VDEAL_28102024113418_New_Order_Announcement_28102024 (1).pdf (1.9 MB)

New order

Disclosure: invested

VDEAL_28102024113418_New_Order_Announcement_28102024 (1).pdf (1.9 MB)

New order

Disclosure: invested

New update and guidance:

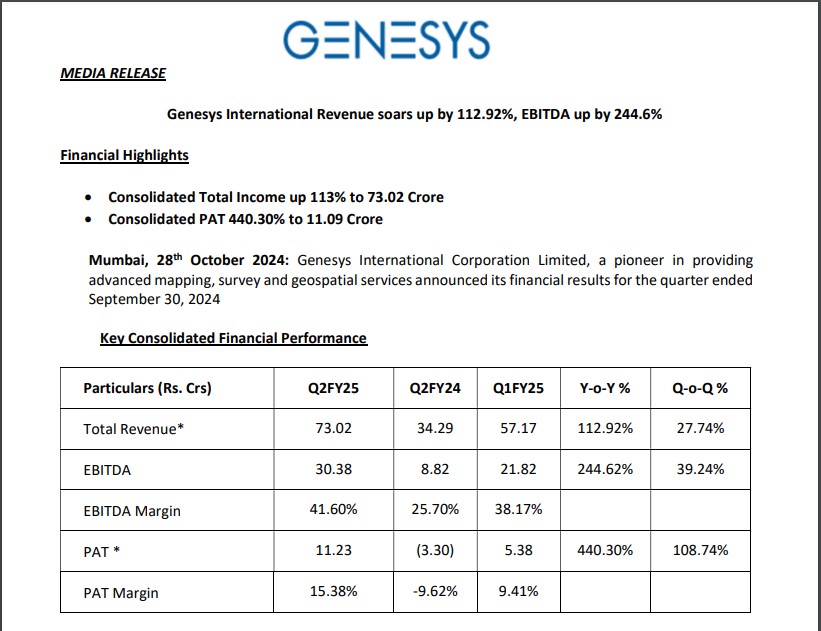

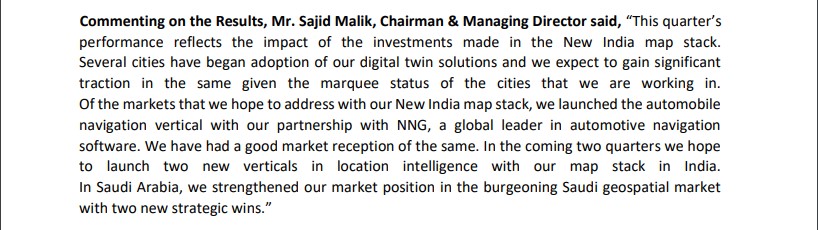

40123e4e-4d13-4031-bb1d-4de4356cc182 (1).pdf (540.8 KB)

Market Focus and Strategy

Distribution Market Shift

Recent Developments

Pipeline and Revenue Growth

Product Strategy

Seasonal Trends

Partnership Strategy

Core Banking Insights

Insurance Sector Focus

My Take:

This quarter exemplifies a recurring situation in which product sales do not materialize, leading the management at Intellect to depict a narrative of missing or delayed sales for certain products. Such delays occur with such frequency that it becomes impractical to concentrate excessively on quarterly figures beyond a certain threshold; however, management continues to emphasize this issue repeatedly over the next four to five quarters.

Furthermore, management places considerable emphasis on achieving a compound annual growth rate (CAGR) of 15-20%, which may appear acceptable from a year-over-year perspective but does not translate effectively into quarter-over-quarter results. The second quarter was illustrative of this trend.

Management often adopts an optimistic tone, and should they exceed sales of 700 units within the next three quarters, as Mr. Jain indicated, they would offset the loss in profit after tax experienced in the second quarter.

Intellect is making strides in the U.S. market; however, their performance regarding Banking and Transaction products—central to their operations—has been less impressive. While their progress in Insurance is satisfactory, its profitability relative to core banking products remains uncertain.

I express caution regarding their approach to System Integration (SI). They have partnered with major SI companies such as IBM, HCL Tech, Wipro, and Accenture. Unless these firms generate revenues between $30-$50 million through their partnership with Intellect, significant commitments are unlikely. Since many of these SIs are joining simultaneously, it will be intriguing to observe how these collaborations evolve. Ideally, Intellect should have initiated partnerships gradually with a select few SIs before expanding further; instead, they opted for a more aggressive strategy. On a positive note, some of these SI partnerships could yield substantial benefits outside the U.S.

For instance, HCL Tech acquired IBM’s product portfolio four to five years ago and has since established client relationships in over 100 countries. Intellect can undoubtedly enhance its reach through these extensive distribution channels. If Intellect succeeds in improving its sales via SIs, significant margin improvements could follow; however, this will likely involve increased costs over the next two to three quarters.

