In Arihant conference today, management gave a guidance of Billion Dollar Revenue target with 10% margin by 2030.

Posts in category Value Pickr

Kitex Garments Limited (26-03-2024)

As per the interview with Sabu M Jacob – it seems like they gave 25 Crores to Telangana party through Electoral Bonds. It is still kept as Privacy per Law – many companies do that including Bajaj Finance.

Company is having 3-5X Expansions in Telangana & That is what we Investors should focus for.

So no ground on CPM funding – as CPM is biggest troublers for them. (although they paid lower amounts as contributions to all parties including cpm)

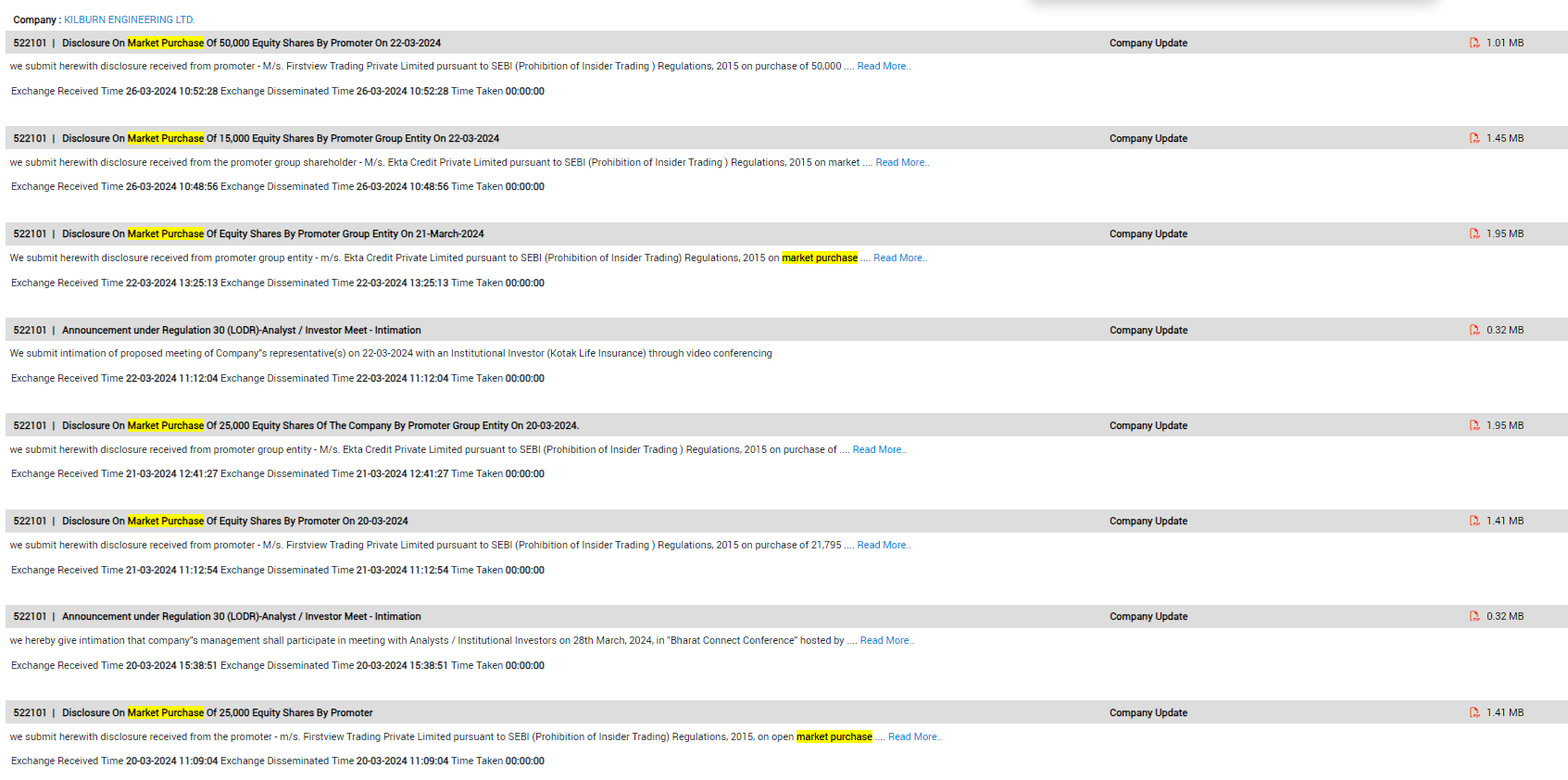

Kilburn Engineering – Huge undervaluation (26-03-2024)

Promoters have been continuously buying from open market in March. They bought more than 2L shares in March.

