I learnt from @Worldlywiseinvestors that it is a red flag … not personally but through their videos .

Your views please noob here

I learnt from @Worldlywiseinvestors that it is a red flag … not personally but through their videos .

Your views please noob here

Non cooperation by Issuer

CRISIL Ratings has been consistently following up with Deep Industries (DI) for obtaining information through letter and email dated January 05, 2024 among others, apart from telephonic communication. However, the issuer has remained non cooperative.

‘The investors, lenders and all other market participants should exercise due caution with reference to the rating assigned/reviewed with the suffix ‘ISSUER NOT COOPERATING’ as the rating is arrived at without any management interaction and is based on best available or limited or dated information on the company. Such non co-operation by a rated entity may be a result of deterioration in its credit risk profile. These ratings with ‘ISSUER NOT COOPERATING’ suffix lack a forward looking component.’

No Concall was conducted this time after Q3 results. But an interview with Rishi Sanghvi was there instead of it.

Reviewing Sanghvi Movers and Apollo Hospitals’ Q3 Results | India Market Open | NDTV Profit

Is that allowed by SEBI.

Can Niyogin Fintech be the true player of digital transformation and financial inclusion partner of India?

Who I am: The company operates on a tech-centric platform-based model offering Banking as a Service (BaaS) through our subsidiary, iServeU and credit solutions to both rural and urban areas in India. We employ a partnership-led strategy collaborating with local enterprise partners that possess extensive distribution networks. These partnerships allow us to leverage the partner’s infrastructure for cost-effective outreach to our targeted customers primarily micro, small and medium enterprises (MSMEs).

Once we onboard a partner, iServeU’s Banking as a Service (BaaS) platforms are integrated into the partners’ customers’ facing touch points. This integration enables these touch points to offer banking, payment, and financial services to their local clientele. By adopting this partner-led approach, the Company can effectively extend its services to a larger number of MSMEs and SMEs through each partner it engages with. The revenue model primarily revolves around transaction fees or commissions earned on every transaction processed through the platform. As an NBFC, Niyogin extends its services to MSMEs by providing credit. They facilitate lead generation and provide digital access to credit and other financial services for MSMEs through our distribution platform NiyoBlu and also by our several Fintech partnerships. Niyogin employs various lending models and generates revenue through either interest income or fees associated with loan lead generation.

“Consolidated Financials” for the Quarter: Revenues stood at Rs. 53.8 crores up 99% year-on-year and 13% quarter-on-quarter. The revenue increase was driven by the prior quarter service revenue and a marginal sequential improvement in Take rates. The adjusted EBITDA loss gap narrowed from Rs. 8.2 crores in Q2 FY24 to Rs. 1.4 crores in Q3 FY24 due to improving economics in the lending and distribution business. ESOP charge for the current quarter was Rs. 0.3 crores versus Rs. 1.1 crores in the previous quarter. The non-GAAP PBT stood at Rs. (4.5) crores in Q3 of this year as against the non-GAAP PBT of Rs. (10.1) crores in the previous quarter. The consolidated cash and cash equivalents stood at Rs. 93.1 crores as on 31st December 2023.

Key development:

Momentum investing in any form and following anyone you learn from will involve putting trailing stop losses to your positions at an appropriate parameter/support etc. This is to protect your profits if you are in a profitable position once you have bought, or limit your losses in any fresh position you have taken.

Growth investing is a totally different kettle of fish. Here you have to do your fundamental analysis and if you are into technicals, apply some knowledge of that to fine tune entry points. You can go through the threads of multibagger stocks, or read few books to get better at how to choose growth stocks.

Another acquisition in Bijnor UP

in continuation of our disclosure of outcome of Board Meeting dated March 12, 2024, we would like to

inform you that the Company has completed the acquisition of 100% equity stake in Healers Hospital

Private Limited (“HHPL”) by entering Share Purchase Agreement with existing shareholders

with an acquisition of 100% equity stake for a consideration of Rs 104 Cr (approx). This equity stake will be acquired within a period of one month, through secondary buy‐outs.

This investment is in continuation with Shalby’s strategy to consolidate asset base for its recent

acquisition of Sanar International Hospital (P K Healthcare Pvt Ltd.) at Gurugram.

Sanar International Hospital is currently operating under leased land held by Healers Hospital.

With this acquisition, Shalby has changed its business model from Leased model to owned

model for its recent acquisition of Sanar International Hospital in Jan 2024.

