Thanks, error was due to info taken from bard ai…deleting it…

Posts in category Value Pickr

Demergers on the radar (25-02-2024)

The Board of Directors of Jubilant Agri and Consumer Products Limited (“Wholly Owned Subsidiary of the Company / JACPL”) at its meeting held today, i.e., February 9, 2024, discussed and in principally approved a restructuring plan under which its Agri Products and Sulphuric Acid Business will be demerged in a separate company.

https://www.bseindia.com/xml-data/corpfiling/AttachHis/9a2e2d03-4425-4a58-97d0-a8ee64b7fde5.pdf

All E Technologies, making businesses ready for AI (25-02-2024)

Thanks, this is very useful. I had stumbled upon All E Tech back in September 2023. I even listened to the entire con call back then and made some notes, which I am pasting here again for your reference. In case you spot something useful or interesting:)

Found this company interesting as the management seems to know their stuff. Ended up going through the entire recording. Took some running notes, sharing it below.

For their IP led products, they get around 25% of the rev share. Going forward this share will only increase. IP component revenue is recurring every year, in addition to MS component revenue and then services component.

Risks – Need to strengthen international sales, gain more business outside of India. Keep cost of talent low.

All customer relationships are multiple years (5,10 yrs). And they are always increasing their business with Alletech

Adding a new Sales head in Toronto, have a sales office in Dallas – will continue to focus on sales as opportunities open up

In 2 quarters will bring solution on MS cloud to make MS co-sell ready. This is both in international and Indian market. Will leverage MS and Salesforce relationship to sell more, both in enterprise space and corporate managed accounts.

Key differentiator – 1. They are development partners and not just implementation partners for MS business applications, they have their own engineering teams working closely with MS because they know the products in and out. 2. Scale and experience – Having done more than 800 projects bodes well for clients’ confidence in them. 3. 97% business comes from existing customers. Customer life time value is key and focus will be this.

New deals – sophisticated , large footprint solutions so organizations take time to absorb and scale. Once finalized, they tend to go on for years. Typical sales cycle is 6 months (average). Customers don’t come to buy MS products, they want customized solutions which Alletech provides. Ball park of typical large customer revenue is 1Crore.

Started rolling out in international markets as well like Malaysia, Dubai, Antigua.

I liked the way management answered most of the questions – showed their core competence, focus on business, refused to speculate on matters of stock market and share price, seem focused on large term client relationships rather than short term profits.

Margins guidance – In 2-3 years times, share of International business and IP led solutions will grow and hence margins WILL grow.

There were also question from existing investors cum customers – they also sound like they are happy with how things are shaping up so far.

Azure is picking up very quickly in ways Alletech hasn’t thought of 1-2 quarters ago. Currently in the process of moving another competing smaller foot print financial accounting software in India from their own cloud to Azure (expect announcement in next con call). Once moved, solution would run 40000 users on Azure, ramping up to over 100000 users. So there is large complex projects/businesses coming in. Total cloud MS Azure cloud market is huge and growing faster than industry which bodes well for Alletech.

They didn’t disclose the size of the order book but said its substantial.

Large part of cash on books (i think ~100 crores) will be utilized for inorganic growth. 2 acquisitions may happen in the future.

No Plan to explore EU or S American markets for now – APAC is a possibility

Financials are healthy as it reflects in the AR. They have booked a loss of 90 lakhs in one of the subsidiaries 2 years ago which is no longer operational (something on the lines of writing off a loan since they ended up merging with the then acquired entity)

Why are the standalone numbers not growing? – You should look at consolidated numbers since we are working in parallel to increase international business so looking at standalone numbers can be misleading.

My portfolio updates and investment journey (25-02-2024)

My first buy was at 2485 on 27th September 2023, lowest price buy was at 2210 on 6th October, highest price buy is at 4410 on 23rd February 2024 and overall average is 2976.

I will delete this message in sometime as this is not a value add.

Salzer Electronics (25-02-2024)

Unfortunately, neither genus or hpl provide the cost they are charging for smart meters or margins, I have only read the last 2-3 concalls at most so not sure if this was provided before or maybe I missed that. HPL did state in the recent concall that they don’t provide the number due to competitive reasons. We would probably need to do some approximations to get potential revenue and margins.

Overall, HPL and Genus have not more than 2 cr meters / year capacities (with expansions) and to get to 15 cr installations within 3-4 years, there is enough scope for Salzer to not underprice their product. Purely my gut feeling.

