Education has seasonality, Revenues depend upon admission season.

Posts in category Value Pickr

Kitex Garments Limited (24-11-2024)

It was another one

What I meant by reading their few of the last activities these things may happen

- Major one was merger of kitex garments and kitex children’s

- Bonus issue

I don’t see much impact for second one

Even though few people especially retail will buy small value shares.

Bonus issue may create more number of shares in the market.

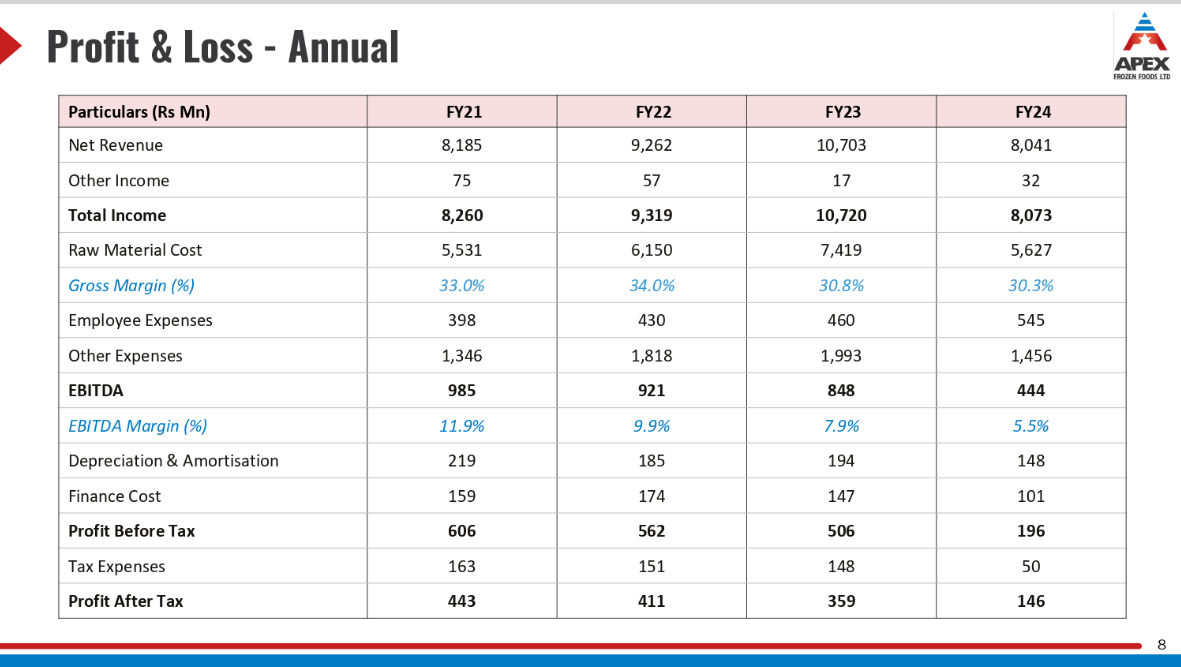

Apex Frozen Foods (24-11-2024)

Why do you think so ? Compared to feeds, shrimp processing looks to be small. But its better than Apex frozen foods both revenue wise and margins perspective. Margins have remained stable around 14% in the last 6 years, where as Apex’s margins have degraded from 11% to 5.5%

Both the companies have more or less same shrimp processing capacity.

Avanti – 36K MTPA (out of this 7K MTPA commissioned in Mar24)

Apex – 34K MTPA

After how many days a stock comes out of periodic call auction? (Esm2 to esm 1) (24-11-2024)

After how many days a stock comes out of periodic call auction? (Esm2 to esm 1), and where could I get the recent list and how set the alerts for the same. Please guide me on this, thank you in anticipation.

HDFC Life Insurance Company (24-11-2024)

HDFC Life MD said that, though this move by IRDA looks good to enhance the reach of Health Insurance in India, but she sounded cautious as HDFC Life may not immediately go for such products.

She mentioned that, there are disruptions happening in Life Insurance domain as well and their first priority is to enhance their coverage in this domain.

I do not recollect all points, so I will say they might look at Health Insurance products but may be with next priority.

