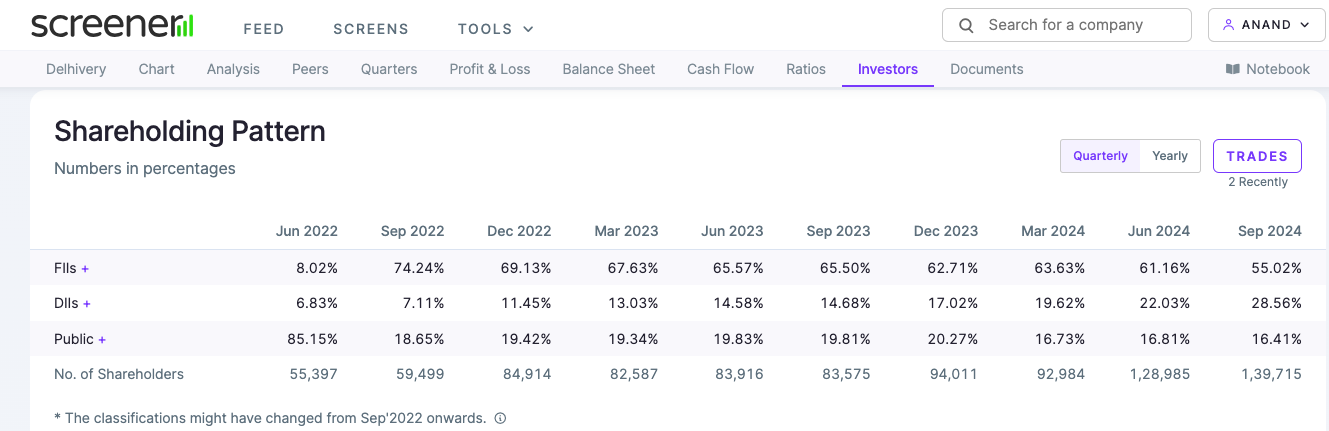

DII mainly buying FII stake (Canada Pension Fund complete exit, for instance)

DII mainly buying FII stake (Canada Pension Fund complete exit, for instance)

The result in the current quarter for all pipes companies will be subdued given the fall in steel prices, late budget and rainy season.

the steel prices have corrected by 30% to 40% from the highs leading to fall in realization of pipe making companies.

Hariom which is an integrated player makes pipe out of HR coil which has better realizations as compared to Patra Pipes so, the difference between Patra pipe & HR coil prices have now Shrinked down and now the difference is of 20% to 25% which is a good thing as the market gets more mature increased traction will be seen by HR coil Pipe manufactures as compared to Patra pipe Manufacturers due to better quality and strength.

This fall in price will lead to increased stocking leading to many pipe companies like Hi-tech pipes, JTL Industries and more posting record volume but the realizations will be more or less flattish.

this, is a short to mid term i expect that by Q3 or Q4 of this year we’ll also see reversal in steel prices and value growth along with volume growth for pipe companies.

Point to highlight:

Disclaimer: Invested in the company

Data well captured!! Who could have guessed the collapse of profitability in IDFC Bank… Profits down 70%… Federal Bank is a steady tortoise… Hopefully

Data well captured!! Who could have guessed the collapse of profitability in IDFC Bank… Profits down 70%… Federal Bank is a steady tortoise… Hopefully

I recently noted a few companies reporting getting ethanol allocation… Are these tenders filling at old rates? There was talk of ethanol prices increasing, but havent seen any announcement so far…Any inputs

I recently noted a few companies reporting getting ethanol allocation… Are these tenders filling at old rates? There was talk of ethanol prices increasing, but havent seen any announcement so far…Any inputs

Given the management is going ahead with the QIP, it knows that there are better days ahead. I just exited the counter after losing patience on the subject of debt management.

Given the management is going ahead with the QIP, it knows that there are better days ahead. I just exited the counter after losing patience on the subject of debt management.

My two bits… ITC is a perennial hold and business that has so many moving pieces that a few of them out shine and a few lag… Agri biz that was a laggard last few quarters (when the export of wheat was banned) has come up and the paper board business is currently facing headwinds… The hotels business is a deep cycle business, with huge capital demand and bad return on capital… hence the companies moving towards the asset light model, where they just deploy their ops expertise and mktg muscle, with a 3rd party putting in the capital. I would be looking to sell the hotel stock at the 1st good opportunity, mat want to see a quarter or 2…BAT will certainly exit, will try do it in an efficient way, but their stake will not amount to much, as the Parent will continue to own 40%. so it remains to be seen, as to who will buy… maybe retail public…