TMB Ltd – Q2FY25:

Interest Income : 1,337.41Cr ( 4.3% QoQ )

Total Income : 1,564.88Cr ( 3.3% QoQ )

PPOP : 465.20Cr ( -0.7% QoQ )

Advances : 42,156.14Cr ( 4% QoQ )

Deposits : 49,342.16Cr ( 0.3% QoQ )

BVPS : Rs. 532.38

NIM : 4.25%

GNPA : 1.37%

NNPA : 0.46%

Cost to Income : 43.51%

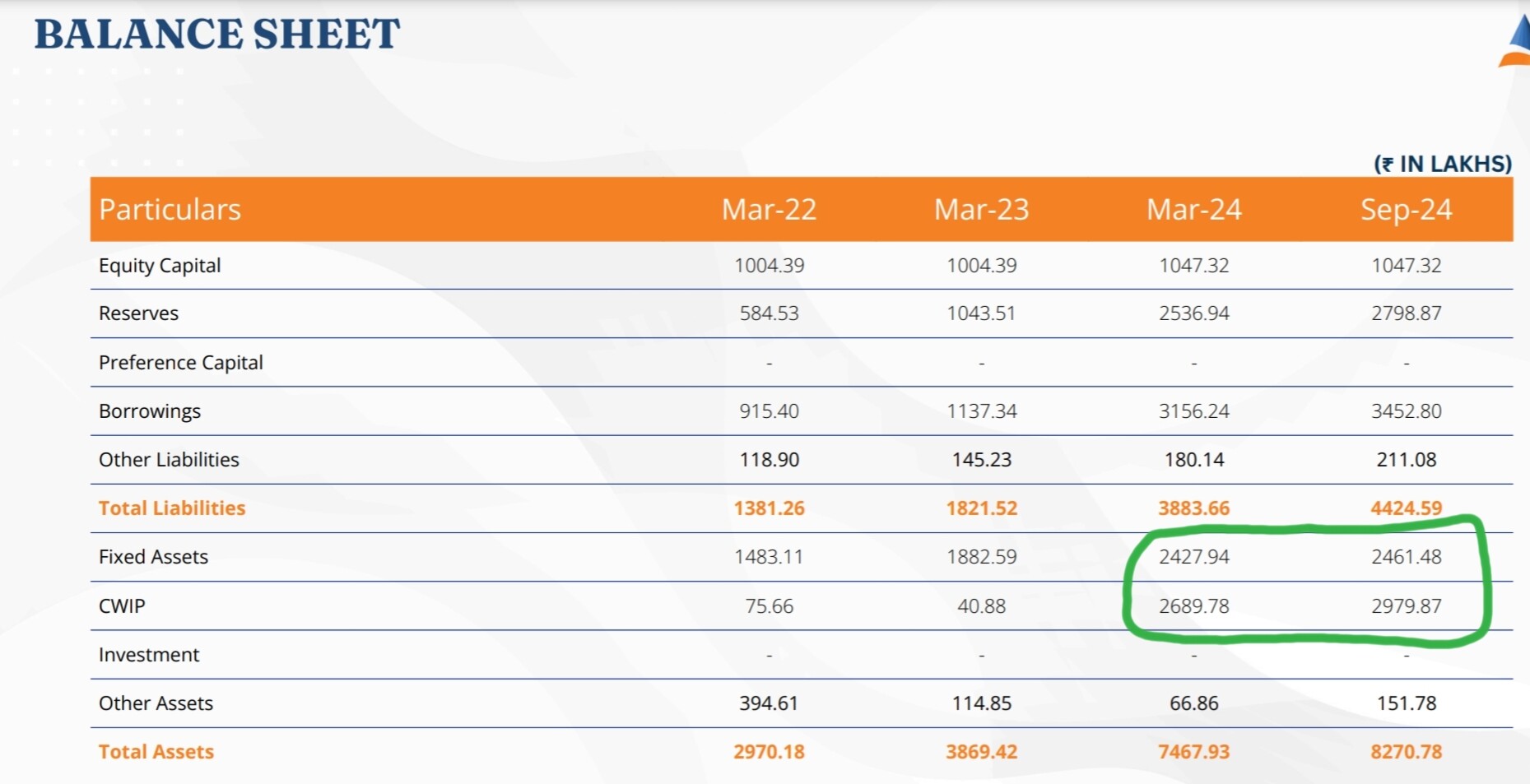

Is the capex completed/completed partially?

If yes why hasn’t the cwip amount converted to fixed assets?

@Investor_No_1

Thanks for seeking my view. Since my basic thesis for investment for high dividend yield, I would critically evaluate hotel business, which is not generally free cashflow generating. However, the company has created excellent brand and among Top 5 Luxury hotel player in India as per my understanding. If it truely follow “Asset Light” business model, then can generate cashflow for paying dividend. Hence, subject to relative valuation, I shall wait for 6-12 months to decide whether to continue to hold Hotel business share or exit. At this stage, it would be difficult for me to take decision.

Having said that, every investor has his/her own aspiration, profile and risk return expectation which are unique. Hence, would suggest every investor to evaluate hotel share investment as a new company being added to portfolio and follow same parameter which they follow while addiing/miniotoring porffolio Companies. There can not be standard asnwer to question. So would suggest each investor to decide on their own behalf.

Discl: ITC Limited is my largest holding. I may add/reduce/exit from the company without informing the forum. I not SEBI registerd advisor. I am not suggesting any investment decision by investor in the message. I have not traded in ITC for last 3 months.

Results are quite lukewarm. CDO/CDMO business has been slipping down further and not sure if management will be able to scale that up. It’s not an easy business and very few in India have been able to establish presence in this space.

Only bright spot was margins that picked up this quarter but still doesn’t compensate flat topline.

Disc- Small quantities received from Aarti Industries merger. Keeping for tracking purpose as I’m also interested in their CDO/CDMO play.

Today’s order qualifies as this Marquee order inflow.

After the initial 16cr trial order from Lockheed, today’s 380cr order is a massive statement, of intent.

Good results IMO.

September 2024 quarter results declared. Sales down 15.5% y-o-y. Sharp contraction in operating margin. Sequentially, the contraction in operating margin in just 40 basis points. Let’s see how price reacts.