@Sujata This is a different style of investing. Here we don’t look at the fundamentals. Just check price action and then enter / exit as per set of rules. We should look at pf returns instead of individual stocks.

If a stock continues to perform well, there is no reason to exit from it. I have several stocks in the pf that have given me already 2x, 3x returns.

Posts in category Value Pickr

Microcap momentum portfolio (24-03-2024)

Microcap momentum portfolio (24-03-2024)

@krishnasristy Every weekend, I pull the data from Google Finance (I don’t enter data manually). After that I have to make some small tweaks in the template and the data is ready. Not very difficult.

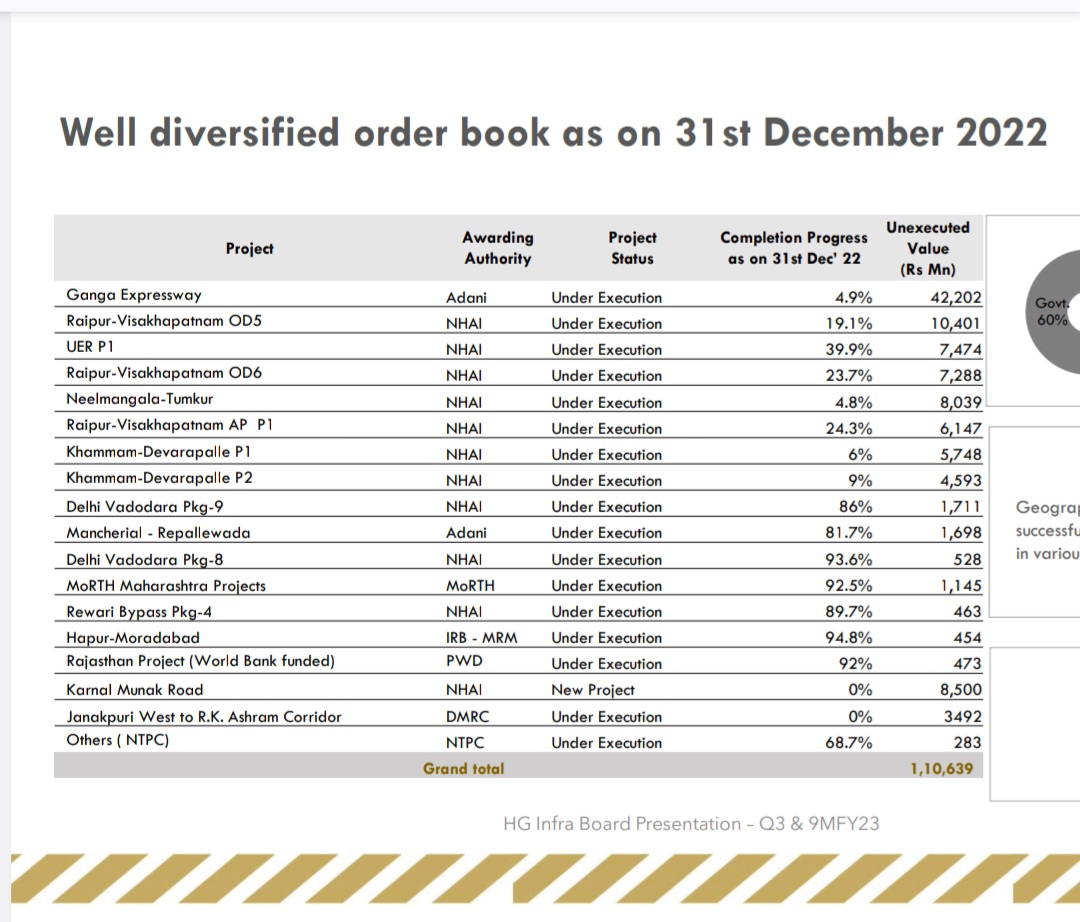

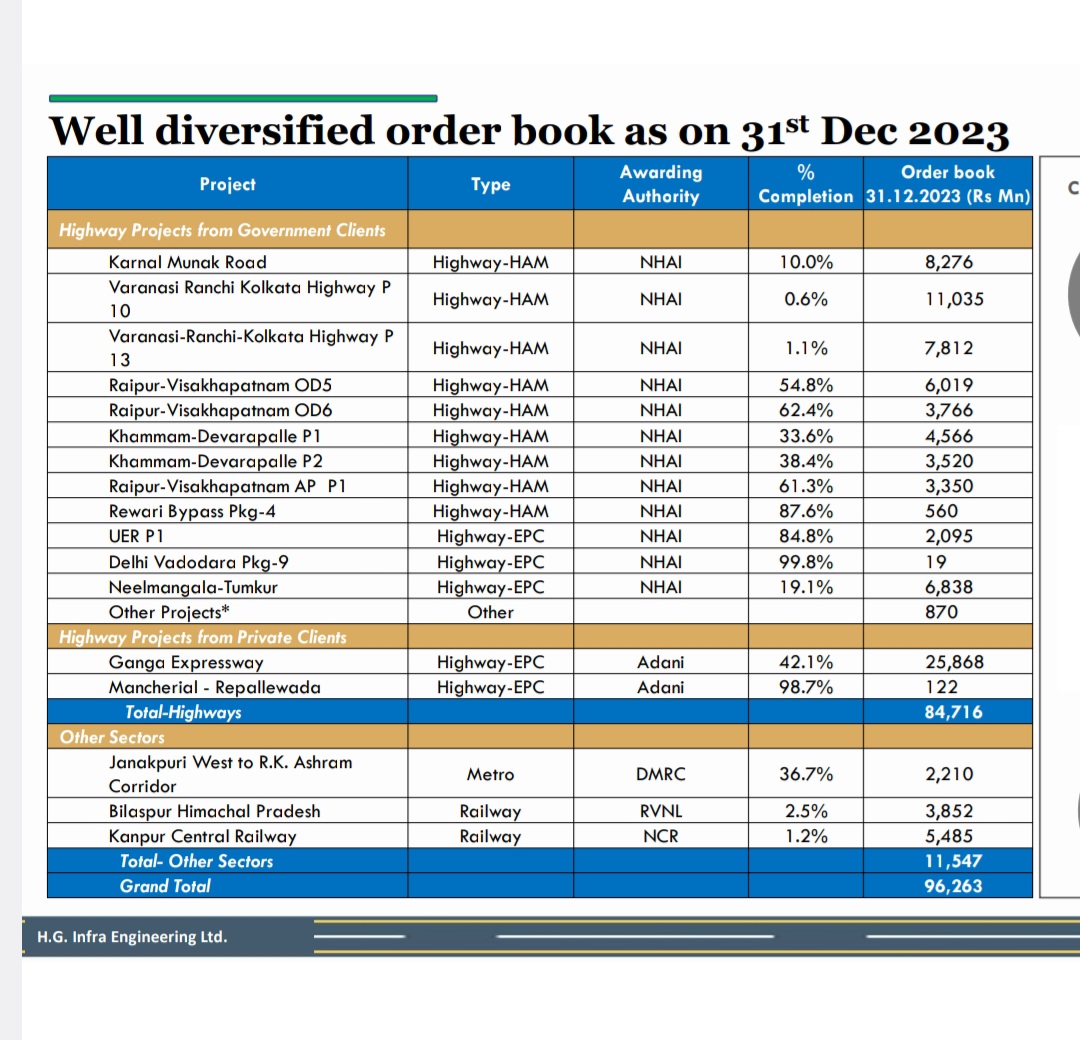

H.G. Infra Engineering Ltd : Paving the Path to Success (24-03-2024)

Sharing with you some numbers of #HGINFRA

● Imorovement in orderbook

As of Dec 2022 = their orderbook was 98% Road, 2% Rail

As of Dec 2023= Their orderbook was 87% Road + 13% Railways

As of today= Their orderbook is 72% Road + 22% Railway + 6% Solar

● Orders received in last 3 months

Railway= 1872 Cr

Highway= 1472 Cr

Solar= 1560 Cr ( Joint venture )

As of today their orderbook

Road= 9940 Cr ( less this quater )

Railway= 3000 Cr ( less this quater )

Solar= 1560 Cr ( Joint venture )

Current orderbook is at about 2X/ FY 25 sales & much better award wins are expected in FY25 after election

In last concall, company has guided for 6k Cr topline, 15-16% Ebidta, 10-11% PAT FY 25

Disc: Invested since 2021 – sold some last yr ( to make my invested capital free at about 4x gains & to invest that in other sector ) now adding on dips this year, as orderbook looks much diversified, May be biased – sharing for learning

Nilkamal – Back on Track? (24-03-2024)

@ranvir : Incase it’s still in your radar, I seek your synthesized view for the Nilkamal’s business.

