@Rj_Arora Is this as part of the SOIC Research desk?

Posts in category Value Pickr

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (05-03-2024)

@Rajat4636 Please don’t post wrong information. He has already given a SELL call on IIFL many days ago.

Tata Investment Corporation: Unusual discount to NAV (05-03-2024)

What is our leaning here, I don’t know , I was holding this stock for 13 years and sold it at all time high , not only that considering holding companies valuation we sold it at a considerable high valuation yet the stock moved 2x from there, I just wanted to ask the community what is the leaning , no regrets just want to know how can we learn from this ?? What should we consider in the future ?

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (05-03-2024)

Good morning folks, do you think promoters involved in this pump and dump. https://x.com/MicrocapAggar/status/1764607198636937582?s=08

See what is happening in Gensol

“Zenith Multi Trading DMCC” is caught by ED for fraud

Zenith is working for Chennai based Opeartor Gunavanth

It had got preferential in many SME pump and dump Guna operated stocks like Gensol, Nibe,veranda

M.Ravi & Dr also with them

#SEBI

Aditya Joshi of Sovernn is also mentioned by this person.

Be careful with SME stocks.

Rainbow Children’s Medicare – Niche player in Hospital Industry (05-03-2024)

I assume it is happening because of latest supreme court’s order to Govt. to standardize hospital charges.

Link- SC directs Centre to standardise healthcare procedure rate: How will it impact hospitals?

Rainbow enjoys over 35% OPM. That’s a big number for a hospital.

If Govt. intervenes here, the OPM is likely to go lower.

If that happens then why should market pay 50+ PE for Rainbow.

Hence the selling.

My thoughts only.

Disc: not invested

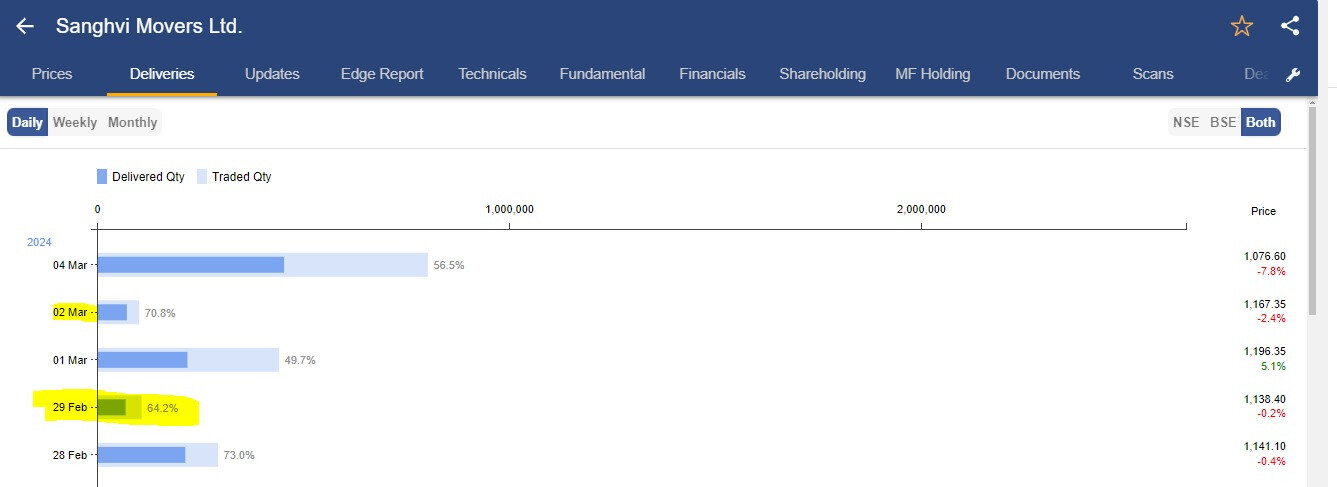

Sanghvi Movers (05-03-2024)

Thank you for putting across this write up. I’m sure this clears the confusion for a lot of investors.

Few reasons to think this maybe a ‘parked’ article and a classic case of shakeout are:

-

29th Feb article released, 5th march still no official announcement

-

bigger hands will only accumulate while and after shaking out weak hands and at DDs. this gives them liquidity for bigger buy quantities without raising the share price.

-

Price action shows a correction to 845-850 levels is pending, which might happen now. That would be an ~ 30-35% DD from the highs – A place when bigger hands, funds etc would want to keep accumulating – on the way down with panic selling and increased liquidty.

-

Image below clearly shows:

- 29th Feb article release date: 64% deliveries, no price reaction

- 1st march Friday: 50% deliveries, stock up 5%, pulling more weaker hands in at the top

*2nd Mar Saturday: 70% deliveries, low volumes

*4th Mar Monday: 57% deliveries with big downside price action.

A big price fall with massive volumes with 57% deliveries doesn’t add up, clearly someone’s accumulating. Moving forward will be interesting to see delivery percentages.

Disc: could be completely wrong in my assessment. Biased and invested since 2018-19.

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (05-03-2024)

(post deleted by author)

Shilchar Technologies – Power & Distribution Transformers – Sunrise Sector? (05-03-2024)

Elon Musk talking about shortage of voltage step-down transformers. Please listen at timestamp 5 minutes 58 seconds.

My portfolio updates and investment journey (05-03-2024)

Hi @Crishna ,

We are driven by our (personal) experiences (in some form Morgan Housel mentioned this in his book “Psychology of Money”). So some history (my experience) and some rationale to justify my buy.

Previous personal experience: I was invested in Dixon from pre-Covid. Luckily I made some 6-7x within 2 years. I was holding the stock even when it was consolidating for a long time. However, in one of the quarter there was flatness in revenues and contraction in margin, on top of it management downgraded its year-end guidance sharply. I exited the stock completely around 3K, now its 7k. So, may be I was trying to be smart in Syrma, sold in 550-600 range completely. Now re-entering at lower levels makes me look smart (only histroy will decide though).

Justification of my buy:

- When I listen to experts, they say EMS might be at juncture where IT was in late 90s. So seems huge runway for growth, I did not have any stock to play EMS theme and my historical bias made the tilt towrds it.

- Q3 FY24 was impacted by push of deliveries to Q4 FY24,thats why revenues and margin got impacted. In Jan they already did 362 crores of deliveries so company seems to be on track at least on revenue front.

- Management continues to guide for industry+ growth. I think industry shall grow in 30%.

- Margin: Margin contraction was expected from previous quarter (Q2FY24). Reason is they are getting into prescriptive business (like Dixon) where margins are lower but ROCEs are comparable to their business. So simply put company is focussed on EPS expansion and not margin exapnsion. Dixon at 4% margin trades at 100+PE. Syrma is around 80PE. However, Dixon has very good cash flows and ROCE. I am hoping Syrma turns good on these metrics in near future.

- Margin: Their product mix shift from industrial to consumer is leading to margin pressure. Consumer is growing at very high rate which is low margin business. So at business segment level margins are holding up but at overall level its the product mix issue. If they get into laptop business then margins will go down further, however EPS may expand and ROCEs may improve.

Please note that I can sell the stock any time.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example and learning purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

Rainbow Children’s Medicare – Niche player in Hospital Industry (05-03-2024)

Why shares fell upto 10% in two days ? Any news regarding this sel off.