Hey – I have dropped the decision of getting a SEBI RA certification. I had enrolled into the ignou course as suggested by @Ferrari1976 and have got the books, if anyone needs the books kindly reach out to me

Posts in category Value Pickr

South Indian Bank (06-03-2024)

The South Indian Bank RE will show up in your demat which you can sell. RE is rights entitlement. If you sell RE it means you’re selling your rights to buy shares at lower price to someone else.

Raymond – The Complete Man (06-03-2024)

Now that the shareholders meeting is concluded in favor of creating two separate companies, when do we expect the process to start and we get shares of the new company?

Zaggle Prepaid Ocean Services (06-03-2024)

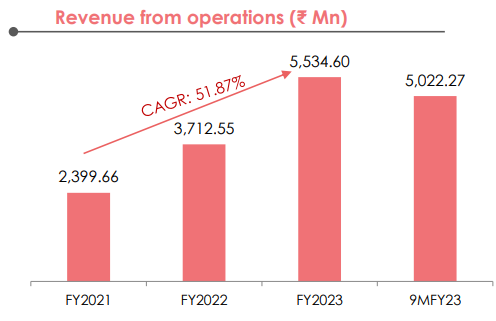

Starting this thread on Zaggle Prepaid Ocean Services which had its IPO in Sep 23.

A combination of SAAS and Fintech domains. The company provides following three products:

- Propel : Suppose you won ‘Star of the year’ award at your company, You will get the reimbursement voucher on your Zaggle Propel console/card.

–Save : Suppose you had to travel as part of company work. The Zaggle card gets loaded with estimated expense for travel, stay, food etc. At the end of it you can upload your bill, your manager approves it and the loop gets closed. Hence ease of expense management for employee as well as the company.

–Zoyer: Suppose you have a vendor, You can keep transferring the sum to him on his Zaggle card, He can reimburse it subsequently.

They are also very active in Prepaid card market. That is suppose you have a fleet of trucks. You can keep loading your driver’s cards on daily or requirement basis for fuel, meal etc. Hence efficient expense management again.

I see a lot of need for a product like this. There are few competitors as well. Example

-Expensify

-Happay

-Zoho expense

SAP concur

However no listed player in India. World over there are 4-5 multinational players.

As the business model sounds it is very important to have good partnership with prominent banks.

Their bank partners include Axis bank, Kotak Mahindra, Yes B ank, IndusInd to name a few.

-Also have recent collaboration with VISA, Razorpay.

-Current customers include TATA Steel, Torrent Gas, Greenply, INOX, DBS, Rajiv Goenka group and many other big corporates.

Finances

-51% CAGR revenue growth over past 3 years. Guidance of 40 – 50% growth in coming years.

-50 % CAGR EBITDA growth with margin guidance of 12 – 13 % in near future.

Cons

- Increased receivables (Inherent to business, because generally employees upload their bills in a cycle of 45-60 days)

Hence increased working capital days

-High PE (137) however as earnings increase, this will start to go down. - Company adopted IND AS accounting which has led to increased revenue from propel. As per them this is to cater for increased take rates from voucher based redemption rather than points based, could be aggresive revenue recognition.

Overall I feel the company has potential to become a multi bagger if they keep a check on receivables and working capital

-Ashish Kacholia invested in this in Q2 FY 24 then increased stake in next quarter. So there is interest from bigger investors.

Lets see what this does. It is definitely one to watch.

DISCLAIMER : Invested, Not a buy or Sell recommendation

Vindhya Telelinks ltd (06-03-2024)

What could be the justification for this stock:

- To be still trading at less than Book value,

At les than 10 annualized PE, when small cap index is at all time high, when junk shares are trading at 10x BV, and 40 PE.

Their reserves are more than their total market cap.

Is it a deep value stock available.

Or perhaps market knows something more , which doesn’t meet the eye.

Could their be possibility of crooked BS & P&L.

Amit Singh Learning page (06-03-2024)

TATA Sons listing and the beneficiaries:

In September 2022, the Reserve Bank of India (RBI) classified Tata Sons as an “upper-layer” non-banking financial company. The category, among other requirements, mandates that such firms seek a public listing within a period of three years.

Understanding NBFC layers as per RBI classification; these layers are based on Size, Activity, Perceived Risk;

• Base Layer- NBFC less than Rs. 1000 Cr

• Middle Layer- NBFC more than Rs. 1000 Cr

• Upper Layer- NBFC identified by RBI as warranting enhanced regulatory requirement based. Value is no bar and at any time top 10 NBFC will be in this Layer.

• Top Layer- It ideally remains empty, if RBI sees substantial increase in the potential systemic risk in a NBFC it moves to this layer from Upper Layer.

https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=12179&Mode=0

TATA Sons listed investment is at Rs. 16 lakh Cr. The expected listing is to be on ~50% discount at 8 lakh Cr. (Open Source info)

Here thing to note is that TATA Sons share held by company are;

• TATA Trusts- 66%

• TATA Motors- 3%

• TATA Chemicals- 3%

• IHCL- 1%

• SP- 18.4%

• Others- 8.6%

| TATA Sons Holding Company | % Holding | Rs. Cr as Financial Asset if listed at 8 Lakh Cr valuation | Market Cap (Rs. Cr) | Yearly Sales (Rs. Cr) | PAT (Rs. Cr) | PAT Margin | CMPS | P/E | Post Listing share price | No of shares (Cr) |

|---|---|---|---|---|---|---|---|---|---|---|

| TATA Trusts | 66% | 5,28,000 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| TATA Motors | 3% | 24,000 | 372533 | 423874 | 20149 | 4.75% | ₹ 1,018 | 19.5 | 1800.00 | 383 |

| TATA Chemical | 3% | 24,000 | 30000 | 16353 | 1770 | 11% | ₹ 1,178 | 17 | 7000-11000 | 25.5 |

| IHCL | 1% | 8,000 | 81733 | 6489 | 1170 | 18% | ₹ 574 | 70 | 2000 | 142 |

Now this information is with the market since 2022 but the price of shares have not moved.

With the proceed the companies can pay off their debts and can go for expansion.

TAMO has 1.28 Lakh Cr debt and TATA Chem has 6000 Cr Debt.

Question is why?

Disc: Not invested in any of TATA Group entity.

VP Bhubaneswar/Odisha Meetups (06-03-2024)

Hi Sir

Am interested in joining/ attending the meet organized.

Have worked in Jajpur and Bhubaneswar for 8 years.

In markets from last 3 years. And learning by the day.

Waaree Renewables – old Sangam Advisors – can it keep on renewing? (06-03-2024)

Their 3rd and 4th quarters are always better in margins. So, can expect somewhere around 180-200Cr PAT this year from execution of 1GW. With 2.5GW order in hand, the earnigs can quickly catch its valuation.

Vineet Jain portfolio (06-03-2024)

Hi @Vineetjain111 , what do you think of Geekay Wires at this juncture ? Top link growth has almost stagnated with margins falling down q-o-q. Yearly margins looks like they’ve peaked.

Do you find the valuation comfort to hold this ?