With this acquisition, Shalby will unlock the consolidated profitability of the group to the tune

of leased rentals expense, ensure the lifelong continuity of Sanar Hospital at owned land model

and also unlock the future value of asset being present at a prime location i.e. Golf Course Road,

Gurugram.

Bijnor is 1 Lakh population town, hospital is new, have good land and built up. But seems ramp up is very slow. But given the linkage with Sanar, we can consider it as single acquisition.

But why Shalby was the preferred choice for the selling management? It seems good asset even for big hospitals!

Disclosure: Invested

@kuldeep_agarwal Your strategy might also work.

What I suggested was slightly different. You have to do ranking 3 times.

This is the simplest and easiest way to start a momentum portfolio. You can add more factors to reduce the volatility or reduce drawdown etc.

But this should work for you well.

I would like to bring PCBL share back up again on the radar again as there is a good buying opportunity after the 20% correction.

Few things to keep in mind:

PCBL Ltd is India’s largest carbon black producer and the 7th largest worldwide. Infact, it commands a 35% – 40% market share of the domestic carbon black market, with other players having sub-20% market share.

The firm operates in three major segments: Rubber Black – Tyres ( 65% of the revenue), Rubber Black – Non Tyres (25% of revenue – e.g., conveyer belt, industrial hoses) and specialty chemicals (10% of revenue – e.g., foodplate, print ink, camera body etc.)

There are two new areas (both high-margin) that PCBL will further diversify into in 2024:

Currently, 70% of the overall demand is domestic in nature. Domestic demand for carbon black is increasing, driven by the expansion of tyre manufacturing capacities, reduced tyre imports from China, heightened demand for PV/CV/tractor tyres, specialized tyres for EVs and rising tyre exports due to anti-dumping duties on Chinese tyres.

In addition, with the global restriction (anti-dumping) on Chinese Carbon black, reduced consumption of Russian Carbon black due to war and regulatory constraints on European and North American production has opened a huge international market demand for PCBL. It now operates in 50+ countries.

Future trends: Over FY23-26E, the sales volumes of rubber black is anticipated to experience a CAGR of 8.5%, In same breath, the volumes of performance black and specialty black are projected to witness a CAGR growth of 17% and 23%.

PCBL is a part of the RP-Sanjeev Goenka Group of Kolkata which operates other listed companies like CESC in power, Spencer in retail shopping, First source which is a BPO, IPL team – Lucknow Giants and others. Most of its companies are AA-rated, so being part of this group gives PCBL a very strong financial flexibility.

While PCBL’s sales volume grew by 19% YoY but the revenue only grew by 2.1% YoY. This happened due to the 15% decline in market prices which was a direct result of oversupply of cheap Russian carbon black before active consumption restraints were placed. EBITDA improved by over 30% due to the rising share of high margin performance and specialty carbon blacks in the overall sales mix. In line, the company profits also increased by 12%.

From an equity research analyst perspective, they are anticipating a 40% upside on the stock with revenue growth of 20% and profit growth of 16% – all bullish on capacity increase and high demand across product lines.

Based on my valuation models (football field with relative, DCF) – the stock is undervalued at the moment by 15% – 20% across the different valuation metrics that you take.

So overall, its an interesting hidden gem that has the potential to grow after the correction is complete.

Please check out the link (6.5 minutes) where I further structure this detail out. Your feedback will help me course correct and increase the depth of my analysis:

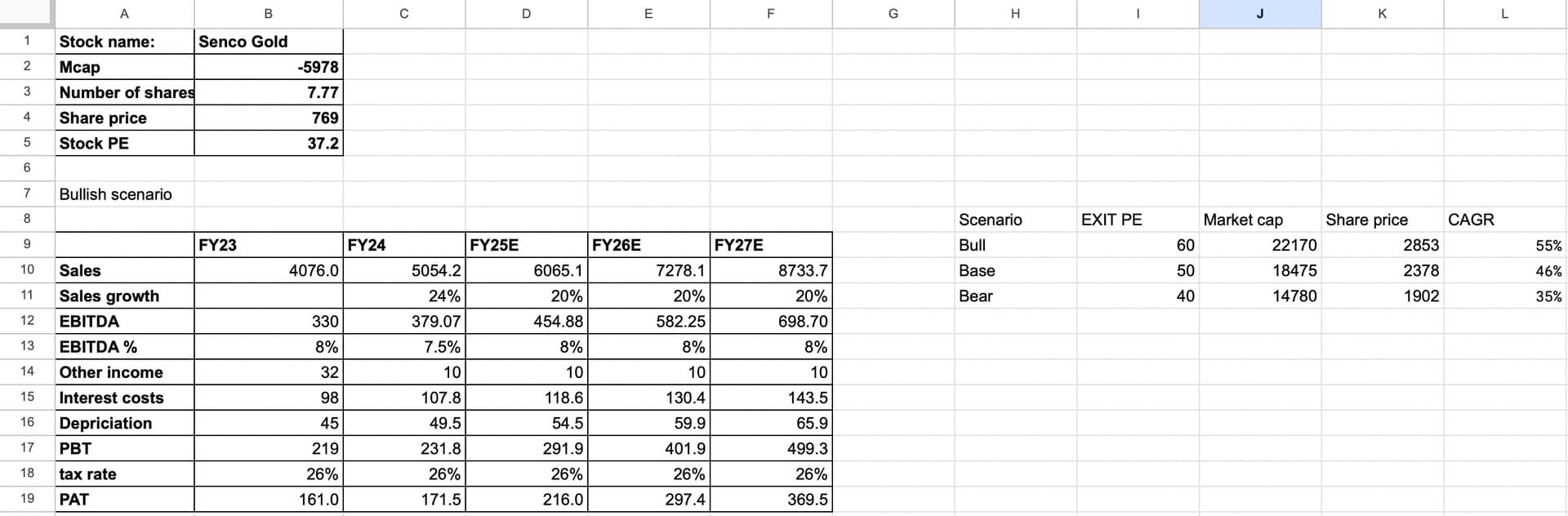

This is my financial model regarding the business

Here is my thesis

Disc: Bought in the last 30 days. No buy or sell recommendation.

Thesis

For FY24, H1 growth has been around 27% which is really great, however i want ti be a bit conservative because of the fact that Q3 base is quite large. Hence, The overall growth I have assumed for the year is around 25%, which sounds great but still could be conservative.

Now for the rest of the years, the company wants to increase the store count by around 25 something each year and reach about 250 stores which seems possible. Current store count is 153 and 10 should be added by FY24 so around 163. With an SSG of double digits, and 15%+ growth in number of stores, even 20% growth in revenue seems very conservative.

Regarding EBITDA,

This FY24 there seems to be inventory losses due to Diamonds, and hence i expect the margins to decline a bit, however we can assume this problem to solve and revert back to mean. Even though the studded ratio is increasing, the company mentioned that it will probably get offset by entering into new markets and more competition, as mentioned in Q1 concall. Another point, the margins were on the higher side last year due to diamond prices and hence we shouldn’t expect increasing margins, mostly stable or even around 7% because of franchise additions and growth phases of the company. I have opted for 8% but I think( could be wrong so correct me whenever) 7% too is a reasonable assumption

Interest costs and depreciation

During the H1 balance sheet, lease liabilities increased by around 10% and hence assuming a 10% increase is possible in depreciation and Interest costs. With the own store additions of our 10%. Its safe to assume these two ill increase by the same range.

PBT

I do have a problem with PBT for FY 26-27. The PBT is more than 5% which seems a bit hard to believe because it’s difficult to achieve a PBT of 5%+. It’s probably possible if operating leverage plays out, which is a thesis pointer.

Valuations

I would not wanna assign the valuations of Titan and Kalyan, since i haven’t studied titan i can’t say much about it but Kalyan does look overvalued. It should command a higher multiple than now, but it does depend on its ability to become a Pan India player. Secondly, Senco has a very strong presence in the east but not much in other regions and that becomes a big risk. If anything goes wrong in West Bengal, any financial model we make will go for a toss. So that’s why, I think 1.5x PEG makes some sense to me. However, upon talking to other investors, it does make sense to me that consumption businesses get a 50x PE.

Personal opinion

There is a strong shift from unorganized players to Organized players and hence I do believe that there are strong tailwinds in the sector. I think Senco can deeply penetrate areas due to their lower average ticket size and business model, which just gives me a sense of relief that they have a lot of growth possibilities in new geographies.

However, not a lot of big pan India players have a strong presence in the east and hence it will be interesting to see how Senco tackles the big boys in other regions.