Thanks for this explanation,

But can those timelines be so strict that they push a PE player to sell at a worst possible time and price…UNLESS they know something which we don’t.

Posts in category Value Pickr

IDFC First Bank Limited (29-03-2024)

E2E Networks Ltd – Listed small Cloud computing player (29-03-2024)

An overview of India’s biggest AI bet by Bastion Research

https://x.com/bastionresearch/status/1770447310201266480?s=20

Best Agrolife – Think Big, Think Best! (29-03-2024)

17c87d70-87dc-4a6b-9948-119b3d0b879c (1) (1).pdf (1.2 MB)

Acquiring a non performing target company with same set of promoters , in cash deal( related party transactions)

It is a cause of concern, Can promoters be trusted?

Srivari Spices and Foods Limited (29-03-2024)

Traveling to Hyderabad to attend a family event and see that Srivari has put up ads in Secunderabad railway station. Good to see small cap company spending on advertising and Meena was a popular South Indian actress in 90s.

Responsive Industries: Luxury Flooring Brand? (29-03-2024)

Interestingly, the company’s promoter and FII shareholding has increased significantly over the past two years, and the retail holding is very low. But I believe I unknowingly bought the LVPs for my house, and it’s been great, the product is solid and unlike Wooden Flooring, doesn’t get bloated on contact with water. It feels just like the wood as well.

Hariom Pipes Ltd: A Capex Play! (29-03-2024)

Yesterday only there was conference here is the summary of it

- Difference between hariom and other players is that Hariom has it’s own raw material and that’s why the margins are higher and they don’t use coal

- it’s eco-friendly

- Some of the products can’t be made by their competitors and they have a monopoly in certain value added products

- Saved nearly 26 crores in power cost in the last

9 months due to 2 MW renewable power capacity

- They will help with dealer financing in order to bring receivables down significantly

- Will start dividend policy from next year

- Guidance for this year is intact

- Right now, 50% capacity utilisation – there was a small delay in the latest plant – can go to 80% next year

- Not competing with JTL and Apollo because they are into customised products, so it’s a different customer and different application – mostly into infra, fan, auto – Working with Asia’s biggest fan manufacturer

- Q4 will be the highest topline ever – crossed

1100 crores by February already

- Scaffolding EBITDA per tonne is 12,000 but the volume is low as this is a customised product. Rs, 8,000 Rs for galvanised pipes and 7,400 for MS pipes – average is lower due to coils and the average holding period is 15 days

Hariom Pipes Ltd: A Capex Play! (29-03-2024)

I had mailed to the company and they replied me as follows.

Dear Sir,

First of all congratulations to the team of Hariom Pipe Industries Limited on a great set of numbers in Q3 of FY 2024. Company is on the way to achieve its goal of ₹ 2,500 crore revenue guidance by FY 2026 without compromising on probability. Company did a great job in every parameter. However, I wanted to know the following things because I want to understand the company in a deeper way as I’m an investor in this company.

- Company do exceptionally well, then why company not hold earnings conference calls?

- Why is the company is not cooperating with rating agency i.e., CARE RATINGS?

- Is there any planning to raise equity funds in the foreseeable future?

It is requested to reply to the abovementioned. Quick reply will be greatly appreciated.

Dear Mr. Sumit,

Thank you for your congratulations and keen interest in the performance of Hariom Pipe Industries Limited. We truly appreciate your support and dedication to understanding our company in depth.

Allow me to address your queries:

-

Regarding earnings conference calls, while it’s true that we haven’t held such calls in the past, we are actively working on initiating them in the near future. We understand the importance of transparent communication with our valued investors, and conducting earnings conference calls will be an integral part of our efforts to enhance shareholder engagement.

-

Concerning our cooperation with rating agencies, we want to clarify that Hariom Pipe Industries Limited has been engaged in an External Credit Rating process with CRISIL LTD for the past 4 to 5 years, resulting in an A- Rating. The agreement with CARE RATINGS had lapsed, but they retain the authority to continue the process. We are currently in discussions with CARE RATINGS to formally conclude the agreement and withdraw the rating process from their purview, adhering to all legal procedures.

-

As for raising equity funds, there are no immediate plans to pursue this avenue. We believe in prudent financial management and are committed to exploring various financing options to support our growth ambitions without compromising on the interests of our shareholders.

It’s important to note that Hariom Pipe Industries Limited remains dedicated to keeping our shareholders informed about all significant developments related to the company. We consistently update pertinent events through the stock exchange, ensuring transparency and accountability.

Furthermore, we are actively working on organizing conference calls with our shareholders, providing a platform for direct interaction and sharing insights into our performance and future prospects.

