Investor presentation by Vindhya Telelinks after a long time. Pending order book of more than 7000 crores as on date.

Posts in category Value Pickr

Yes bank (27-10-2024)

Summary of Yes Bank Q2 FY25 Investor Concall Highlights:

- Record Profit Growth: Yes Bank posted a significant quarterly profit of ₹553 crore in Q2 FY25, marking a 146% year-on-year increase and 10% growth from the previous quarter, driven by a strong operating profit and 14% increase in net interest income.

- Improved CASA Ratio: The bank’s CASA (Current Account Savings Account) ratio reached 32%, reflecting an increase in low-cost deposits that contribute to stable net interest margins and reduced funding costs.

- Strategic Focus on Retail Growth: Yes Bank is carefully expanding its retail assets, balancing profitability with risk management, particularly due to industry-wide challenges in unsecured retail lending.

- Enhanced Asset Quality: Asset quality improved with a gross NPA (Non-Performing Assets) ratio decrease to 1.6% from 1.7% in the previous quarter, and a provision coverage ratio of 70%.

- Commitment to Shareholders: Management reassured investors regarding share price performance and dividend policy, emphasizing their goal of consistent financial performance and optimized returns for stakeholders.

- Managing Margin Pressures: Despite potential pressure from moderating interest rates, the bank expects stable margins due to well-matched assets and liabilities and plans to reduce SLR (Statutory Liquidity Ratio) and RFR (Risk-Free Rate) security holdings, which have impacted margins.

- Improved Credit Practices: Yes Bank is enhancing asset quality in unsecured retail lending through stricter underwriting standards and improved collection processes.

- CASA Growth Strategy: The robust CASA growth is attributed to a focused strategy on service quality, customer engagement, and expanding branch networks.

Overall: Yes Bank’s investor call highlighted strong Q2 results, a proactive approach to industry challenges, and dedication to sustainable growth and profitability.

Sree Rayalaseema Hi-Strength Hypo Ltd (27-10-2024)

Any update on the industrial Sodium metal production and the water-treatment specialty chemicals project the company was looking to enter into?

Is the EC received?

And if anyone can share the capacity details, will be very helpful.

IDFC First Bank Limited (27-10-2024)

Hope you permit me to disagree. After the merger was announced, Capital First continued to post stunning results till the last day. I.e. q4 18, q1 19, and q2 19, exactly in line with trends of five years of Capital First ( always stunning results after first 4 years of capital first 2010 to 2014 when they used to post bad results (loss after loss after loss)

Meanwhile idfcb posted horror results in each of these 3 quarters, in fact in sep 30 2018 results they sold a lot of bad loans to ARC.

So it is clear to me IDFCB dragged the stock down.

Those days Dewan went down ( sep 18) and isfc collapsed with it (simultaneously).

I was invested those days and he got many brickbats from all exactly the way he is getting now. I was a junior kid those days even i ranted. After 2015 suddenly he became God when results were good, you shouldnhave seen seasoned investors just adoring him.

Imho he truly inherited the bank at that price of 37.6, good results of capf could not lift a idfcfb stock, because idfc was the acquiring entity and was the larger entity with some 3x market cap of cfl

Btw their infra exposure alone was morenthan the networth! Wonder what all idfcb shareholders were smoking holding the stock, with 10 pc retail deposits 23% corporate deposits 33% certificate of deposits and ~ 34% odd in bonds.

I was an investor in capf so i have the full history studied them went to their branches etc.

Overall i believe (because i am supporting his positon when the popular mood is against him dont beat me up pls). I have been enuf against him in 2019 2020 2021 22 etc. See old posts…

Now after seeing the extent of his work am atleast an admirer of his work. I went to the cynergy branch and friended the staff and the admiration of the staff about his motivation, direction, systems focus, etc was something i was impressed with. (Apparently he cones there v often)

Am a user of their products and happy customer and also biased in that sense.

Have never seen anyone bashed up so much after fixing the bank. I am only hoping he can stand and fight his way out and not chicken. And repeat capf get bashed first and then deliver and be respected.

