This was a hypothetical question. I don’t like Debt ETFs for reasons mentioned above.

I don’t want to be on mercy of fund house. When I invest in debt instrument as a small investor, I want it to be legally binding on fund house to redeem at NAV and credit my account next day. I used debt MFs regularly.

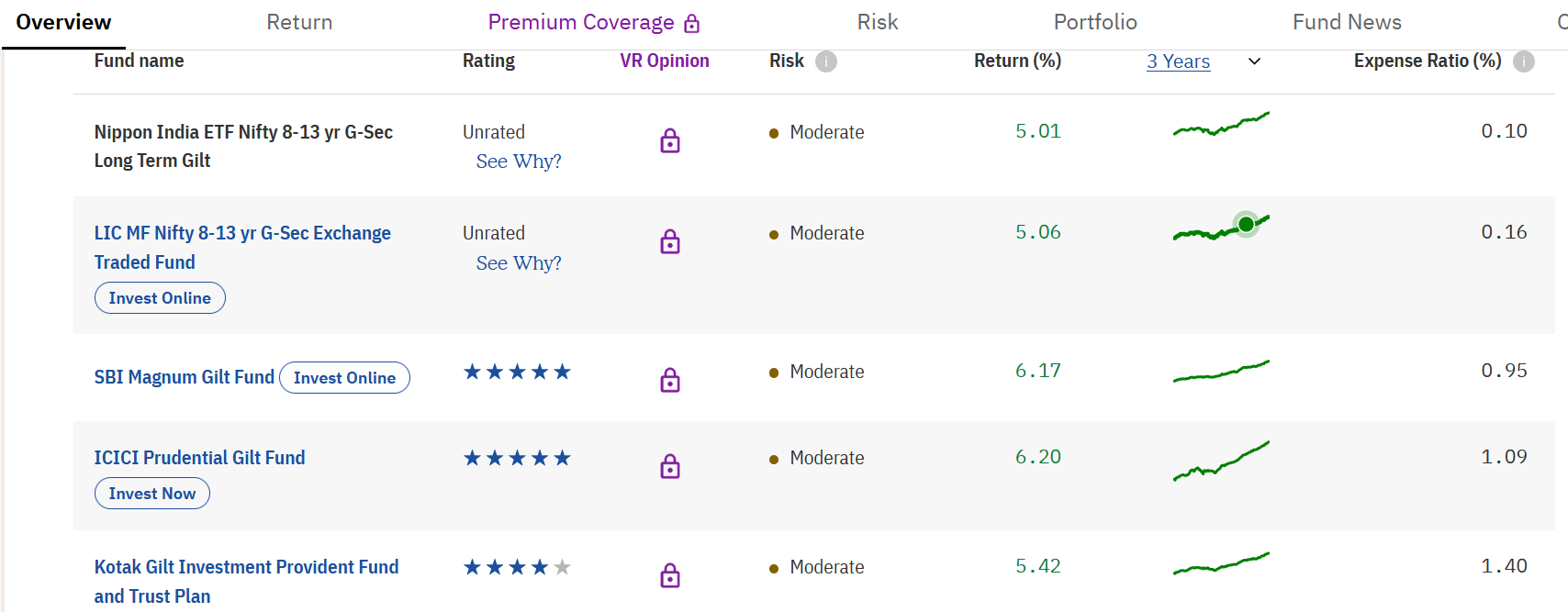

Also, why should one invest in these ETFs as returns are also lower that actively managed funds despite much higher expense ratios.

This comparison is for regular active plans. Direct plans funds expenses are much lower and therefore out performance will be much higher.