Please read about Ind AS 116 Leases. Long term + short term debt is the actual debt payable. Lease liability is created on liabilities side and Right of use asset on asset side. This was done to stop hiding of commitments as they used to take it off balance sheet

Posts in category Value Pickr

Krsnaa Diagnostics – what is the diagnosis? (19-03-2024)

In continuation to your condensed notes, there is an interesting view presented at

:

Nykaa – The Make Up Company (19-03-2024)

Note on Nyka

NYKA (Mcap – Rs. 43,318 Cr)

Summary

Nykaa’s leading position drives self-reinforcing flywheels, which further bolster strong network effects. The brand affinity it has cultivated with consumers draws them to engage on Nykaa’s platform. As consumer traffic increases, so does the number of transactions on its platform. With more consumers and transactions, there is a growing imperative for more brands and sellers to associate with Nykaa, thereby expanding the choices available to consumers. Leveraging its brand strength, the company has successfully added and will continue to add more lifestyle verticals and adjacencies on its platforms, thereby expectedly increasing its consumer base. The experience flywheel further accelerates the transaction flywheel: more consumer data leads to better analytics, resulting in higher engagement and a superior experience. This, in turn, fosters the creation of more content, which further enhances consumer experience and drives transactions.

Background

In the beauty industry, Indian women previously faced challenges such as limited options and lack of convenience. Recognizing this gap in 2012, Falguni Nayar, a former senior managing director at Kotak Mahindra Capital Company launched Nykaa, an online beauty retailer that revolutionized the market for Indian women. It sells cosmetics, wellness, and fashion products through its websites, apps, and 141 physical stores in India. In 2020, Nykaa launched two new businesses: Nykaa Pro, a professional beauty services platform, and Nykaa Fashion, a fashion e-commerce platform.

Nyka’s revenue segments

-

Beauty and Personal Care (BPC) (85% of revenue)- Nykaa operates with an inventory-driven business model for the BPC category. This means that Nykaa purchases products directly from manufacturers and stores them in its own warehouses. By doing so, Nykaa can maintain control over the quality and availability of its products. Additionally, Nykaa implements an omnichannel marketing strategy, engaging with customers through various channels such as its website, mobile app, social media platforms, offline stores, and events. This multi-channel approach enhances Nykaa’s reach and allows for greater customer engagement.

-

Nyka fashion (8% of revenue) – In 2018 Nykaa launched its curated marketplace for apparels, jewellery, footwears etc. It is building up its fashion business with similar principals it used to build its BPC business: (1) strong focus on merchandising, brand assortment and exclusivity, (2) focusing on premiumization and upselling as opposed to discount-led tactics adopted by competitors.

Others ((7% of revenue) -

Nyka e-B2B – Since India BPC market may increase substantially, 41-50% consumption is expected from unorganized trade. The current distribution system, which caters to the unorganized part of the market, has a few inefficiencies such as fragmented distribution, poor credit coverage, uneven playing field (large brand dominating newer brands) etc. Nykaa plans to leverage and disrupt this via technology through its eB2B platform Superstore. Nykaa aims to buy directly from the brand, bypass middlemen (distributors/wholesalers) and directly supply to retailers.

-

NykaaMan – Nykaa launched NykaaMan mobile application/website in FY21, thus customizing models and experience for men, as also spiking education/awareness among men on grooming/personal care product use.

Industry

•A recent report by JM Financials indicates a shift towards higher BPC spending, with 16% / 14% of consumers spending Rs. 10,000-20,000 / >20,000 respectively, as compared to 8% / 6% a few years ago. The share of consumers spending < INR 2,000 has contracted from 43% to 21% now, validating the argument suggested by Nykaa that Indian per capita beauty shopping is expected to rise sharply.

•Higher skincare and haircare expenses now indicate premiumization. Also, when it’s about skin and hair, people become loyal to brands compared to when using makeup.

•Large young population driving consumption: India has the largest Generation Z and millennial population globally. According to the UN Population Division estimates for 2019, approximately 375 million Indians are Generation Z (10-24 years of age) and approximately 333 million Indians are millennials (25-39 years of age), forming approximately 51% of the Indian population. Both groups are considered India’s biggest spenders, a trend likely to increase further as they enter their prime earning and spending years.