Btw i think he made a mistake marrying this bank. He could have gone and got a license and make cap first bank. Lige would have been better rsther than solving MEP and cox and kings and dewan and r capital and vodafone and 100 such names.

Holmarc Opto-Mechatronics – R&D play (27-10-2024)

Thx for the excellent analysis @bm and didn’t felt it as long as you have beautifully focused it on management, and quality of their reporting. While reading through the report and AR one thing i thought of is ‘Do they have any IP rights or not? Or do they have any collaborations with others to use any IP rights/license? Couldn’t trace any from last 2 AR’s, except for some Device trademark, and Word Trademark, both issued in 2021 and 2022. I do not have much clue about the industry they operate, and given the size of the co., not sure they must be working towards those and filing for it??

Adding few other bit of findings that could be worth highlighting. The tax case mostly a negligible item, but keeping it only for reference.

1. The company had a property tax case against Kalamassery Municipality. It was initially quashed by the high court, however the municipality went ahead and filed an appeal against the judgement. The case is still pending as per AR (May, 2024). Not sure, how much of a financial impact it may have (if goes against the co.) though its most likely not a possibility.

Incerpts from the indiakannon site.

The case involves a dispute over the levying of property tax on Holmarc Opto Mechatronics by the Kalamassery Municipality. The company contested the property tax assessment order and demand notice issued by the municipality. The dispute centers on whether Holmarc’s industrial unit within an industrial estate is exempt from property tax.

2. While going through directors list and associated companies, I noticed few relations with “Greentreat Machines Private Limited” and Holmarc Opto-Mechatronics Limited. Not sure, if the company is still active, and having any business. The following is what i could trace from the Annual report.

Past Associate Company: Holmarc’s annual report for FY2023-24 mentions that Greentreat Machines Private Limited was an associate company of Holmarc until March 15, 20211. An associate company is typically an entity in which another company has a significant influence but not control, often through a minority ownership stake.

50% Shareholding: Holmarc held a 50% shareholding in Greentreat Machines Private Limited until that date.

Promoter Disassociation: Jolly Cyriac, Holmarc’s promoter, resigned from Greentreat Machines Private Limited on March 16, 2023. Likely the formal disassociation between Holmarc and Greentreat Machines Private Limited.

Based on the above, Greentreat Machines Private Limited was previously closely related to Holmarc through a significant ownership stake and likely operational influence. However, this association ended in 2021 and was further solidified by Jolly Cyriac’s resignation from Greentreat Machines Private Limited in 2023.

While digging further some websites showed current MD of Greentreat Machines is one Mr.Joy George Menachery, and Additional director Eby Manakkatu cherian and i couldnt trace them back to Holmarc’s KMP’s.

Edit: Greentreat mach., Co., status is active as per MCA site.

Disclosure: Not invested. Post purely for study purposes. thanks.

Vadilal Ice Cream (27-10-2024)

Hi @hakim_yamin

Could you elaborate on the hoardings part? Photos, location, etc??

The stock performance has been frustrating. Looking for reason to not sell at such valuations!!

EFC – Entrepreneurial Facilitation Centre (27-10-2024)

EFC(I) Limited Q2FY25 Concall Summary:

Financial Performance:

- Consolidated revenue reached INR 171.08 crore, revenue grew by 63% in Q2 FY25 and 77% in H1 FY25 YoY.

- H1 FY25: Consolidated revenue reached INR 276.36 crore, EBITDA around INR 133.59 crore, and PAT of INR 52.33 crore.

- Consolidated net profit jumped by 131% in Q2 FY25 and 267% in H1 FY25 YoY.

- Consolidated EBITDA of around INR 84 crore, and PAT of INR 36.56 crore.

- Cash flow from operations stood at INR 150 crores for H1FY25, 4x from H1FY24.

- EPS for Q2FY25 is 7.34 not 14.69 which management reported in their exchange filing.

Operational Performance:

- Rental Segment: Generated approximately INR 89.2 crore in revenue, constituting 54% of total revenue.

