What worries me the most about Fredun is the lack of operating cash flow!

Do we have any insights on why are the cash flows so dried up and when do the trade receivables hit the balance sheet? I also saw the inventory days is >200, any thoughts on this? Seems odd compared to other pharma companies.

Posts in category Value Pickr

Fredun Pharmaceuticals – A good microcap with great potential? (26-10-2024)

Dhruv’s Portfolio: Comments Appriciated (26-10-2024)

It is still a financial heavy portfolio within equity. Not sure why are so much inclined to investing into this sector leaving out tailwind sectors. It is time to slowly deploying the cash into these tailwind sectors as the market is playing out exactly what I said on March 13.

Also you can look at having some exposure to long tenure bonds for portfolio stability and steady stream of income. IMO the current yields are expected to further drop post RBI rate cut action.

Take informed decisions.

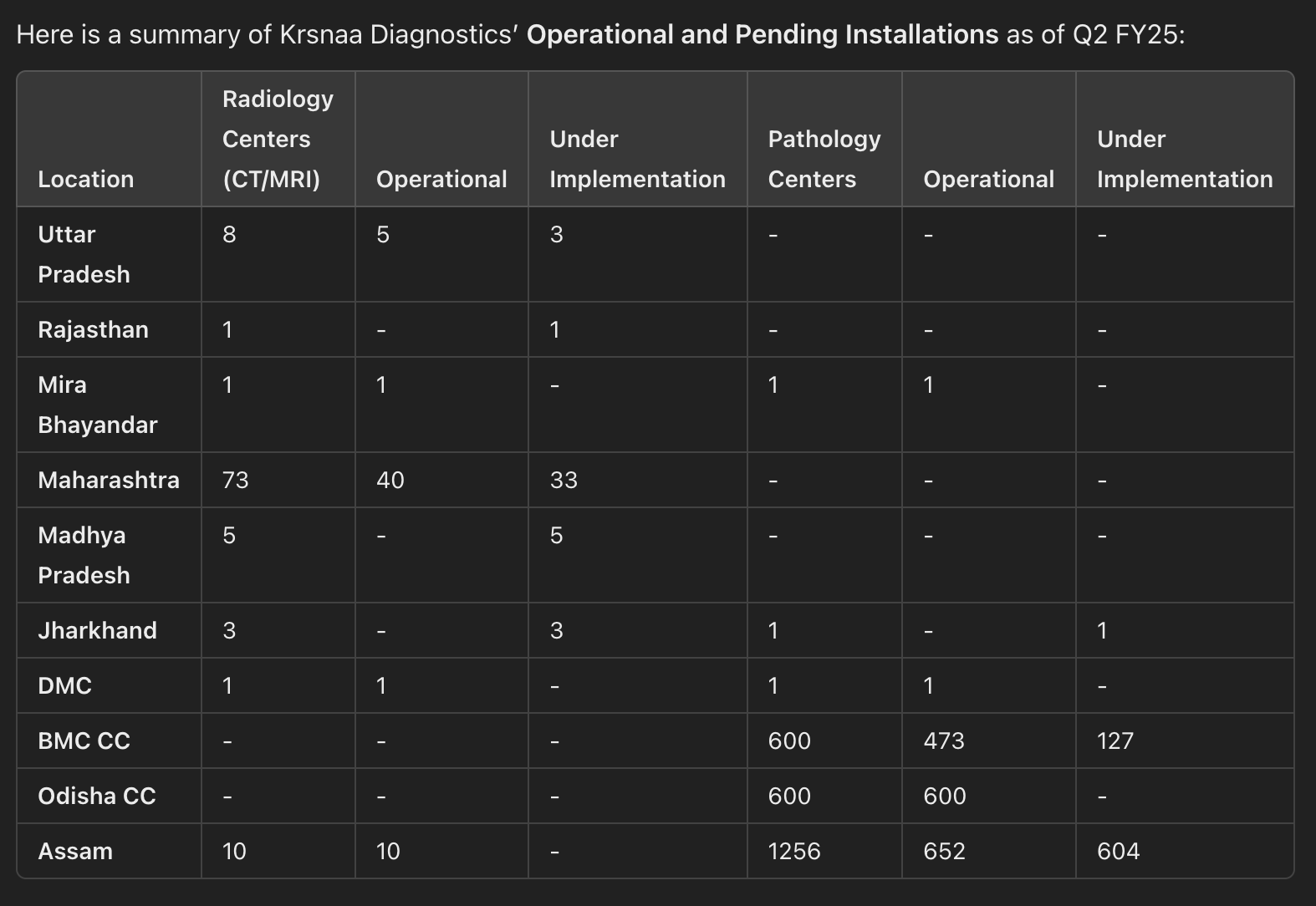

Krsnaa Diagnostics – what is the diagnosis? (26-10-2024)

Punjab is missing from the list !