Competitive advantages

•Omni-Channel Strategy: Building a more resilient distribution network that will allow for potential hyperlocal delivery. Nykaa leverages its omni-channel database of consumers to select store locations, design brand and assortment mix, direct traffic to its stores, plan offline beauty events and marketing campaigns, and create an experiential-based, educational, and personalized shopping experience.

•Deep Brand (Supplier) Relationships: Nykaa engages with brands and provides them end-to-end services, Nykaa has helped premium brands develop miniature versions of their hero SKUs to drive product trials and acquire mass-market consumers, who over time would migrate to the full-size SKUs. This has enabled Nykaa to also get exclusive brands into India. Nykaa has been successful in giving the luxury brands a platform where their aspirational status could be maintained. Shipments to consumers for such products are also packed in premium packaging to enhance the luxury shopping experience for consumers.70% of business for luxury brands comes from online channel.

•Clear Thought Through Business Model: Showing that the company is not lethargic and even if new entrants come, it will keep climbing up the ladder and stay ahead of them. A few examples are: Premium brands are focused on maintaining their premium positioning and do not wish to be listed alongside mass brands on horizontal platforms. To counter this, Nykaa has created a special Luxe platform for high-end brands and to provide a better customer experience. Also, Nykaa launched the Nyka Man app, even though more than 50% of the product would overlap, but just to focus on customer experience (75% of the customers of Nykaa Man were not shopping in the main app).

•Inventory-Based Model: Nykaa has gained trust in an era where not-so-trusted sellers on Flipkart and Amazon were cheating by selling products like duplicate Maybelline kajal. Nykaa came in, took responsibility for inventory, and became an actual online D2C beauty platform. The inventory-based model ensures authenticity. The proliferation of counterfeit products is one of the challenges in the BPC market globally.

•Exclusive Brands and Private Label: Exclusive partnerships help increase customer loyalty and stickiness, while private label helps increase margins. Nykaa’s data related to customer preferences, choices, and price points helps it to acquire and launch brands and products that can immediately achieve product-market fit. These brands now account for 11.2/12.1% of GMV in BPC/fashion respectively.

•Not into a Discounting Game: Discounts on the platform are not Nykaa-funded and are usually brand-funded, resulting in better profitability for the company. Luxury brands usually do not like discounting given the desirability around these brands, thus creating a win-win situation for Nykaa and the brand. Contribution to GMV of BPC from existing buyers has increased from 66% in FY20 to 78% in FY23, indicating trust and loyalty factor and not discounting factor. The good part of Nykaa’s journey is that it was not built on the positioning of discounts or low prices. Amidst a crowded e-commerce market, it tried to differentiate itself by: (1) strong vertical focus, (2) positioning it as a platform of premium beauty brands, and (3) robust consumer engagement, including a network of (social media) influencers.

Risks

•Heightened competition might raise customer acquisition costs. Nykaa’s competitors include various online marketplaces, retailers with physical stores, and brands adopting a direct-to-consumer approach, which effectively bypasses third-party platforms like Nykaa in the distribution and sales process. In the Fashion business competition comes from well-established players such as Myntra. (Myntra infused Rs. 42bn over FY21-22 to further its growth story; Reliance Retail has invested Rs. 118.4bn towards tech stack building for all its online platform businesses and category building)

•Launch of Tira: There will be an initial consumer churn as some customers will try Tira as well. Whether the new venture, Tira, can retain all these customers will depend on the consumer experience it provides. A situation could arise where a player like Reliance with deep pockets starts offering EMI options on beauty purchases.

•There are too many moving parts to fully understand (marketing expense, brands giving discount, fashion business etc.) making valuation uncertain.

