what about the valuation of marine electricals…?

Posts in category Value Pickr

Dreamfolks services limited( DFS) (04-03-2024)

DreamFolks had a decent Q3 performance (in absolute terms) – with revenue up 50% YoY + gross margins up 15% YoY. However in terms of margin %, both gross margins / EBITDA were down YoY.

I wrote a detailed article covering the performance of DreamFolks – here

Here’s a summary of DreamFolks Q3 performance ![]()

Pros

- DreamFolks launched ‘The DreamFolks Club’ – an exclusive membership program where it can bundle together it’s various services into a package. There are 4 package variants (ranging from INR 6,999 to INR 99,999). This is to cater to people who don’t have debit cards / credit cards and still want to avail benefits.

- The preliminary focus of the program would be to attract large enterprise customers (B2B) who can buy such programs to rewards their employees / customers / channel partners. However a normal individual can also buy into the membership directly from the website.

- Entered into partnership with Grey Wall (Russia’s largest lounge operator) whereby Indian passengers will gain access to airport lounges + railways lounges in Russia.

- Expanded their presence in railway lounges in Chennai & Old Delhi – the company continues to maintain 100% coverage in railway lounges in India.

- Added two new services – Pathology testing & Gifting services

- Major growth drivers will be increase in credit card penetration (currently 5.5%) and growth in air passenger traffic

Cons

- Credit card companies are moving from fixed benefits model to spend based model which will impact the volumes for the company

- Other services (e-SIM, Visa services, Golf, Spa) contribute <2% of total topline. Management expects these services to contribute around 20% in the next 4-5 years (I think the management should aggressively push for this in the next 1-2 years and not 4-5 years)

- Employee benefit expenses have increased due to increase in ESOP cost

- Q4 is expected to be flat in terms of topline / bottomline sequentially

Concluding Thoughts

I think the membership program has potential, but how much? Can it be profitable? Can it scale? Do they have some sort of pricing power here? I hope the management can answer such questions in the future.

The company already has 95% market share of the card based lounge access market – so not a lot of room to grow unless air passengers grow and more credit cards enter the market. The impact of shifting to a spend based model by credit card companies will have to be seen over the next few Qs.

Disclosure: Recently sold all my position in the stock due to low confidence in the B-model. Tracking, will buy if it falls atleast 30% from CMP

Dreamfolks services limited( DFS) (04-03-2024)

DreamFolks had a decent Q3 performance (in absolute terms) – with revenue up 50% YoY + gross margins up 15% YoY. However in terms of margin %, both gross margins / EBITDA were down YoY.

I wrote a detailed article covering the performance of DreamFolks – here

Here’s a summary of DreamFolks Q3 performance ![]()

Pros

- DreamFolks launched ‘The DreamFolks Club’ – an exclusive membership program where it can bundle together it’s various services into a package. There are 4 package variants (ranging from INR 6,999 to INR 99,999). This is to cater to people who don’t have debit cards / credit cards and still want to avail benefits.

- The preliminary focus of the program would be to attract large enterprise customers (B2B) who can buy such programs to rewards their employees / customers / channel partners. However a normal individual can also buy into the membership directly from the website.

- Entered into partnership with Grey Wall (Russia’s largest lounge operator) whereby Indian passengers will gain access to airport lounges + railways lounges in Russia.

- Expanded their presence in railway lounges in Chennai & Old Delhi – the company continues to maintain 100% coverage in railway lounges in India.

- Added two new services – Pathology testing & Gifting services

- Major growth drivers will be increase in credit card penetration (currently 5.5%) and growth in air passenger traffic

Cons

- Credit card companies are moving from fixed benefits model to spend based model which will impact the volumes for the company

- Other services (e-SIM, Visa services, Golf, Spa) contribute <2% of total topline. Management expects these services to contribute around 20% in the next 4-5 years (I think the management should aggressively push for this in the next 1-2 years and not 4-5 years)

- Employee benefit expenses have increased due to increase in ESOP cost

- Q4 is expected to be flat in terms of topline / bottomline sequentially

Concluding Thoughts

I think the membership program has potential, but how much? Can it be profitable? Can it scale? Do they have some sort of pricing power here? I hope the management can answer such questions in the future.

The company already has 95% market share of the card based lounge access market – so not a lot of room to grow unless air passengers grow and more credit cards enter the market. The impact of shifting to a spend based model by credit card companies will have to be seen over the next few Qs.

Disclosure: Recently sold all my position in the stock due to low confidence in the B-model. Tracking, will buy if it falls atleast 30% from CMP

Pune investors group (04-03-2024)

I am in. Nice move! Will benefit all!!