Microcap momentum portfolio (24-03-2024)

No. There is no analysis of business done here.

You can go through this thread to have an understanding.

Microcap momentum portfolio (24-03-2024)

Ok, On the contrary you mean to say one identify and grab value multipliers at nascent stage?

Microcap momentum portfolio (24-03-2024)

@visuarchie How do you update this? All manual?

PCBL Limited – Is the market correction an opportunity to enter? (24-03-2024)

I would like to bring PCBL share back up again on the radar again as there is a good buying opportunity after the 20% correction.

Few things to keep in mind:

-

PCBL Ltd is India’s largest carbon black producer and the 7th largest

worldwide. Infact, it commands a 35% – 40% market share of the domestic carbon black market, with other players having sub-20% market share. -

The firm operates in three major segments: Rubber Black – Tyres ( 65% of the revenue), Rubber Black – Non Tyres (25% of revenue – e.g., conveyer belt, industrial hoses) and specialty chemicals (10% of revenue – e.g., foodplate, print ink, camera body etc.)

-

There are two new areas (both high-margin) that PCBL will further diversify into in 2024:

- Post its 3800 crore acquisition of Aquapharm, India’s largest phosphonate manufacturer, PCBL gets access to water treatment sector. Aquapharm has all the largest FMCG (e.g., P&G, Reckitt, Unilever) as its clients so PBCL is inheriting a strong business base

- It has invested 130 crore to get 51% stake in the JV with Australia silicon nano-technology specialist Kinaltek limited. This will give access to battery applications esp. for EV batteries

-

Currently, 70% of the overall demand is domestic in nature. Domestic demand for carbon black is increasing, driven by the expansion of tyre manufacturing capacities, reduced tyre imports from China, heightened demand for PV/CV/tractor tyres, specialized tyres for EVs and rising tyre exports due to anti-dumping duties on Chinese tyres.

-

In addition, with the global restriction (anti-dumping) on Chinese Carbon black, reduced consumption of Russian Carbon black due to war and regulatory constraints on European and North American production has opened a huge international market demand for PCBL. It now operates in 50+ countries.

-

Future trends: Over FY23-26E, the sales volumes of rubber black is anticipated to experience a CAGR of 8.5%, In same breath, the volumes of performance black and specialty black are projected to witness a CAGR growth of 17% and 23%.

-

PCBL is a part of the RP-Sanjeev Goenka Group of Kolkata which operates other listed companies like CESC in power, Spencer in retail shopping, First source which is a BPO, IPL team – Lucknow Giants and others. Most of its companies are AA-rated, so being part of this group gives PCBL a very strong financial flexibility.

-

While PCBL’s sales volume grew by 19% YoY but the revenue only grew by 2.1% YoY. This happened due to the 15% decline in market prices which was a direct result of oversupply of cheap Russian carbon black before active consumption restraints were placed. EBITDA improved by over 30% due to the rising share of high margin performance and specialty carbon blacks in the overall sales mix. In line, the company profits also increased by 12%.

-

From an equity research analyst perspective, they are anticipating a 40% upside on the stock with revenue growth of 20% and profit growth of 16% – all bullish on capacity increase and high demand across product lines.

-

Based on my valuation models (football field with relative, DCF) – the stock is undervalued at the moment by 15% – 20% across the different valuation metrics that you take.

So overall, its an interesting hidden gem that has the potential to grow after the correction is complete.

Please check out the link (6.5 minutes) where I further structure this detail out. Your feedback will help me course correct and increase the depth of my analysis:

Microcap momentum portfolio (24-03-2024)

@Jitendra_Vyas It can be done, but I do not have the resources. Professional fund managers are doing this regularly. Zerodha has got an option called Streak that helps you to do some kind of backtesting.

Phillips Carbon Black (24-03-2024)

(post deleted by author)