Financials and Valuations

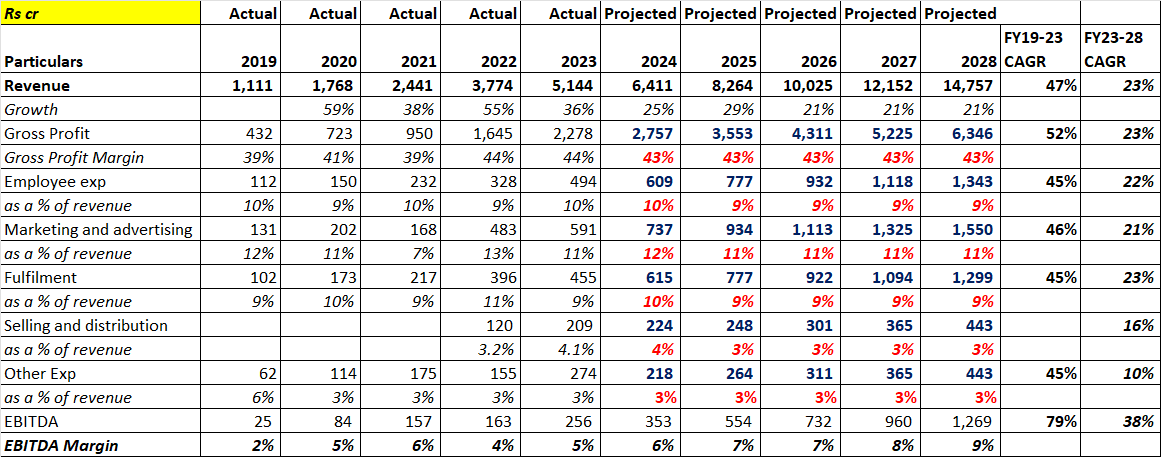

•In the past 4 years (2019-2023), Nykaa’s revenue has grown at a CAGR of 47% and EBITDA at a CAGR of 79%. According to a few assumptions that I have made (mentioned in the attached Excel), Nykaa’s revenue is expected to grow at a CAGR of 23% and EBITDA at 38% for the next five years.

•The current EV/EBITDA, based on 2024 earnings, is 125 and EV/Sales is 7. There is no similar business to Nykaa in the listed space. Businesses like HUL trade at a higher price-to-sales ratio (10.3), as their sales track record is proven, and they are cheaper in terms of EV/EBITDA (35.1), having already established their business profitability over the years. On the other hand, businesses like PB Fintech and Zomato trade at a higher EV/EBITDA (>250) compared to Nykaa. These businesses have not yet turned profitable. Markets like India have high growth, low penetration, increasing disposable income, and valuations here can’t be compared to valuations that a US-based company gets, because over there the markets have slower growth. In my opinion, Nykaa is an investible business once its dominance is proven over competitors with a few KPIs that need to be tracked regularly.

Conclusion

Nykaa has emerged as a prominent contender in India’s e-commerce industry. Through cultivating a robust online and offline presence, delivering personalized customer experiences, and offering a wide range of products, Nykaa has successfully set itself apart from competitors and established its leadership in the Indian beauty and wellness market. Beyond its business achievements, Nykaa’s triumph extends to its unwavering dedication to innovation, expanding business verticals in similar domains, and maintaining a focus on profitability.

The huge addressable and growing market in fashion and BPC segments will continue to drive revenue growth. Additionally, leveraging private labels will aid in expanding EBITDA margins. In my opinion, while marketing strategies can be replicated, discounts offered, and channels copied by competitors, certain aspects such as customer comfort with the platform, loyalty, and trust associated with Nykaa, particularly due to its non-focus on pricing alone, along with private label offerings and exclusive tie-ups, cannot be easily disrupted.

Moreover, Nykaa’s commitment to continuous growth through expanding into similar business segments adds further resilience to its competitive position.

Vineet Jain portfolio (19-03-2024)

https://x.com/VishalBhargava5/status/1769994408617820198?s=20

Any views on this? He is predicting oversupply situation in Mumbai housing market.

Lazycap’s Portfolio – Feedback (19-03-2024)

Update

Entered UPL ltd with allocation of 2% at 465 price point. I feel this one resembles Lupin at 500 bucks, similar issues of price erosion, inventory destocking, volume, high interest due to high debt & out of nifty 50 all negatives bombarded at once. Trading at 1.2 PB which is bottom valuation for the stock I guess in lifetime, could lose most of money so less allocation, one thing I am not clear is what to do if rights issue is executed in next 6 months although i feel its unlikely for them to issue at depressed price unless in pretty bad shape. Agro is bad currently anyways got it not basis fundamental outlook but basis past history and valuation point of view

Sitting with zero cash, bank has money to get me by till month end xD

Digikore Studios Ltd – a micro cap VFX play with good growth potential (19-03-2024)

Company Name: Digikore Studios Ltd (DIGIKORE)

Website: https://digikorevfx.com/

CMP: 490

MCap: 310 Cr

No. of Shareholders: 1007 (Promoters: 66.54%, FII: 2.79%, DII: 7.89%, Public: 22.79%)

About the Company: Incorporated in 2000, Digikore Studios Limited is a visual effects studio that offers a full suite of visual effects services.