All E Technologies, making businesses ready for AI (25-02-2024)

Very nicely explained Aadhar

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (25-02-2024)

I don’t think any of them is accurate. I searched for a few names and couldn’t find any of them related to the company.

Neelesh Choukesy – PPFAS (I have invested in this for quite some. Never heard of a person called Neelesh)

Anil Talreja – Edelweiss (No such person existed or resigned)

Jaideep Goswami – AU Small Finance Bank (Same here).

AGI Greenpac- on the cusp of growth? (25-02-2024)

Well in that case you are late. SC heard the case for the first and the only time around 16 oct (don’t remember the exact date) and admitted it for further hearings…

Stock corrected from around 1000 Rs.

Two quarterly results are declared after that.

I believe that Even without HNG the stock has still to realise it’s true potential…(individual call)

The harsh portfolio! (24-02-2024)

I have a slightly unconventional thought process on this. Any activity aiming to make future predictions is speculation. In my line of work, I create mathematical models projecting how climate change might affect water resources over the next 50 to 100 years. So you could say I’m a full-on speculator. I guess you could call me an “investor” if you really wanted to, but it doesn’t quite capture what I do.

Very hard to answer this question. I did some work on previous agchem downcycles which I am sharing below, maybe it can add some value.

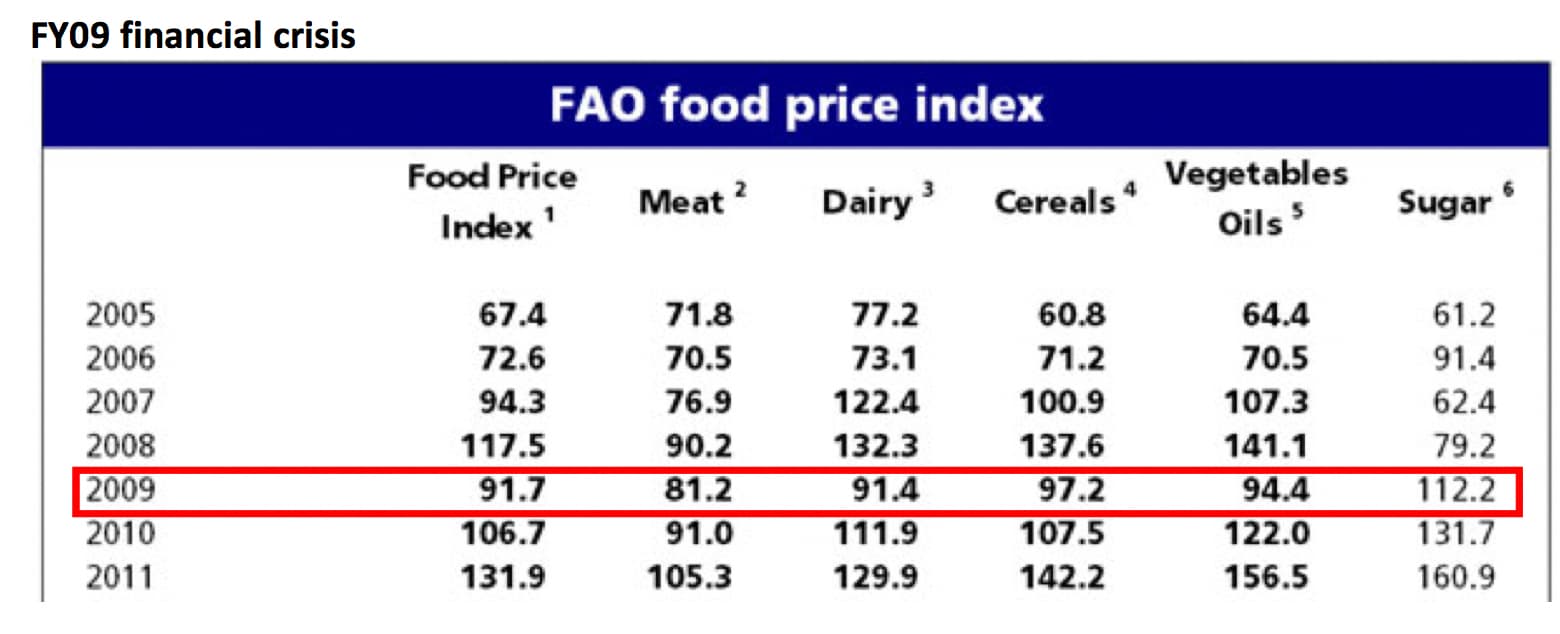

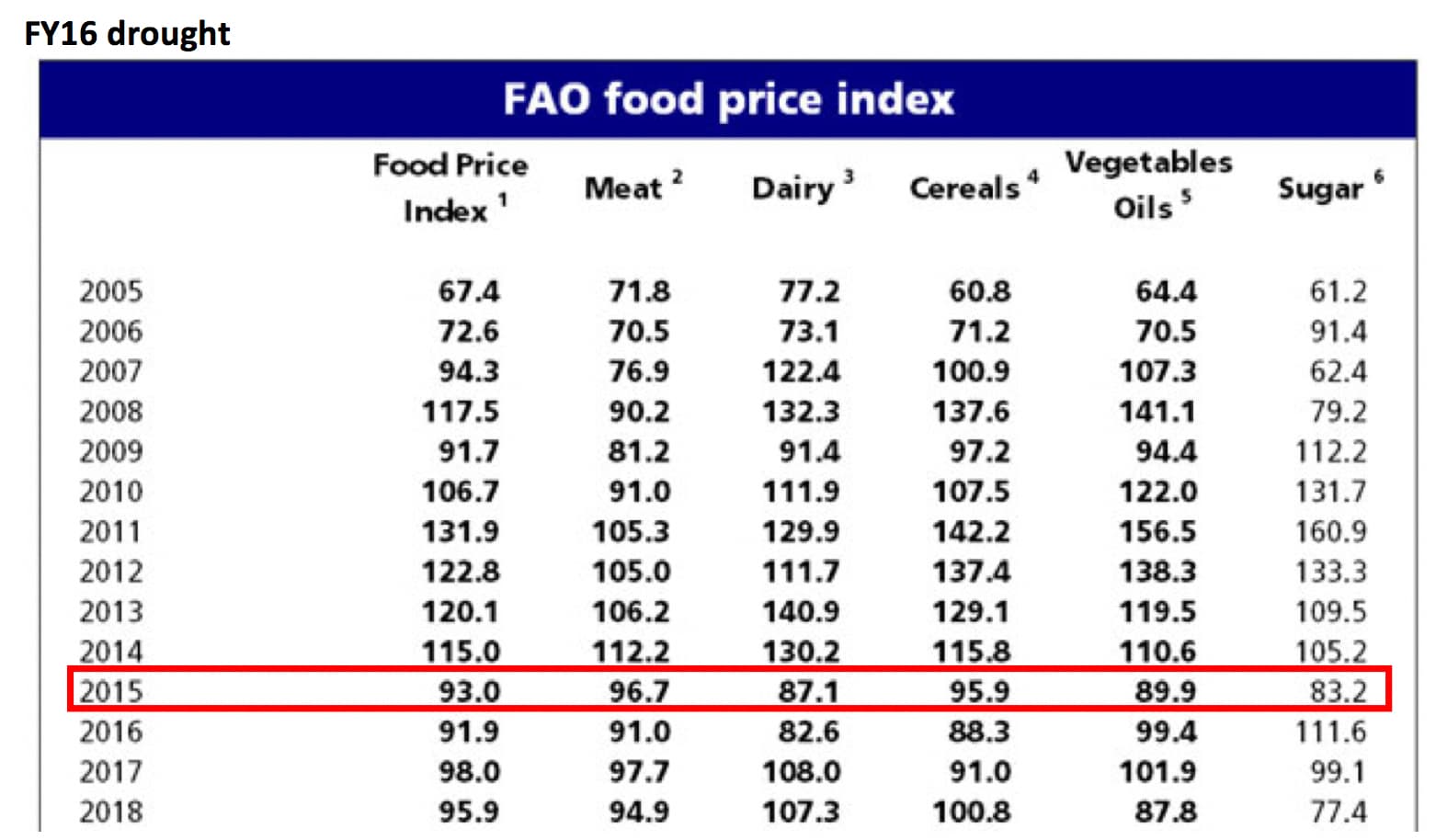

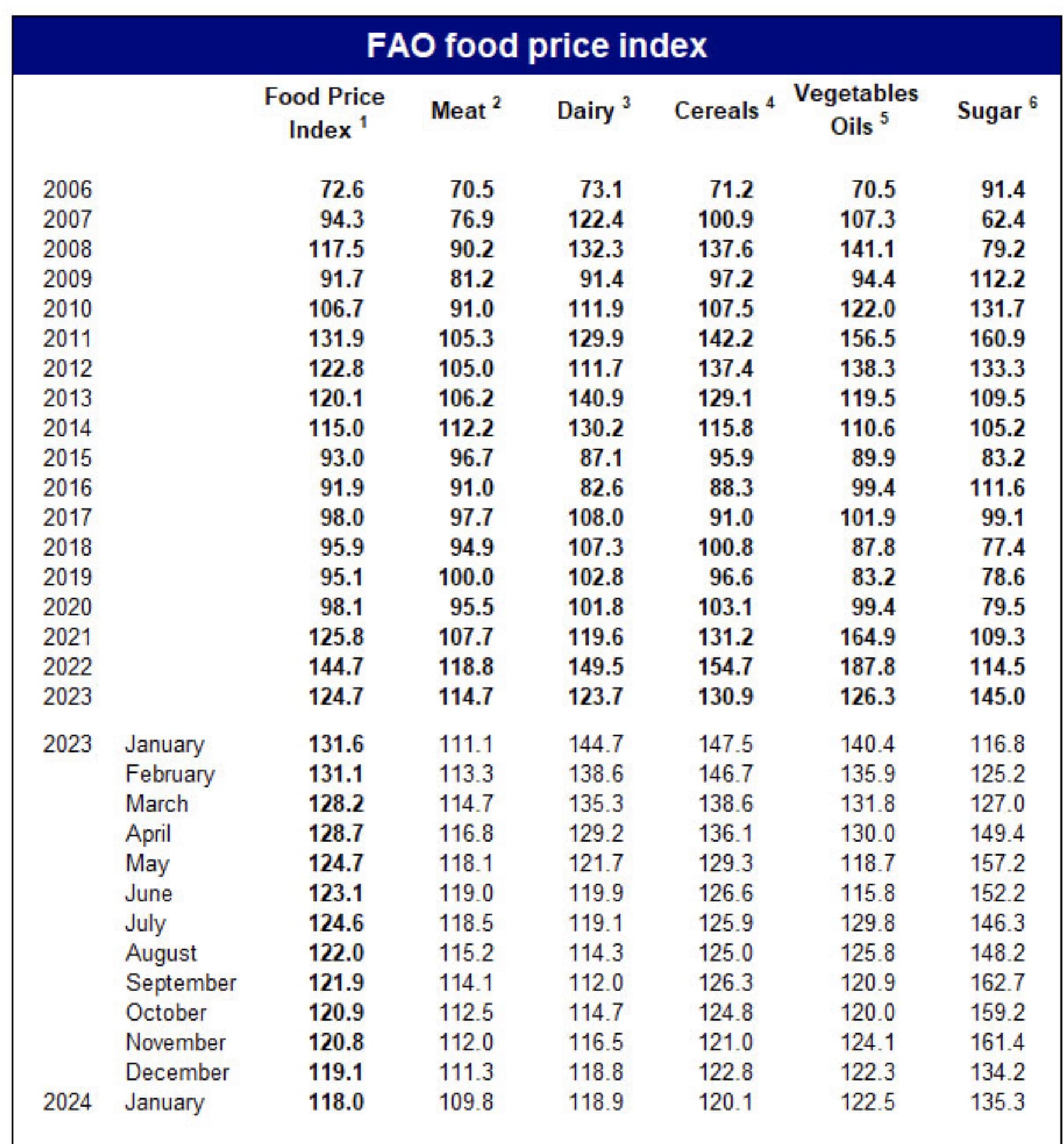

Analysis of downcycles (FY09, FY16) – 23.06.2023

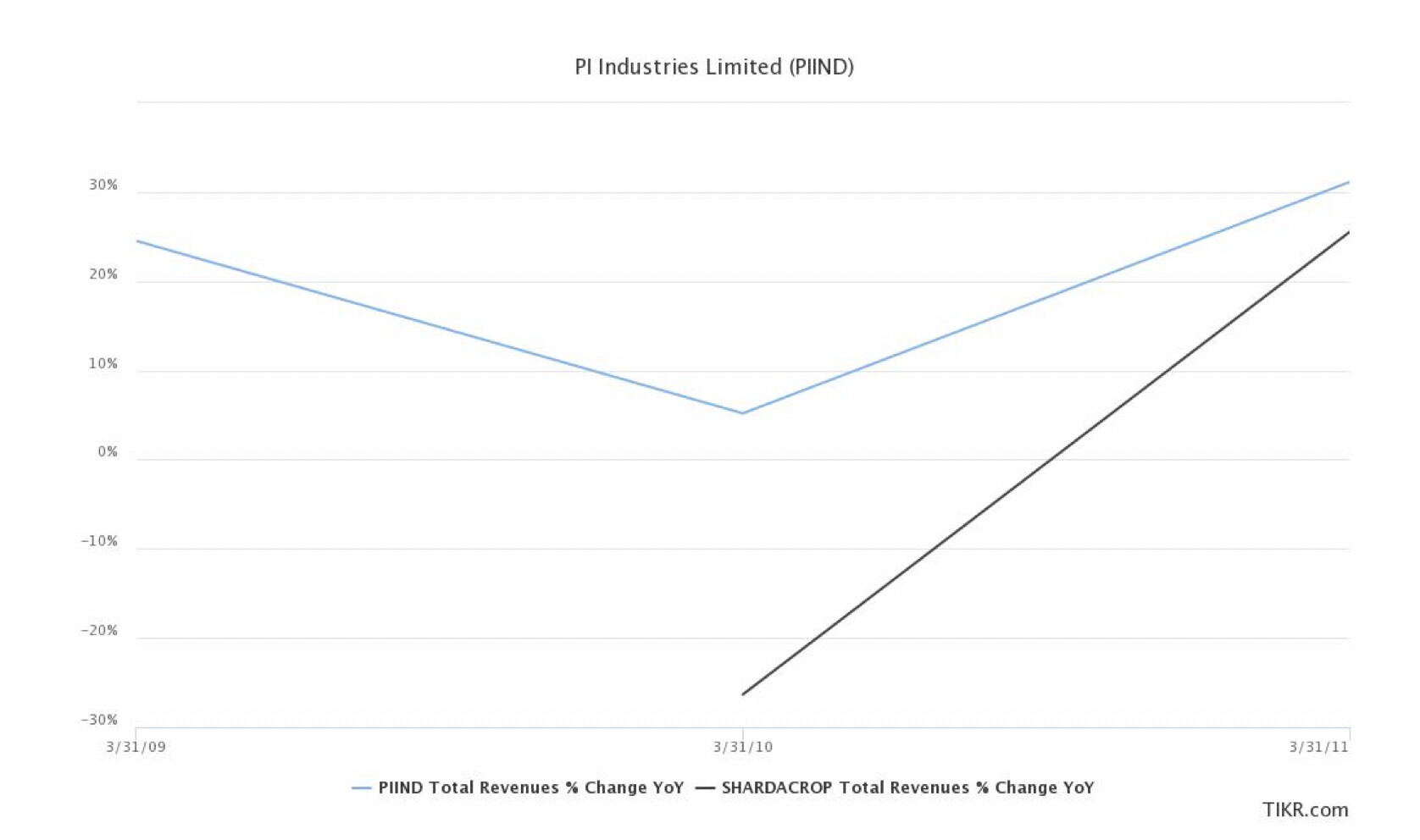

Underlying logic is when FAO food price index goes down sharply, farmers use less pesticides. Let’s see this with data of Sharda Cropchem and PI Industries. I have excluded UPL as they have kept growing in downcycles by acquisition

In 2009, FAO food price index dropped by 22%. This impacted sales growth of PIIND and Sharda in FY10. FY10 sales growth for PIIND declined to 5% (vs 25% in FY09 & 31% in FY11). The effect was more stark on Sharda, whose FY10 sales declined by 26% (vs 25% growth in FY11). However, both companies had a very clear revival in growth rates in FY11 as food prices recovered very quickly.

The next major downcycle was in 2015 where FAO food price index dropped by 19%. The impact this time around was more on PIIND, whose revenue growth rate in FY16 declined to 8% (vs 22% in FY15 and 9% in FY17). Sales growth for PIIND only recovered in FY19. Sharda managed this downcycle better, but their FY16 sales growth declined to 15% (vs 34% in FY15 and 14% in FY17). Their sales growth recovered in FY18.