Your continued support and interest in Hariom Pipe Industries Limited are invaluable to us, and we look forward to your ongoing partnership as we navigate the path to sustained growth and success.

Thank you once again for your inquiries, and please feel free to reach out if you have any further questions or require additional information.

Thanks & Regards

Rudra’s PF and Information attic (29-03-2024)

Hello Mudit,

I don’t invest through mutual funds. I track my portfolio returns against an weighted benchmark as mentioned above

BSE (Bombay Stock Exchange)- Bet on Financialization? (29-03-2024)

Quick snap shot of BSE’s performance during the quarter:

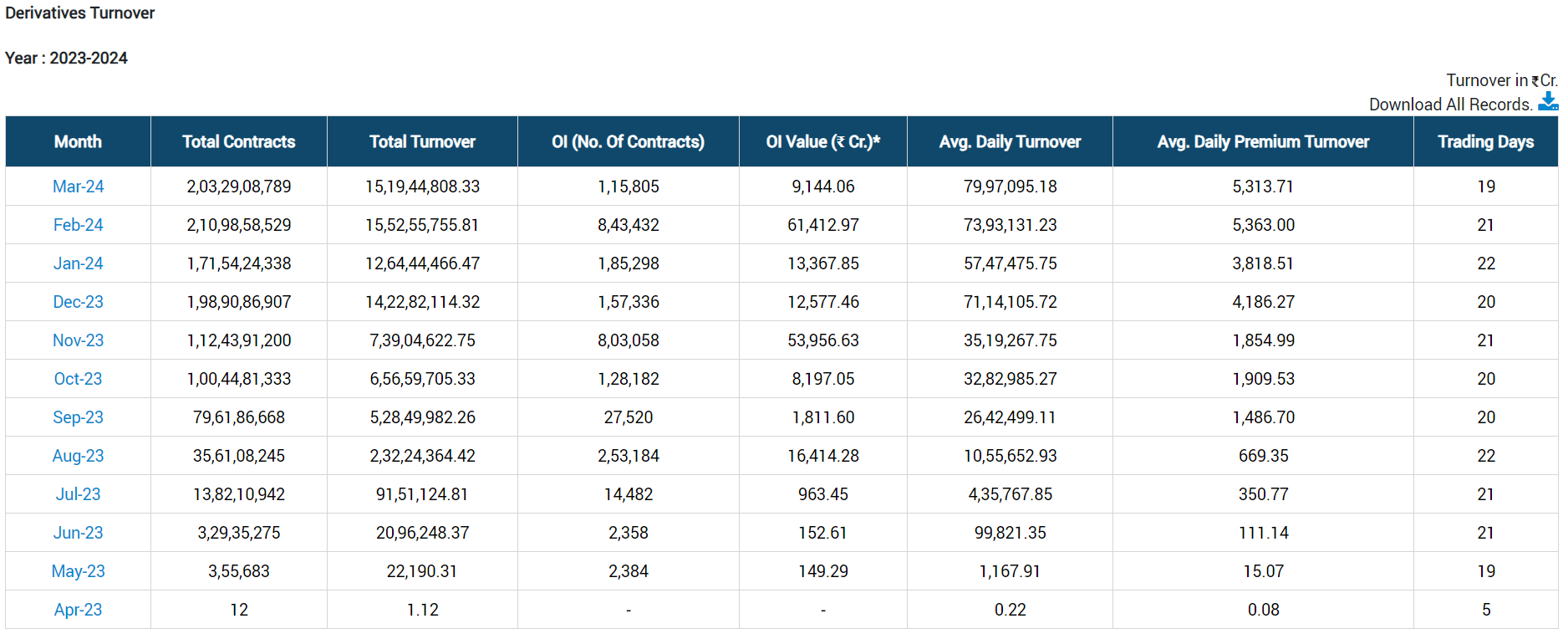

Derivatives:

The Sensex derivatives volumes remained largely range bound during the quarter. Bankex volumes are picking up slowly. The average daily volume improvement is largely on account of Bankex growth.