Business Profile: The company offers Visual Effects (VFX) services for Films, Web Series, TV Series, Documentaries, and Commercials and has a studio in Pune.

Services: Rotoscopy, Reflection Removal, General Cleanup, Wire and Wig Removal, Muzzle Flash, Composting, Green Screen Composting, MatchMove, Driving Camps, Day to Night, CG Blood Camps, Beauty Fixes, Crowd Multiplication, Set Extension

Projects: The company made its mark in animation and VFX. It worked with projects like “Thor” – Love and Thunder, “Black Panther” – Wakanda Forever, “Glass Onion” – A Knives Out Mistery, “Deadpool”, “Star Trek”, “Jumanji”, “The Last Ship”, “Titanic”, “Ghost Rider”, etc.

Approvals: The company has approvals from major production houses like Disney/Marvel, Netflix, Amazon, Apple, Paramount, Warner Bros., Lions Gate, etc.

Matchmaking Business: The company has started a new venture known as Digikore Matchmaking, which is the world’s first Televised Matchmaking Show hosted by Bollywood Celebrity Bhagyashree

Clientelle: Digikore Studios’ clientele mainly comes from India, Australia, New Zealand, the US, and European markets.

Geographical Revenue Bifurcation:

North America – 86% in FY23 vs 42% in FY22

Europe – 11% in FY23 vs 12% in FY22

Australia & NZ – 2% in FY23 vs 0.11% in FY22

Rest of the world – 1% in FY23 vs 46.5% in FY22

Takeaways from Q2FY24 Concall and Q3FY24 Investor Presentation

If one looks at their screener page, they’d find this stock to be trading at a PE of 71. However, this is based off the FY23 Net Profit data. I confirmed this from the H1FY24 EPS of 9.85 mentioned in screener.

H1FY24 – Net Profit: 6.24, EPS: 9.85

FY23 – Net Profit: 4.37, EPS: 9.85 * (4.37/6.24) = 6.90

PE = 490/6.90 ~ 71

If I extrapolate the H1FY24 performance for FY24, the EPS would come to 9.85*2 = 19.7, giving us a current/TTM PE for FY24 of 24.87. There is most likely going to be some more growth in H2FY24 relative to H1, leading to an even lower PE, but for now let’s assume a linear projection.

This gives me an attractive valuation, given how its peers command a PE of greater than 20:

Prime Focus: 20.66 (TTM -16.90)

Basilic Fly Studios: 31.23

Phantom Digital Effects: 40.49 (TTM 29.31)

Now, let’s look into the projections given by the compny’s management. If we see the Investor Presentation PDF released in Jan 2024, on page 39, we can find the management forecasting a revenue of INR 120 crores by FY26. This would be 2.4x from current figures (again, I’m going by extrapolating H1FY24 sales).

Also, on page 8 of the concall transcript of Nov 2023, their CEO Abhishek More says that the company will target a PAT margin of 30%-35% by FY26. This means a PAT of 36 cr to 42 cr, taking the EPS between 56.83 (at 36 cr PAT) and 66.30 (at 42 cr PAT). Calculating the forward PE at current price, we get something between 8.62 to 7.39. This is mouthwatering value, and assuming no PE rating change, a price target of 1420 to 1657 at 25 PE can be expected in the next two years.

Disclosure: I am not a SEBI registered analyst. Please do not consider this post as a buy/sell recommendation. Unfortunately, since it is an SME stock, buying a tracking position in this stock is beyond my budget. However, I would have bought it if I could afford.

Redington India : Strong Performance history, re-rating candidate (19-03-2024)

Shifting business model that has become a trend mostly in the IT industry. Rather than just providing sales and support companies move towards a subscription based approach with much better support.

From my understanding of providing “As a Service” is that

- there is a fixed source of recurring revenue compared to a one time sale, although looking at the current business it might have never been a one time sale.

- They would also benefit on scalability as it is easier to adjust resources(infrastructure) to cater to the growing needs(this is often seen in cloud solution provider and other subscription based services).

