Detailed risk analysis is missing. The thread remains locked till you comply.

Posts in category Value Pickr

Exhicon Events Media Solutions Ltd (27-03-2024)

Please read forum guidelines properly before initiating a thread. FAQ – ValuePickr Forum

To nurture a vibrant community ValuePickr does not restrict anyone from starting a thread on a stock of his/her choice. Only Caveat is if you are going to introduce a discussion on a stock, we expect you to do your homework and start the thread with some basic info-set, and 1st level analysis such as growth drivers, a few positives & negatives, immediate triggers if any, and enumerate some RISKS. Nothing very heavy is required, but enough to set the tone for 2nd level of discussions.

Starting a New Thread: Please follow these guidelines – #2 by Administrator Thread initiators are usually alerted to edit their post, and make necessary changes before thread is opened up again. So you/colleague and look to edit the post in order to meet prescribed guidelines. We have the responsibility – especially the thread initiator (assumption is he/she is a savvy investor) – to cater to bringing everyone on same page – quickly – if you know what we mean.

Wockhardt – A story with twist and turn (27-03-2024)

15f30474-d756-4eb2-b7ea-1c913dc3013c.pdf (bseindia.com)

480 Crores QIP done. Institutional investors including ICICI MF, TATA and Mirae,and MK among others.

Pokarna Limited: (27-03-2024)

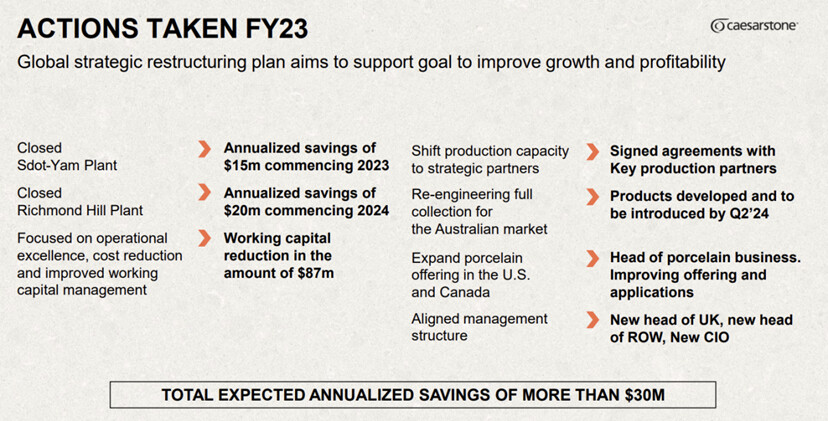

“In the second quarter of 2023, we made a decision to close our Sdot-Yam manufacturing facility. And in December, we announced the closing of our Richmond Hill facility. Following these strategic changes to our operations, we are now sourcing over 40% of our products from production business partners. We expect that percentage to trend up further as we move through 2024.”

Would this be beneficial to Pokarna growth prospects ?

Rajesh’s portfolio (27-03-2024)

Sir ji are you present in twitter or anyother way to connect to you? My mobile number is 97 89 89 9393

Kama Holdings Limited (27-03-2024)

Historically, whenever SRF is uptrend HoldCo discount in Kama has increased & whenever SRF is stagnant or in downtrend ; HoldCo discount has decreased.

Couldn’t get the logic, have back tested for last 9 years this pattern has emerged.

52 week highs and all time highs strategy (27-03-2024)

Usha Martin 200 dema currently is at 299. Stock price recently went below that level and traded and closed below that level for a few days and now has bounced back above that. Double top was at around 375 and intervening bottom is at 253. That level of 253 seemed like a panic bottom and effectively stock price has been taking support at around 270-275.

Here we have a fair idea about fundamentals of the company and the reason why the stock price is under constant pressure. Fundamental performance remains good and with capex benefits coming on stream in a quarter or two, I would like to keep observing how the company performs. Many a times abatement of selling pressure itself can cause a rally in stock prices. If Prashant Jhawar group were to stop selling for some time, we can see some uptick in stock price. The heartening thing to see for me was that most of the supply was getting absorbed above the support zone of 270-275.

Usha is one stock where I have had fundamental conviction right from the entry point and that has helped in me managing to hold on to the stock (and adding at appropriate times ) during long periods of consolidation.

Above is my thesis of investing and holding in Usha and not an investment advice.

Som Distilleries and Breweries (27-03-2024)

@manhar the promoter has in effect purchased 10% of the company at 30cr instead of 200cr. And people are willing to look at his 2cr worth market purchase and claim that he is minority shareholder friendly. Does this not set a very bad precedent? Should they not be penalised with a very low multiple (like Lux etc?)

Gabriel India Ltd. – Shock free ride? (27-03-2024)

I would like to bring Gabriel India share back up again on the radar again as there is a good buying opportunity after the 25%+ correction.

Few things to keep in mind:

- With 60+ years of operations, Gabriel India is India’s largest and is one of the top 10 largest suspension manufacturers globally.

- The company has four product segments:

- 2-3 wheelers which contributes to 64% of total portfolio sales and commands 32% market share;

- passenger vehicles which contributes to 22% sales and commands 23% market share;

- the commercial vehicles which contributes to 12% sales but commands a whopping 89% market share and

- finally aftermarket with 40% market share.

-

With a production capacity of 24M units, it is the only company which is present in all the 4 segments

-

There are two new areas (both high-margin) that Gabriel India will further diversify into in 2024:

-

This firm diversified its offerings by successfully launching sunroofs for Hyundai Creta in a Joint Venture with Dutch Sunroof specialists Inalfa. This venture is expected to generate 1000 cr. In revenue by 2030.

-

This is India’s first indigenous company that makes shock absorbers for trains (e.g., Vande Bharat and Rajdhani). As of today, they have exclusive supplier rights and can work in their favor esp. with Indian government’s push to modernize indian railways.

-

Currently, only 4% of the market is global in nature. However, with new international orders, new joint ventures and push from the company for aftermarket sales in Latam and Africa – this share is expected to rise.

-

Gabriel India is a part of the Anand Group which operates 21 auto ancillary companies and has established multiple technical partnerships to drive the group R&D. It also created a new subsidiary called Anevolve EV and signed 3 JVs to create wide range of EV products. This allows Gabriel India to access deep customer insights from its sister companies and unlock strong OEM relationships globally.

-

From an equity research analyst perspective, they are anticipating a 40% upside on the stock with revenue growth of 12% and profit growth of 22% – all bullish on revenue diversification, demand uptick and healthy market share across segments.

-

Based on my valuation models (football field with relative, DCF) – the stock is undervalued at the moment by 10% – 150% across the different valuation metrics that you take.

So overall, its an interesting gem that needs a revival after the current sideways run is complete.

Please check out the link (5 minutes) where I further structure this detail out. Your feedback will help me course correct and increase the depth of my analysis:

Gabriel India | Fundamental Analysis of the Automotive shock absorber leader!

MOLD TEK PACKAGING—dividend plus growth (27-03-2024)

Thanks Mudit and Pragnesh for an illuminating discussion,

I have a slightly different point of view. At the end of the day individual stock CAGR is an useless metric for an investor as any PF will have lets say a median retail investor will have lets say 10-20 shares in the PF.

All that matters is PF CAGR. To expect that all shares will be at high points throught is impossible. What is the probability that the share you have swapped into will continue to go up and will not stagnate or drop below.

4 years of a mega bull run has conditioned us into thinking we can time a stock.

Hindsight is golden. The Future is uncertain.

This is my extremely limited non expert and maybe dumb 2-cent view.