, DAM, Nuvama, K.R. Choksey, Indsec and others) with as high as 1732 driven by market growth parameters.

Please check out the link where I further detail this out. Your feedback will help me course correct and increase the depth of my analysis:

Worth ₹1 Trillion without a product! | Varun Beverages Limited

Smallcap momentum portfolio (31-03-2024)

I guess you are meaning the Nifty 200 Momentum index. I do not use this as a reference as it is a different universe.

Over the last 3 to 4 months, I have been comparing pf returns against the index itself on which it is based. Returns have been equal or better.