Hey, We do have certain plans to provide alerts through WhatsApp. It is on our to-do lists and we will try to work on it in the coming days.

Posts in category Value Pickr

My US stock portfolio – started (01-03-2024)

hi, for international investing, now that GORWW has folded it’s service (kind of), which service is best?

appears to me Interactive Brokers is very cheap and reliable. Perhaps Indmoney too?

do share views and thoughts on this.

many thanks

VP Bhubaneswar/Odisha Meetups (01-03-2024)

Hopefully, with time. For now, please confirm your attendance for this Sunday 5 PM.

Microcap momentum portfolio (01-03-2024)

Your disclosure is mandatory.

Easy Trip Planners (Easemytrip) – An outlier in OTA (01-03-2024)

So sir, need to look at other hospitality and travel sector players. As the sector is prospective, your take please, Thank you.

Mudit’s Portfolio (Passively Active) (01-03-2024)

Lets say the government and court allows Hospitals to even charge higher than CGHS rates as hospitals will not bow down easily. They will use different techniques to maintain premium pricing power.

Even then margins will drop. Ebidta margins of 30%+ and 20%+ NPM will be unsustainable. Look to it dropping to more sustainable rates. 10-15% NPM are global average. So, it would settle there.

But since the government depends on high FDI and investments from PE and SWF capital to boost the sector, it’s also possible it may drop just a few points and not drastically.

All depends on how seriously government manages the contradictons.

Is small, micro cap sector over priced? (01-03-2024)

Hi, ![]() I sold some stocks, realised meagre profit, amt will come from dp account to bank account in three days, so want to reinvest in Gold etf, to avoid tax is it okay sir, or any other instrument is better please advice.

I sold some stocks, realised meagre profit, amt will come from dp account to bank account in three days, so want to reinvest in Gold etf, to avoid tax is it okay sir, or any other instrument is better please advice.

Deepak Fertilizers and Petrochemicals (01-03-2024)

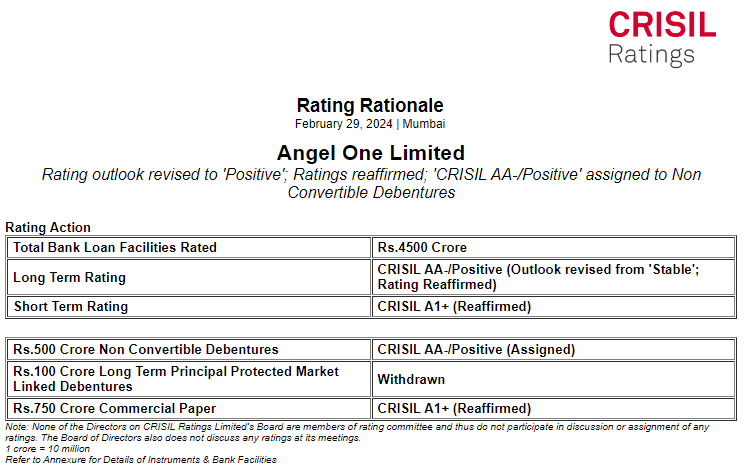

Key headwinds as per rating rationale:

The ratings are, however, constrained by the agro -climatic and regulatory risks in the fertiliser business and the vulnerability of the chemical division’s profitability to the inherent price cyclicality along with the volatility in natural gas prices. The ratings are also constrained by the large debt- funded capex plan being undertaken by the company i.e., the technical ammonium nitrate (TAN) project at Gopalpur with a capital outlay of nearly Rs. 2,200 crore and the nitric acid plant at Dahej with a capital outlay of Rs. 1,950 crore. The large capex plan exposes the company to project execution risks and timely commissioning of hese projects and within the proposed capital outlay will remain a key monitorable going forward.

DFPCL is reorganising its operations under fertiliser and chemicals business separately. On a consolidated basis, ICRA does not expect the reorganisation to have any financial impact, as it will help in streamlining the company’s operations. However, ICRA will continue to monitor the developments on this front.

Further, ICRA also notes the appeal filed by MAL in response to the receipt of assessment and demand orders for the block period (assessment year 2013 2014 to assessment year 2019 -2020) pursuant to the search operation conducted by the income tax department in November 2018, resulting in a demand of Rs. 486 crore (including interest). ICRA will continue to monitor the development on this front.

Large debt – funded capex :The company has recently commissioned its 5,10,000- MTPA ammonia plant at Taloja in August 2023 with a capital outlay of Rs. 4,030 crore till September 2023 and will be incurring another Rs. 470 crore, including purchase of certain stores and spares within FY2024.

As on September 30, 2023, the company had an outstanding external long-

term debt of Rs. 3,175 crore. However, due to the long repayment tenure of the term loans, the annual debt repayments are likely to remain modest (~Rs. 122 crore in H2 FY2024, Rs. 389 crore in FY2025 and ~Rs. 535 crore in FY2026)

Their ultimate customer for TAN was Coal India and if Coal India itself is coming up with such huge capacity it will be very callenging for the Company to sell its TAN from upcoming new plant and Coal India plant is also coming up in Orissa.

Balkrishna Industries (01-03-2024)

Agree with your observation. A good set of numbers and price correction has made the PE correction aggressive.

In my opinion, all export oriented companies will continue derating till clarity on Red Sea operations is seen. BKT is primarily an export oriented company. Freight and Insurance costs will be a drag till they do not pass on the cost to customers.

Most of this impact will be felt in Q4’FY24 as the issue was raised E/Nov’23. So most of Q3 was reasonably stable. My plan is to wait and watch for Q4 results and then decide the way forward. Avoiding catching a falling knife. ![]()

Disc: Please do your due diligence. Not an investment or sell advice.