- Design and Build (D&B) Segment: Contributed INR 77.24 crore, amounting to 46% of total revenue. Secured an order book exceeding INR 70 crore, including a large contract with TCS worthover Rs.18 crore.

- Rental Business: Operates on a ~30% EBITDA margin at the center level and ~25% at the corporate level.

- D&B: EBITDA margin averages 17-18%, with potential for higher margins (24-25%) on projects with higher complexity.

- In the Design and Build Segment total team size of 40 peoples, includes your architects that includes your designers and also includes your sales teams part of it.

- Furniture Manufacturing: Successfully completed the first order after commercial production commenced in September 2024. The order book looks promising, with a revenue target of INR 60-75 crore for the fiscal year.

- Managed Office Business: Increased leasehold area by ~125,000 sq. ft., adding 3,600 seats across four existing city centers.

- Total Footprint: 61 operational sites across eight Indian cities, covering 2.4 million sq ft, with a total seat capacity exceeding 50,000.

- Furniture business started its production on 28th September so actual number will flow from Q3 onwards.

- Rental Business: Receivable cycle is generally less than 30 days.

- Design and Build: Receivable cycle averages around 90 days, due to the project-based nature of the business.

- Furniture Manufacturing: Receivable cycle is expected to be between 60-90 days, with a focus on institutional clients.

- Management plans to share a detailed breakdown of receivables by segment in future financial updates.

- Management is committed to expand their seat capacity to 65,000 – 70,000 by end of this FY.

- Total Billed seats are 42183, up by 9% QoQ.

Key Takeaway from Concall:

- Usually Q1 has lower margin as compared to other 3 quarters, as seats are under development and discussion with landlords usually takes place in Q1. So once the seats get occupied and billing starts the benefits start from coming quarters. This cycle goes for every quarter but usually happens in Q1.

- Design and Build Division has higher receivables as it takes time from the day order is received and design build and approved. Also clients took some amount of money as retention money, typically what happens in EPC business. Roughly receivable periods go from 0 to 180 days.

- Since management is focusing on contract value of more than 25,000 square feet where organised clients are more, that’s why cash flow is in a better position than earlier.

- “All the assets that will be acquired that the SMREIT they will be independent and they will not be having any direct link to the assets that our company owns” EFCIL will book only the management fees under REIT business.