- This in turn would increase the overall profits, even though (one time)sales maybe higher, in a continual service the subscription cost leads to higher profits over time(depends on the product) specially with the customer base of Redington Ltd.

There is good and bad in everything here as some downsides:

- initial investment to infrastructure to get the business model up and running(in likes of new software and customer support etc…)

- adapting to the market dynamics and customer preferences, some customers(smaller ones) may not agree to subscription based services.

Overall impact on profits is subjected to how effectively the company transitions with its execution plan.

Future concalls/investor presentations will probably highlight more on this.

Annapurna Swadisht Ltd – A Swadisht FMCG investment? (19-03-2024)

Positive development

Annapurna has accquired a 6 acre plot in Tezpur, Assam on a lease basis for a greenfield manufacturing facility to expand its footprint in the North-East market.

https://nsearchives.nseindia.com/corporate/ANNAPURNA_19032024142232_Intimation_SE_PR_ASL.pdf

Mankind Pharma – Next Big Pharma Player? (19-03-2024)

Insightful and Interesting podcast w/ the MD of Mankind – Rajeev Juneja.

I liked the humble nature of Mr. Rajeev and the pedigree of experience (~30 years) he comes with. Right from personally visiting small villages to sell his products to now managing a company with 22,000 employees, his journey is very inspiration.

Yet to read more about the company. Disclosure – Not invested.

Truth of Pharma Industry, Medicine, Condom Sales explained by Mankind’s Founder Rajeev Juneja | TRSH

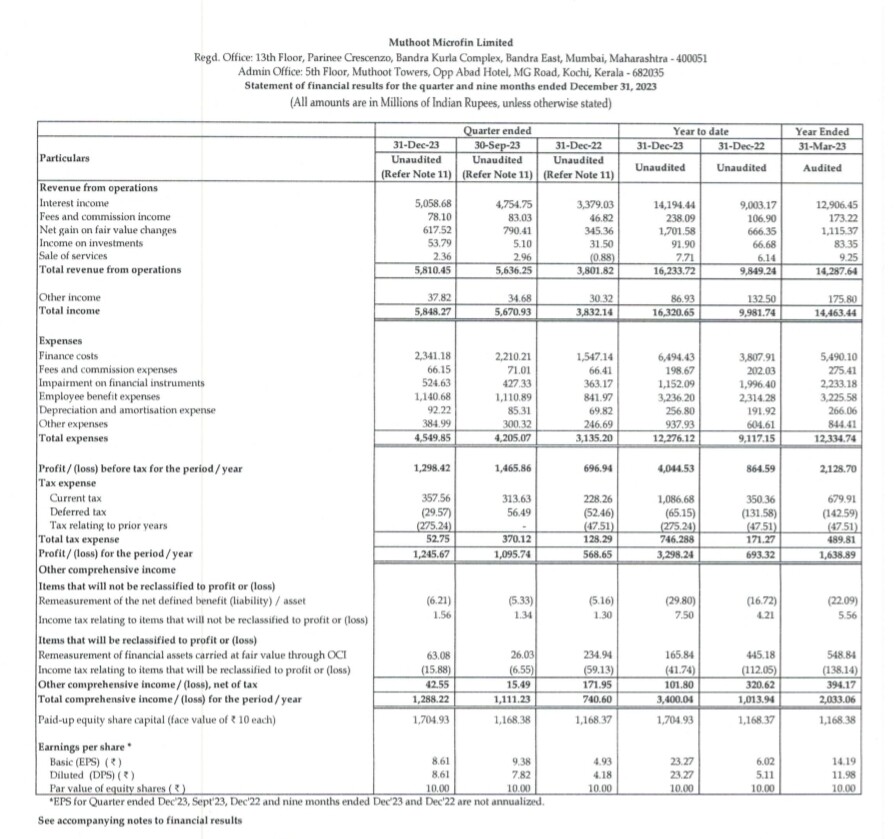

Muthoot Microfin Limited is it next JP Morgan? (19-03-2024)

Net profit is one of the important indicators to show the financial health of the company. Net profit of Muthoot Microfin is Rs 163.89 Cr and the compounded growth of profit in the past 3 years is 108.02 %. The PAT margin of Muthoot Microfin is 11.47 %.