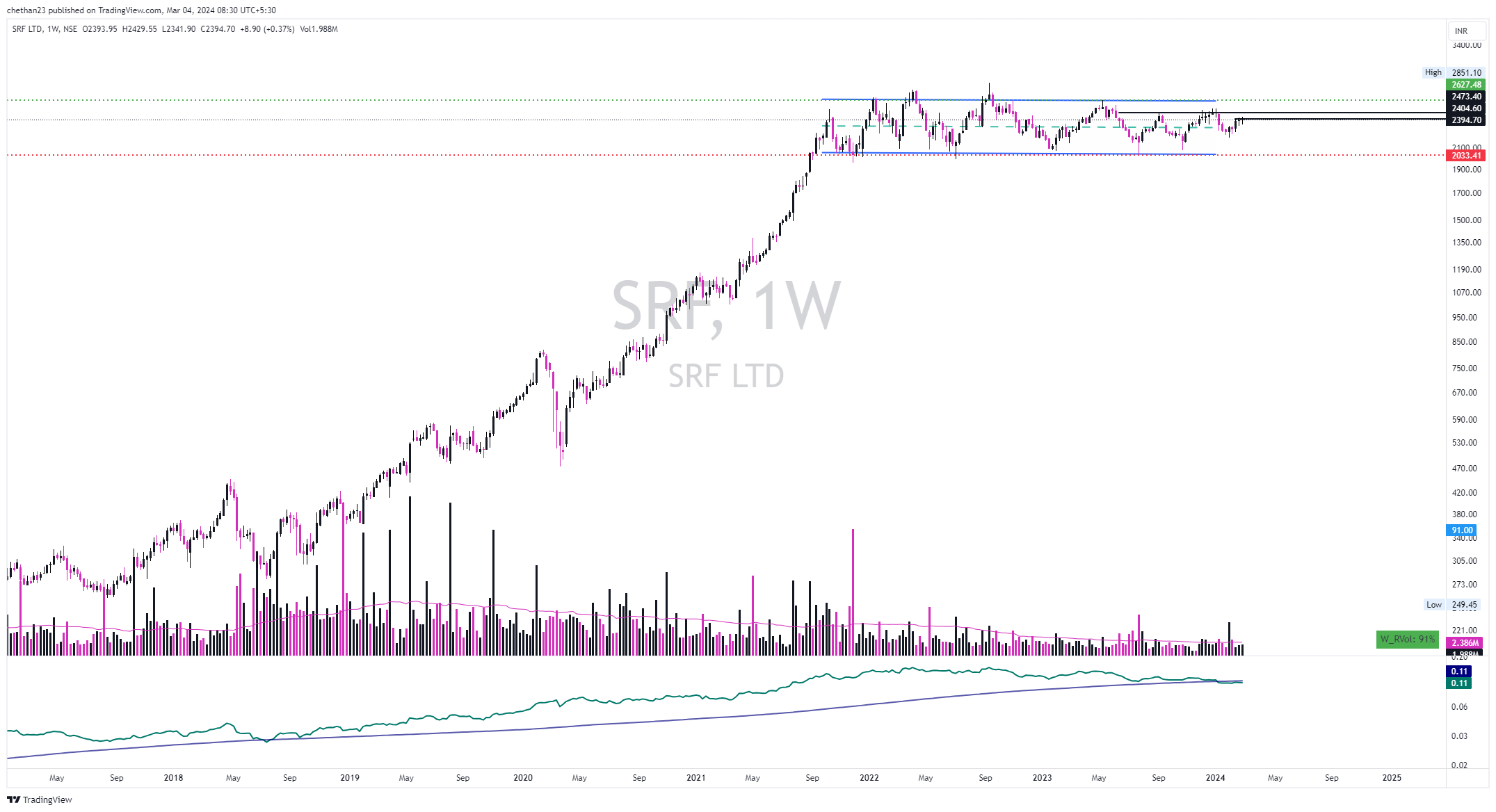

52 week highs and all time highs strategy (04-03-2024)

SRF, After strong up move and now it has consolidated for over 2 .5 years seems the move can be expected in this, I was watching other chemical related stocks most of them are getting into right structure, near Stage 4 BO. so there might be some sector tailwinds also.

Avenue Supermart: a compounding machine? (04-03-2024)

Compared to a lease dependent business, PnL costs (Interest and Depreciation) would keep reducing with time. Per store sales can be stepped up by making additional floors that are dedicated to the new lines of business [Speculating].

Overall, it enables the business to maintain its competitive advantage – offer low prices to challenge any current or future competition.

Buy Unlisted Shares (04-03-2024)

Mostly at around 66. Price discovery is a big problem in unlisted space. It depends how well you negotiate with the broker.

Buy Unlisted Shares (04-03-2024)

Mostly at around 66. Price discovery is a big problem in unlisted space. It depends how well you negotiate with the broker.

Sunshield Chemicals Ltd (04-03-2024)

who are these other two producers?

Sunshield Chemicals Ltd (04-03-2024)

who are these other two producers?