Microcap momentum portfolio (24-11-2024)

INOXGREEN should not be on the list as the price in constant in your reference sheet. @visuarchie sir.

below is the list I got

- STAR

- GRWRHITECH

- WOCKPHARMA

- CHOICEIN

- PGEL

- SUPRIYA

- NEULANDLAB

- TIPSMUSIC

- WABAG

- SHILPAMED

- NAVA

- PRUDENT

- ZENTEC

- GANESHHOUC

- VMART

- OPTIEMUS

- SANSERA

- AMIORG

- MARKSANS

- KIRLPNU

- ORCHPHARMA

- AVALON

- KESORAMIND

- BANCOINDIA

- IIFLSEC

The Anti-Portfolio (24-11-2024)

To be explicitly clear, my comment was to highlight sheer admiration for overcoming endowment or Loss Aversion bias. Not otherwise. Thx.

The Anti-Portfolio (24-11-2024)

Decision of long term and short terms are based in recent triggers, nothing is black & white in stock market, especially in bull markets crooks promoters play with balance sheet hence for small cap and mid cap companies untill there are very strong reasons based on valuations and cash flows, selling and protecting capital is best decision. Long term hold can become a hard sell based on change in industry dynamics hence nothing wrong. This is not the time for long term hold, your friend might have become a “forced long term” than long term. I had invested in Kalyan Jeweller in Nov 22 at average 110 levels, as oer management guidance my estimations were for a market cap of 80000-100000 cr in FY 26. Market euphoria has given market cap of 70000 cr in 2024 with rich valuation of 115 PE, so what should i do, should i hold for two more years for time correction? Never, i have exited my all holdings 700 average levels. A long term bet of 5 years sold in 2 years flat. Sarcasm for others strategy is not a good.

Srivari Spices and Foods Limited (24-11-2024)

As mentioned above, it is due to right issues and promoter has not participated in the same nor they have sold any share. So promoter shareholding has decrease by 20%.

Himatsingka Seide (24-11-2024)

KEY NOTES FEOM Q2 FY 2025 CONCALL

### Business Update:

- Q2 FY ’25 total income decreased by 6.4% due to a recalibration of the brand portfolio.

Capacity utilization reported as follows:

- Spinning division: 99%

- Sheeting division: 61%

- Terry Towel division: 67%

- The recalibration process is expected to impact operations for another 4 to 6 months.

### Strategic Initiatives:

- The company is reassessing its brand portfolio to balance value proposition against revenue and costs.

- Aim to add new clients and explore new markets as part of the recalibration strategy.

### Domestic Market Performance:

- Significant improvements in revenue from India during the first half of FY ’25 compared to the same period last year.

- Targeting to grow India’s market to approximately ₹1,000 crores over the next 5 years.

- Currently operating with three brands in India: Himeya, Liv, and Atmosphere, across multiple product segments including bedding, bath, drapery, and upholstery.

- Distribution presence expanded to over 460 cities with more than 3,000 points of sale.

### Financial Developments:

- Successfully completed a ₹400 crores Qualified Institutional Placement (QIP), with proceeds primarily aimed at repaying term debt, which will significantly reduce net debt.

- Net debt as of September 30, 2024, was ₹2,679 crores, marginally up from ₹2,671 crores at the end of June.

- Operating cash flow has averaged approximately ₹300 crores over the last few years.

### Margin Guidance:

- Current EBITDA margins are hovering around 20%, with management indicating they can fluctuate between 18% and 22% due to product mix and inflationary pressures.

- Management remains optimistic about maintaining margins despite cost pressures from container costs and high cotton prices.

### Export and Textile Demand:

- Outlook for exports remains buoyant, with ongoing efforts to enhance market share.

- The management anticipates increased interest from U.S. retailers due to shifting sourcing strategies (China Plus One) and geopolitical factors.

- Other jurisdictions (EU, UK, Middle East, India) are also expected to contribute significantly to growth.

### Challenges and Headwinds:

- The recalibration of the brand portfolio is causing short-term revenue impacts, particularly in the Sheeting division.

- Management acknowledges that some revenue streams may be subdued in the near term due to this strategic repositioning.

### Future Outlook:

- Management expects to achieve a revenue run rate of ₹4,000 crores at full capacity within the next 18 to 24 months.

- The domestic business is projected to grow to ₹300 crores to ₹400 crores over the next two years, aligning with overall EBITDA margins.

### Brand Portfolio Insights:

- Approximately 30% of revenue currently comes from branded products, down from around 40-50% two years ago.

- The company is actively working to optimize its brand portfolio, focusing on brands that provide a viable value proposition.

### Working Capital Management:

- The company is addressing increased debtor days, cash conversion cycle, and inventory days, with an aim to improve working capital cycles by the end of FY ’25.