Paushak Ltd. – Alembic’s agrochemical business (26-03-2024)

Any view w.r.t holding.

Moldtek Technologies (26-03-2024)

Actually the owner being Mr J. Lakshmana Rao boosted my confidence in this company and was a major factor in buying this as my thought process is, if he built plastics to what it is today at an impressive growth, he can do the same for this, and till now YoY it has proven right. Their reviews online by employees is rather poor and is an issue to consider.

Kama Holdings Limited (26-03-2024)

SRF is approaching 52 week high and rebounding. Parent company Kama Holdings is not reflecting the value in its price action yet. Kama Holdings alternatively is closer to its 52 weeks low.

Any thoughts on this divergence?

52 week highs and all time highs strategy (26-03-2024)

Hitesh Bhai, Per my understanding, 200D.EMA had flattened & a double top pattern was evident on the daily chart after a long uptrend. Price broke below 200D.EMA in the last week. I felt that the current week’s closing price will confirm/disconfirm the double top pattern.

Do you think otherwise?

Disc: No position. Just curious to learn.

IBC referred Cases: Value investing or Value trap? (26-03-2024)

@Amit2saxena asked me a question, which i think might help everyone

the question was-

in ongoing IBC, if there is agreement between CoC and aquirer and 1) company owns valuable assets and 2) plan is to keep the company listed, then case becomes very interesting.

Example – 1) Amusement park of Imagica 2) Processing plants of Ruchi Soya

In the cases that I mentioned above, what part of the asset base i found interesting. For example, in case of Golden Tobecco or MT Educare?

my answer-

in golden tobacco its not about the assets, its about the list of prospective resolution applicants, i have never seen that many individuals being interested in any firm. In any of the IBC cases i read, i do not give any particular preference to assets, if its there then its a bonus.

I have a very simple strategy to follow change, any business going from 0 to 5 or 0 to 10 will give the same returns till a particular point (10 being the firm with strong assets and value and 5 with nothing special or significant), so i need to hold the firm till that particular point and then understand its value, in this way i broaden my target area (universe of firms), while also not getting paralysed while analysing the small units of data which prevents me from cashing out alpha till that particular point.

Cineline India – Picture abhi baaki hai (26-03-2024)

Has management given any commentary on slow screen growth this year?

They had added 60+ screens in FY23. They have added less than 10 screens in FY24. Each screen contributes to 8-10 Cr valuation.

Investor value creation only happens through screen addition in movie business. You can play with 10-20% with ATP + SPH increase. For multibagger returns, they need to add 30-40 screens every year.

I see only 2 possibilities – Sell hotel/ Dilute equity and bring growth money.

Companies with 20%+ growth guidance for next few years (26-03-2024)

Hi Anant,

I am not sure if there is a sureshot way to know if management is acting in their interest or that of shareholders. (If there was, I’m sure no Enron would ever happen.)

What an aam investor can do is some due diligence and hope (or pray) that things won’t go south.

What I do with my investee companies (small caps) is to read quarterly concall transcripts and check quality of answers management provides to analysts’ questions. I also follow corporate actions (e.g. fund raise, preferential allotment), third party transactions, legal disputes, relevance/quality of investor announcement (and their timings) etc. If something seems odd or fishy, I either get out of stock or avoid it completely (if I’m not invested yet).

Others may debate this approach but I feel at peace knowing that I’m not stepping on a visible landmine.

There is no guarantee that I wouldn’t end with odd companies with hidden landmines and that’s the risk I will have no choice but to accept. As they say in stock market it’s important to not only have rules for what you want to buy but also have rules for what you will never buy.