Posts in category Value Pickr

1 Trillion rupees worth without a single product! – VB Limited (30-03-2024)

A thread exists, post here.

1 Trillion rupees worth without a single product! – VB Limited (30-03-2024)

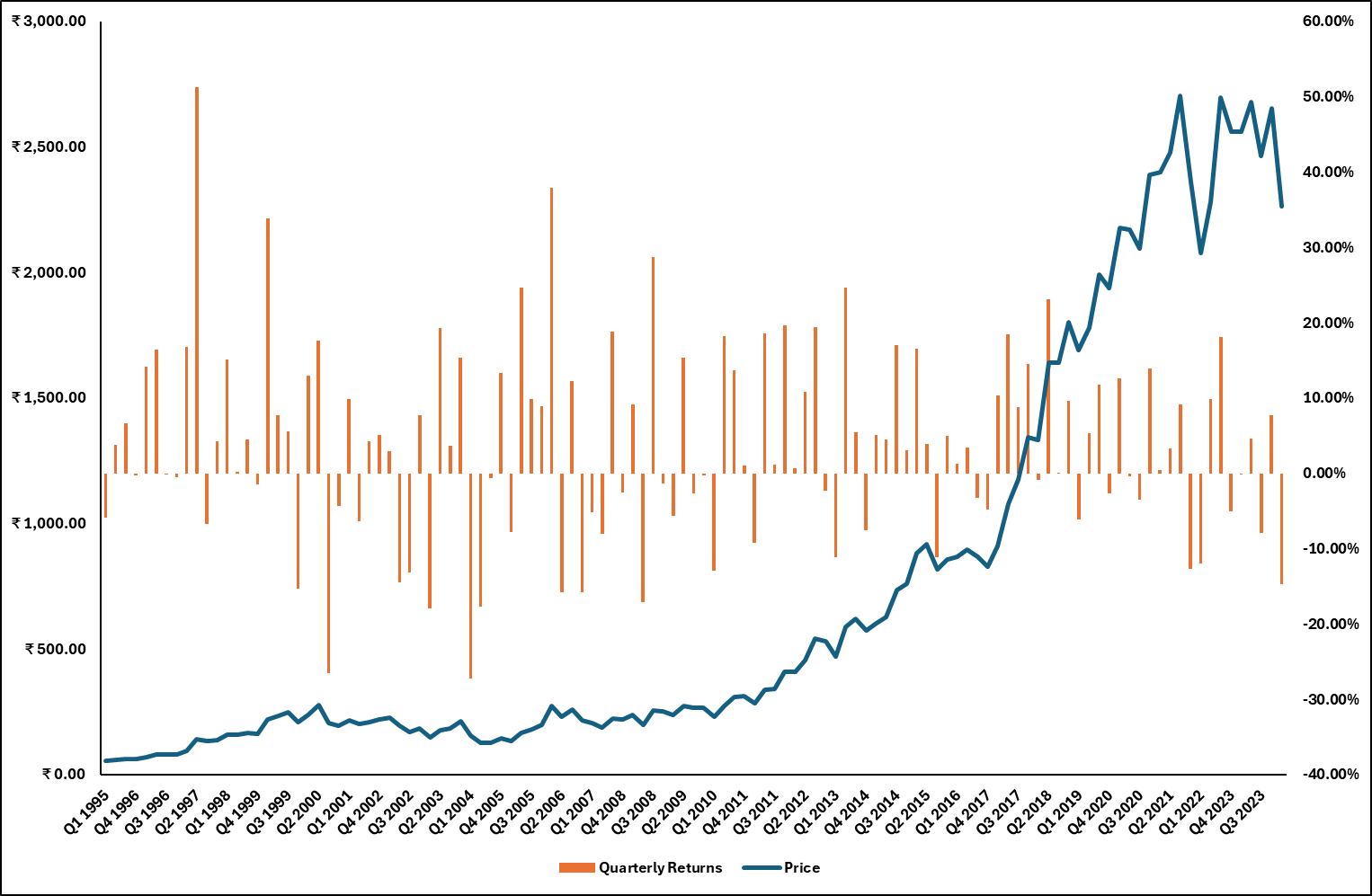

Let us talk about the Pepsi’s largest manufacturer and distributor in India – VBL!

Few things to keep in mind:

-

With 25+ years of operations, Varun Beverages or VBL is Pepsi’s top 3 franchisees in the world outside US.