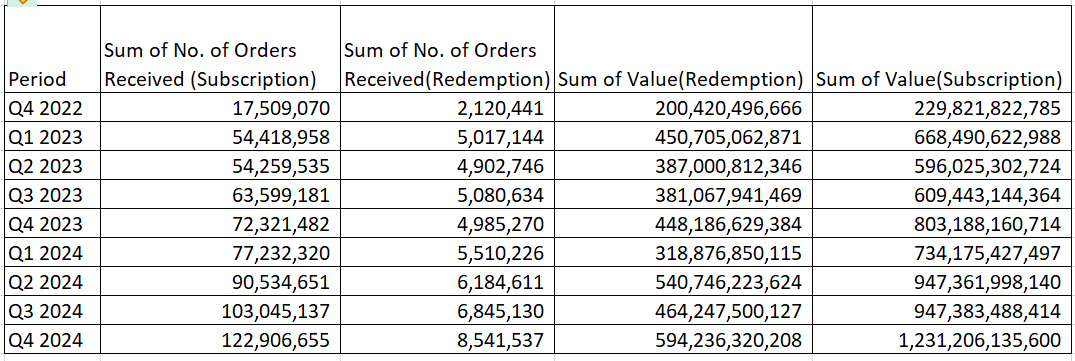

Star Mutual Fund:

Robust growth in subscriptions and redemptions orders – Noted nearly 70% growth in both subscription and redemption as compared to Q4 2023. Expect this segment to deliver its best ever results till date.

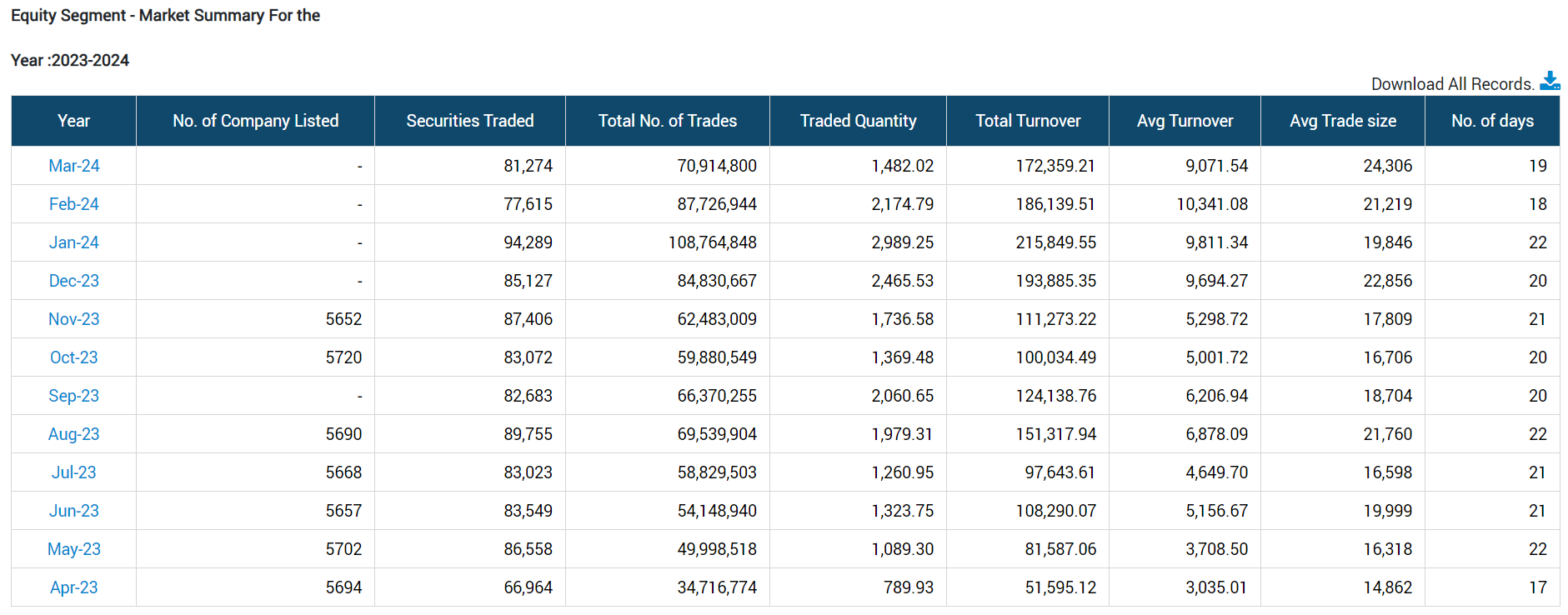

Cash segment:

The cash volumes are improving – have a look at the market summary below. The segment result should reflect this growth.

The commodities and currency derivatives segment is drying up and i’m not really sure about the reason for the same.

Overall the numbers that will get reported during the quarter will be robust and are likely to be the best in the history of BSE.

Thank you!

AJ

Disclaimer: Remain invested from last many years. Views are based.

Happiest Minds Technology (29-03-2024)

HDFC Securities initiated coverage on Happiest Mind. Really interesting read if someone wants to understand how IT companies are valued.

https://www.hdfcsec.com/hsl.docs/Happiest%20Minds%20-%20IC%20-%20HSIE-202312051305467994050.pdf