Krsnaa Diagnostics – what is the diagnosis? (26-10-2024)

Krsnaa Diagnostics currently has a strong operational footprint, with 92 centers fully operational and an additional 45 under implementation, focusing heavily on CT and MRI installations across multiple states. Their strategy includes expanding diagnostic services and enhancing revenue through partnerships and state contracts

Northern Arc – Long term play (26-10-2024)

I am starting to like this company at 1.7 times book. If anyone has any further insight on management and loan book quality please share.

Poor guys small portfolio (26-10-2024)

HDFC bank Hold

Kotak bank if you have very convinction then hold or convert to. good company

Switch to ICICI BANK OR other small cap

Sell Motilal Oswal and re allocate the capital

Reason : my dad had myself had invested in 2.5 L in portfolio investing of Motilal Oswal

It gave Good returns 26%in 1.5 years

But Relationship manager does not closes the Account as my dad needed urgent for buying property

They just Give lectures and was not providing services only

I was fed up ,

Shocking Part there is no Proper structure for customers care call , it diverts and no physical person is available only to handle issue

I had to email to CEO , And all high hireachy people multiple times

Local RM does not how to do profit booking

Customer has not right to do profit booking

Worst Experience

I got the money that too through email update about processw when they are doing activities

No RM or sineor hierarchy contacts on ur email or personal number

They just tell you have not right to email ceo and gave normal email but my mail ceo escalation gave pressure

I also respect Ramdeo Agarwaal but no way I am going invest my money in business where customers are having nightmare after sales

Follow Ramdev Agarwal for value investing lessons but not to invest Motilal oswal

Rest is your choice

P.S many celebrities / may dumb HNI may be giving Motilal oswal for investing

But they are acting to do value investing but not doing it

Just Indian market is kind so they are making money buying selling in large stocks

They never hold for long term like we value investor do

Mankind Pharma Hold

But get it due diligence and future aspects for pharma guy or senior investor

I am not right person to advise on pharma

Nesco

U can check Valuepicker post

It is showing some red flags

My advice would be sell

Restaurant brand Asia sell

Kind of investment you have chosen it is way risky

I also liked Rishabh instruments

After ipo it was near 52 week lows / good buy zone

But this kind of business will eat up your years of investment and provide not returns

It’s odd are such that

With High Capital you can keep small tracking positions

But not in small portfolio concentrated position

You can keep doing arguments but odds is not good for your portfolio

Same goes for radiant ,

Taraon I have kept 1 share for tracking

From 2 years it is not performing

Kindly accept and keep it as loss or book loss

Your choice

HDFC life 5 years 15% returns

Regular portfolio targets 26% per year returns as rule of 72

Concentrated portfolio expectations are high

I will suggest not to keep even small tracking positions

Smarts investors will simply understand by 5 returns

I know IRDAI has brought many new rules which can be give turnaround

But don’t expect multibagger resturns

Rather change positions to get good returns

I had also done same mistakes as new investor

I myself started as new demat Account

Learned from Valuepicker

And new portfolio 90% stocks are in profit

It doesn’t affect your investing and returns calculations

Simple maths

Mixing up will get you yours efforts good but calculation and u will not see proper results even after doing good

As you are seeing mix results

This portfolio is your choice what to do or not to do

But please start with new zerodha

U have the edge

But edge + studying business in Valuepicker = results

90% success ratio was showing my personal study is not wrong but picks should be good

IDFC First Bank Limited (26-10-2024)

The management deserves every bit of it and more…the gentleman was kind and well behaved imo,

Management gave zero indication of what is coming in MFI during Q1 concall and subsequent media interaction…in fact vaidyanathan tried to give an impression that provisions will be slightly less in Q2 at that time…

.

until now management used to conveniently blame everything on legacy issues and ‘start-up bank’.

this time underwriting is their own…so ‘pristine quality’ of their loan book got exposed.

.

also someone should advice them to stop printing that history of capital first and merger story BS in investor presentations and Annual Reports…its been 6 long years…

ITC: “Will”(s) “Gold Flake” assist “Ashirwad” to win “Bingo!”? (26-10-2024)

Let me try to put my question differently…rather than what one would do with their ITC hotel demerged stocks, what must be ideal market cap of ITC hotels as on today, with Indian Hotels trading at a mcap of almost 1 lac crore and PE of approx 76? Is this valuation of Indian hotels sustainable ? If the hotel industry is all about deep cycle related to capital intensive nature, the trajectory of the sector should not work in unison but rather depend in individual companys capex…however something unique happened last few years after covid and we saw this sector also move in unison…is this sustainable change?

IDFC First Bank Limited (26-10-2024)

I respectfully disagree with this. I feel the management is misleading investors. When the speaker mentioned that he is calculating the share price from the time the merger was announced, not from the date of the merger, Mr Vaidyanathan conveniently ignored this and repeated the share price from the merger date.

Isn’t it the management’s responsibility to review the bank’s books before the merger? How can he wash his hands of it now? This is very irresponsible of him. While the bank may do well in the future, his refusal to accept his mistakes is very bad.

I believe it is the responsibility of investors to keep the management in check. In fact, I’m glad the gentleman advocated for the average investor’s perspective so strongly. After all it is his money, and lack of return over 6 years is just unacceptable.