-

The company operates in three broad segments:

-

Carbonated Soft Drinks which contributes to 71% of the portfolio volume. Products include: soft drinks (e.g., Pepsi 7Up) energy drinks (e.g., Sting), club soda and carbonated juice drinks

-

Non Carbonated beverages which contributes to nearly 25% of the portfolio volume. Products include: fruit-pulp drinks (eg., Tropicana), ice tea (under Lipton brand), sports drinks (e.g., Gatorade), packaged drinking water (e.g., Aquafina) and in-house dairy based drink (under the Creambell brand).

-

Food Products. Products include: Kurkure Puffs in India and Lays and Doritos in Africa.

-

With BevCo’s acquisition, the firm will get access to four new product lines. Products include: Caffeine drink – Refreshhh, Energy Drink – Reboost, Carbonated Drink – Coo-ee and Alternative Drinks -JiVE

-

It has 42 manufacturing facilities (36 in India & 6 in International territories). Also, the firm completed a capacity–driven capex of 2100 cr. in 2023 and has planned for 3600 cr. in 2024 of which 600 cr. is earmarked for international markets. As per the management, with new plants, the revenue potential will double in the coming years.

-

In terms of geography, Indian business contributes to 80% of overall sales. Within India, it operates in 27 states and 7 UT. Remaining sales are international, from Nepal, Sri Lanka, Morocco, Zambia and Zimbabwe.

-

Varun Beverages is part of the $15B + Jaipuria Group. The group runs the listed firm Devyani International (KFC India, Pizza Hut) and Pearl Drinks, manufacturer of PET bottles. Almost a vertically integrated ecosystem for Pepsi.

-

The firm has had a long history with Pepsi. It has grown from 26% contribution to sales in 2011 to 90% contribution in Pepsi sales in 2023. It has the ‘right to manufacturer Pepsi in India’ till 2039 so unlikely to have another firm break this space.

-

With over 39 manufacturing facilities, 120 depots, owned fleet of 2500 vehicles, over 2400 primary distributors, 35 lakh outlets and 10 lakh Visi-coolers, VBL’s on ground infrastructure remains a key driver for company’s growth.

-

Varun Beverages Limited (VBL) reported a 20% growth in revenue with an 18% volume growth YoY in Q4 CY23. Despite the increase in cost of sugar, the company still ended with improved EBITDA margin. This improvement was due to softening bottling costs and operational efficiencies

-

Net debt increased to Rs 4,700 Cr in 2023 from Rs 3,400 Cr in 2022, an increase of 38% due to growth Capex. But, given this is for capacity expansion, the debt is good as long as it can remain controlled. The interest coverage is 11.4x which means firm can pay back interests for this year

-

And finally, with my valuation models (both DCF and relative) the stock is highly overvalued so it is not a value play at the moment. However, equity research analysts are claiming a median rise of 1490 (Sharekhan, Motilal, DAM, Nuvama, K.R. Choksey, Indsec and others) with as high as 1732 driven by market growth parameters.

Please check out the link where I further detail this out. Your feedback will help me course correct and increase the depth of my analysis:

Worth ₹1 Trillion without a product! | Varun Beverages Limited

Rajesh’s portfolio (30-03-2024)

Will assess post H2 results all, management is aspirational and track record is great too… Let’s see

Rajesh’s portfolio (30-03-2024)

Many thanks for the reply! Thoughts on DocMode at the CMP?

Great articles to read on the web (30-03-2024)

AF_AR_Annual-Report_2023.pdf (4.3 MB)

Aquamarine Annual Report.

Brookfield India Real Estate Trust (BIRET) – Institutionally managed REIT (30-03-2024)

I don’t think they have the luxury to go on an expansion spree in the near to medium term without pushing up leverage, which will lower Credit worthiness and Distributions further.

Hindustan Unilever (HUL) (30-03-2024)

That’s because much of the future growth was already priced in and due to lack of fresh triggers the stock price maintained its sideways trajectory. I’ve seen some experts opining that FMCG companies getting 50-60 PEs were relics of the last decade and might not continue…remains to be seen.

Linde India Ltd. – A Case Study by a Newbie! (30-03-2024)

Thanks. All new age GH2 and Semicon and other speciality gases are being routed through unlisted firms.

Same cases with most MNC including Bosch, Schneider, Siemens, ABB etc. No one routes the new speciality or higher margin businesses through the listed firm.