Correction overall PF gains are 155% March 23-24.

Posts in category Value Pickr

Long term investment strategy (Buy, hold but don’t forget) (29-03-2024)

Correction overall PF gains are 155% March 23-24.

Long term investment strategy (Buy, hold but don’t forget) (29-03-2024)

Hi @Amit_Paul

Added wockhardt as new entry, development on two molecules is very interesting. Trimmed Some force motors as it has gone 6 X in an year. No other changes, booked some loss making positions to cut short term gains, below is current PF rightnow

Kalyan Jeweller ( 30%) 300% gains

Force motors ( 12%) 500% gains

Aditya Birla Fashion ( 12%) – 40% gains

Aditya Birla Capital ( 9%) 10% gains

Tata power ( 6%) 25% gains

AGI Green ( 6%) 225% gains

Arvind Fashion ( 6%) 50% gains

Sanghvi Mover ( 7%) 60% gains

Narayana Hrudayala (4%, accumulation mode)

LT Food (3%) 20% gains

Thomas Cook (2.5) 20% gains

Wockhardt (2) new entry

Brand Concepts (2.5) 100% gains

Overall PF gains 250% March 23-24.

Trading positions

- Swelect Energy

- Jubilant Pharmova

- PVRINOX

- Rushil Decor

5 Jash Engineering

6 LIC Housing

7 Suzlon

Long term investment strategy (Buy, hold but don’t forget) (29-03-2024)

Hi @Amit_Paul

Added wockhardt as new entry, development on two molecules is very interesting. Trimmed Some force motors as it has gone 6 X in an year. No other changes, booked some loss making positions to cut short term gains, below is current PF rightnow

Kalyan Jeweller ( 30%) 300% gains

Force motors ( 12%) 500% gains

Aditya Birla Fashion ( 12%) – 40% gains

Aditya Birla Capital ( 9%) 10% gains

Tata power ( 6%) 25% gains

AGI Green ( 6%) 225% gains

Arvind Fashion ( 6%) 50% gains

Sanghvi Mover ( 7%) 60% gains

Narayana Hrudayala (4%, accumulation mode)

LT Food (3%) 20% gains

Thomas Cook (2.5) 20% gains

Wockhardt (2) new entry

Brand Concepts (2.5) 100% gains

Overall PF gains 250% March 23-24.

Trading positions

- Swelect Energy

- Jubilant Pharmova

- PVRINOX

- Rushil Decor

5 Jash Engineering

6 LIC Housing

7 Suzlon

IDFC First Bank Limited (29-03-2024)

This observation on PE players is unfortunately a by-product of buying what I felt were fairly cheap companies and then to notice a big investor exiting . I had the same doubts. But this has happened a few times now that I feel confident in sticking to and continuously re-evaluating my original hypothesis. Sorry but there is no specific study on PE players.

IDFC First Bank Limited (29-03-2024)

you are awesome…Do you follow such PE investors specifically and regularly? Do you have some resources to do it or this is just one-off?