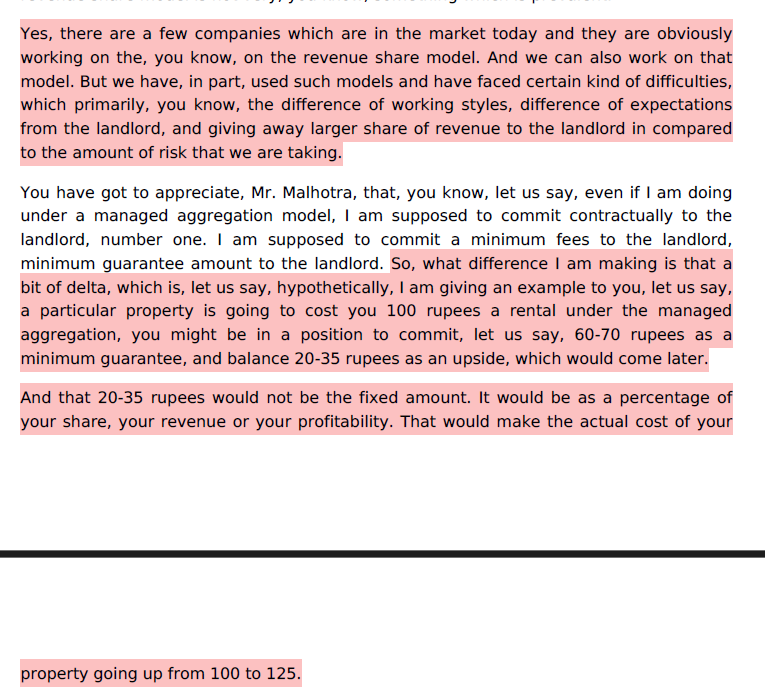

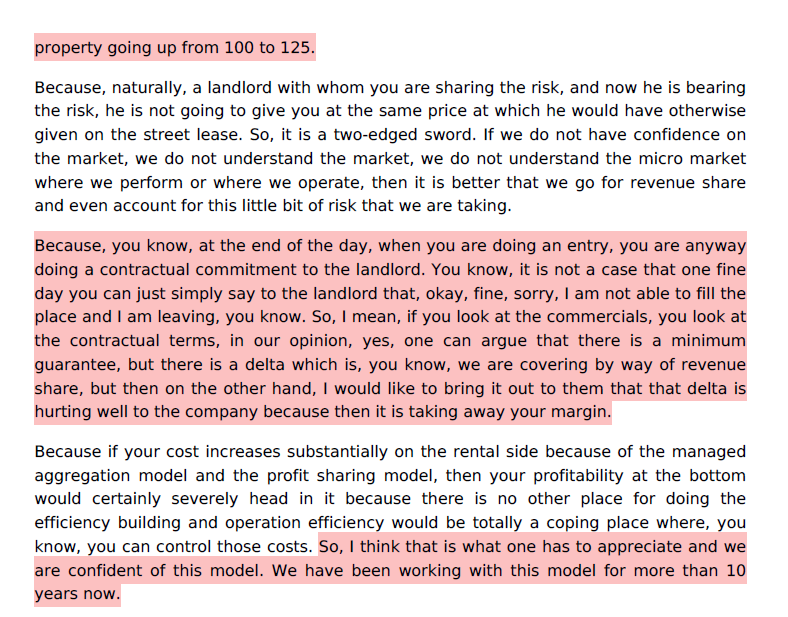

- One question is raised on the fixed rental and managed aggregation model; for which I’m attaching concall snippet as management has explained in a very simple way.

- Management is right on their part because if we see mgmt is providing fixed income to landlord, though downside is protected, mgmt is also not sharing revenue% with landlord, which can also impact margin in the future because everyone knows that COWORKING will exist here taking 5-10 years time frame, so why not go with some other model? And everyone is also aware of the WeWork scene so no one will commit the same mistake in the future.

- Going forward you can certainly at least expect a full revenue for 50,000 seats and obviously partial revenue for the new 15,000 to 20,000 seats which are going to be operational ahead.

- Management expects to maintain an annualized EBITDA margin around 30% at the center level and 25% at the corporate level. PAT margin of around 15-16%.

- In this year furniture will contribute not more than 15%, however in future the company will keep equal revenue for all the three divisions 33% each.

- Average rate per seats still remains around INR 6250 but with the new seats getting added more and more and they are getting sold at a higher rate of INR 6500 upwards as it is already evidenced by companies entering into larger office spaces.

Management on larger space; There are obviously benefits. In acquiring the larger space is the economy of scale that we are able to achieve. We are yes acquiring or rather acquiring these old rights over the larger area.

- Again a question is raised on competition in the industry, in which management admitted that competition will remain as always which exists in every industry but presence of PAN India players is still not visible in this space, regional players are more in this space.

- One very interesting question which was on valuation of INR 545 crore for whitehill, I know it’s a very absurd valuation and the fact the merchant banker and Registered valuer has already furnished the report so there is no question to be asked now. Why am I saying this? I’m doing my CA articleship in valuation domain and I know how we arrive at the final value, all the inputs are furnished by management and they provide the final value to be arrived at and it too depends on the future estimates of the management. There is no point to escalate this point further.

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (27-10-2024)

The management was clear when they mentioned that they will announce capex when they have future orders in hand, hence they are waiting for two months before they announce. The cautious approach is in fact a very comforting for an investor that the management will take very calculated call on capex.

As an optimistic investor, I feel that the AI boom and manufacturing power that the country is striving to become, putting up power generation capacity is an inescapable requirement.

Cautious investors must wait for the capex announcement as valuations are rich.

Rossell India Ltd (27-10-2024)

Not reflecting yet.

Can anyone comment on the future prospects of Rossell India post demerger