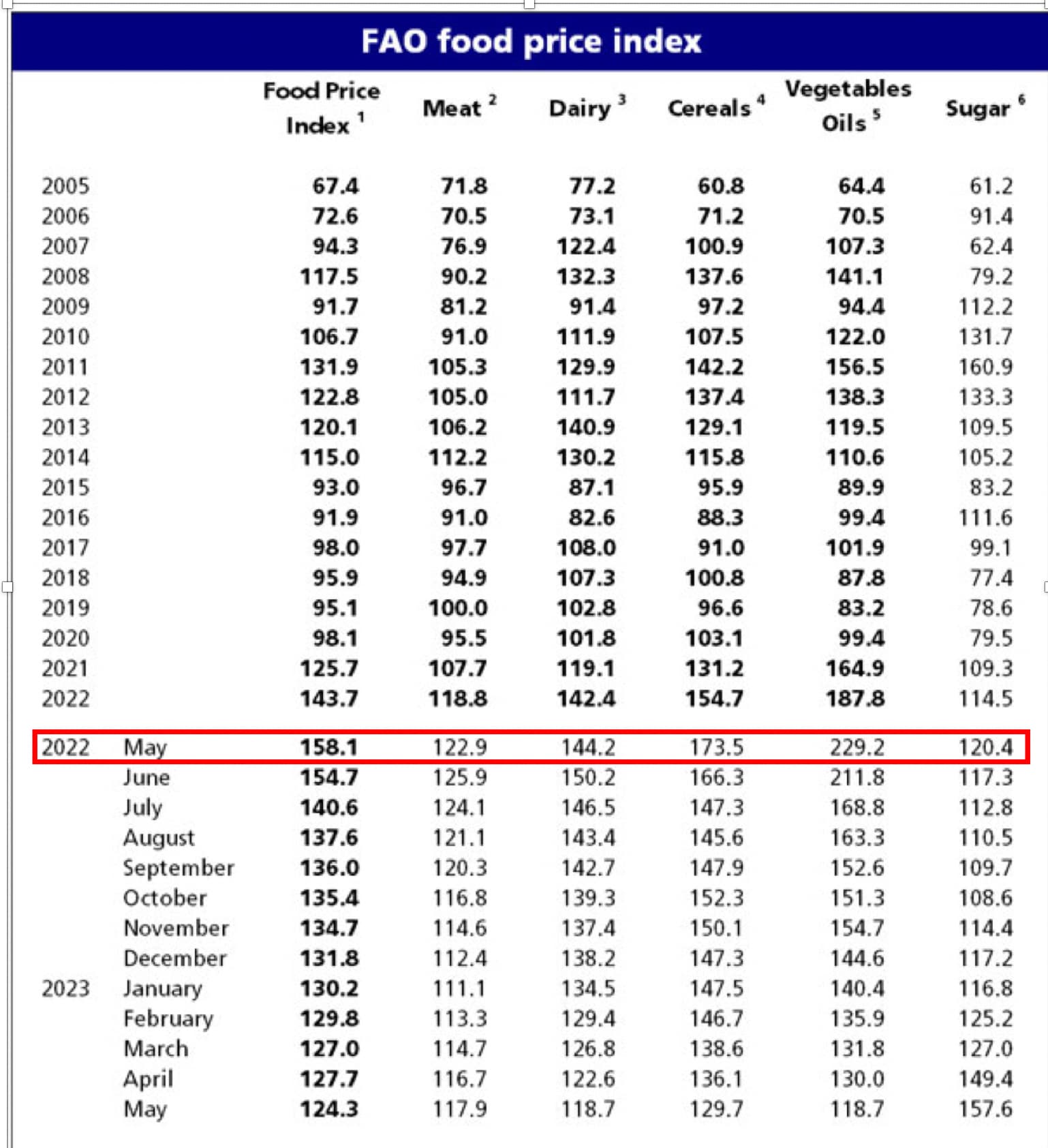

Current scenario

This time around, food prices peaked in May 2022 and have been showing decline for the last 1-year. It’s down by 21% already but hasn’t come down below 100, where in the past they have bottomed out. Given how high food prices became, recovery this time around can be prolonged.

Jan 2024 food prices are still 118 (very high by historical standards). So its hard to call it a bottom.

Avanti has struggled in past couple of years to pass on wheat and soya price increase because government regulated the final feed prices. Avanti nos are not really bad, look at other feed cos to see the carnage happening in this space (waterbase in losses). Avanti is a clear cut leader.

As explained in my agchem analysis above, we are coming out of a huge upcycle. I am personally still bullish on Punjab and have added shares in the last 30 days. I feel they have managed the whole downturn quite well, recovering their margins when most technical manufacturers are really struggling.