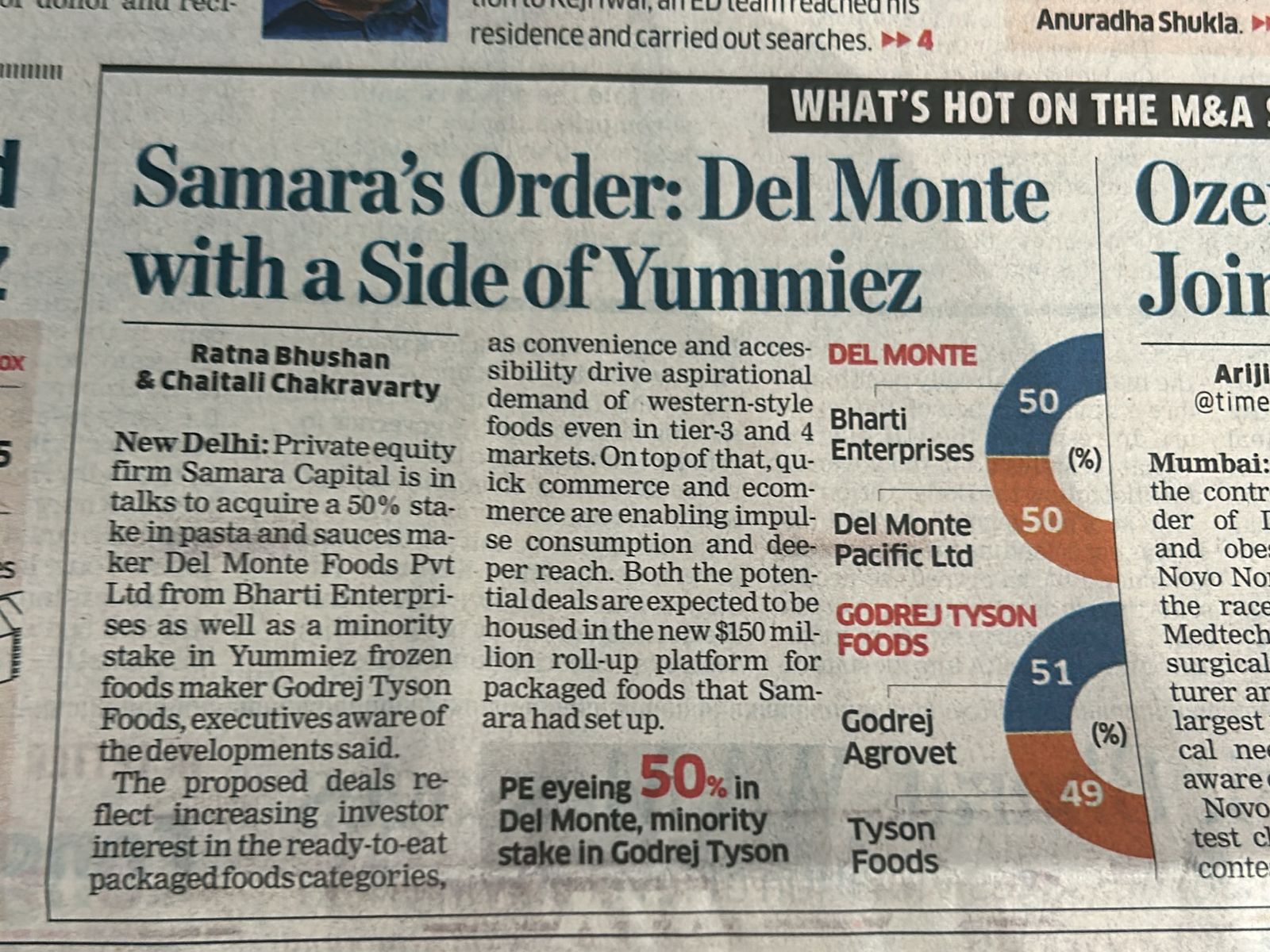

Ceinsys Tech-Engineering, Geospatial & IT solutions Company (29-03-2024)

Wow, this company’s order’s are on a roll. Two more today.

SMC Infrastructures Private Limited

( Announcement under Regulation 30 (LODR)-Award_of_Order_Receipt_of_Order)

Central India Engineering Private Limited

( Announcement under Regulation 30 (LODR)-Award_of_Order_Receipt_of_Order)

Both the orders are for 6.7 Crores INR, for a time period of 12 months.

IDFC First Bank Limited (29-03-2024)

To clear your doubts . I will give an example of the same investor’s( Warburg Pincus ) investment in Laurus Labs . They bought a 32 % stake in 2014 at a 1700 cr valuation. They sold some stake when Laurus went public in 2016 at 5000 cr valuation (Stock price of around 100 )They sold the remaining stake ( around 20%) in May and June of 2020 at 5000 cr valuation( Again stock price around 100) . By the end of September 2020 Laurus was trading at 250 per share. By July 2021 Laurus was trading at 650 per share . They made 3 times their money in 6 years , but missed 6.5 times rise in the next one year . Once their selling was done , there was no stopping the rise. Remember they were on the board of Laurus too.

Fun Fact : Warburg Pincus invested in QIP of Idfc first bank in May June of 2020 at around 20 Rs per share . We cannot say for certain , but some money from Laurus sale might have been used for Idfc first QIP. Even after waiting for 4 years , they could not get the 6.5 times return in Idfc first that Laurus got in next one year .

Conclusion:

- Even the biggest investor , with the access to CEO and the board information can make horrible calls.

- If you are right in the fundamental analysis of the company , the exit of the biggies is often the best time to load up .

It’s not a recommendation to buy Idfc first , but according to me it is definitely a good time to look at it more closely .

Agro Tech Foods – A small cap MNC foods FMCG (29-03-2024)

Sharing a few articles post the change of management

This looks like an interesting special situation where the Current valuations don’t seem to factor in much optimism of mgt change and the possibilities which could arise in an under-utilised franchise

Disclaimer

- Not an investment advice

- Educational post only

- Not sebi regd

- Plz consult ur financial advisor before investing

Cineline India – Picture abhi baaki hai (29-03-2024)

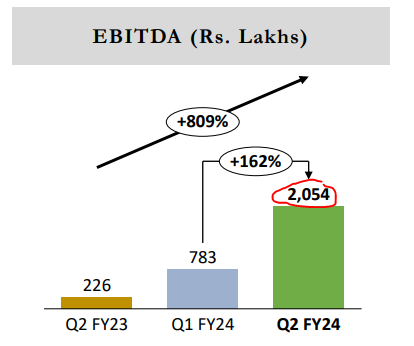

Cineline did 20 cr ebitda in q2-24 from cinema business with 64 screen operating, extrapolating it as an avg for 4qrts makes it rs 80cr ebitda(its naïve and too much of an optimism to assume this considering seasonality, hit releases etc, but just for sake of some estimation)

if they sold hotel for rs500cr(as they claim its the valuation) and added 230 screens (its from the company published info about cost of installing a screen) they should generate around rs300cr additional ebitda.

Currently hotel does an ebitda of rs 10 cr per year, so growing screen count looks like better capital allocation.

Its still however a riskier investment considering the past history, but it can playout well if they execute as per the published plan and maintain operating metrics.