The reduce in Import duty would definitely be an improvement going forward , however considering they have a huge stock pile of old inventory on which they have already paid the duty this may be a bit counterintuitive. Their competitors will be producing with the lower cost raw material.

Posts in category Value Pickr

Welspun India – most vertically integrated textile co (22-02-2024)

What explains the valuation gap between Welspun & Trident? Both are close in terms of operations except that Trident is backward integrated into Yarn (which is at best 4-5% EBITDA business).

- Welspun’s EBITDA margin 15.5% vs 15.1% for Trident.

- Welspun has a higher B2C share vis-a-vis Trident which is more B2B

- Welspun has higher Bed Linen capacity vis-a-vis Trident and hence greater operating leverage in play

- Similar net debt levels (1540crs for Welspun vs 1450 for Trident). Infact, the debt ratios are better for Welspun due to higher absolute EBITDA (1114 crs for Welspun vs 766crs for Trident)

In terms of valuation

If anything its Trident that had an income tax raid recently. Can’t understand the gap.

What’s the logic?

Marksans Pharma- Can it be the next Pharma Biggie? (22-02-2024)

Highest ever quarterly sales at 586 crores.

US market grew by 16 % QoQ

Filed DMF for one products and planning to file another DMF for backward integration this quarter.

Cash balance at 688 crores

Consistent improvement in gross and EBITDA margins.

Teva facility is yet to break even. Operating leverage will kick in once sales increase at Teva facility. Expecting more contribution from Teva in Q4. The company seemed confident in future growth.

Expecting 600 crores sales from Teva facility in FY 25. Management sees a lot of prospects in US markets. Mentioned that they had just touched the tip of an iceberg. Sees a lot of prospects in the US market. Focussing on cough, allergy, digestive and cold OTC markets.

Spent 29.4 crores on R & D which is 1.8 % of sales.

Capex of 160 crores for the 9 months. Expecting a total capex of 250 – 300 crores over the next 2 years including the cost of acquisition of Teva. Nothing concrete on acquisition in Europe.

In US, the flu season starts in winter and a part of the QoQ growth could be attributed to this.

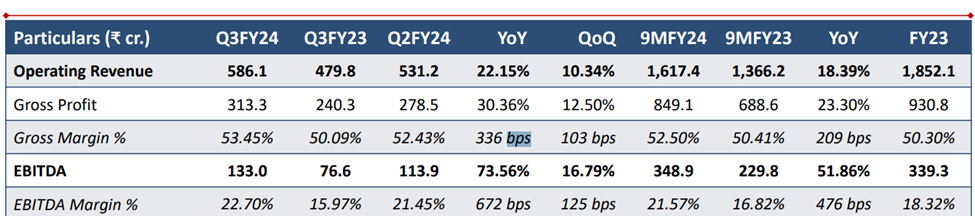

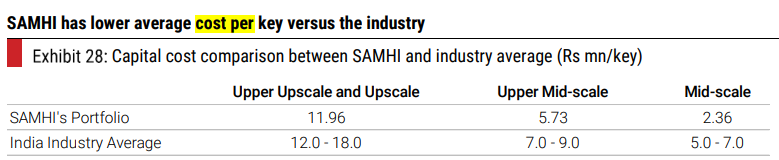

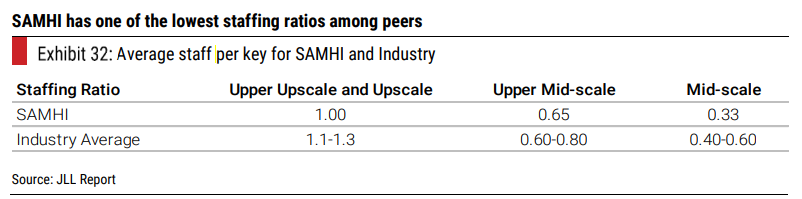

Samhi Hotels – Turnaround with Tailwinds (22-02-2024)

Thanks for starting this thread, something which I had in my list for a couple of weeks now ![]()

You have covered almost all important points. A couple of points which I found interesting are:

- They do not build the hotels from scratch. They go for dislocated hotels which are not working up to their optimum capacities. Once these hotels are identified, they renovate these hotels, re-brand those and operate those hotels with the likes of Marriott, IHG and Hyatt.

This enables them to do away with the challenges involved in building the asset from scratch. Moreover their cost per rooms are very low as compared to industry.

- They have shared service centres where they carry out operations such as finance, accounting, engineering and procurement centrally. This allows them to have lowest average staff cost per room.

- The management has extensive experience in the hotel industry.

A couple of risks that I found are:

- Institutional/PE holding.

- Operates in the upper-midscale and midscale segment, which faces higher competion.

Disc: Invested.

Ujjivan Financial – Small Finance Bank (22-02-2024)

Is it possible that company can decide to not go for the reverse merger and can cancel it? Or is it confirmed?

KDDL (Ethos Watches) – Scalable business model at an inflection point? (22-02-2024)

KDDL’s own business is not growing. See this quarter’s numbers.

Nifty index PE, PB & dividend yield ratio chart (22-02-2024)

I have combined the PE, PB & Dividend yield data of all indexes of NSE available historically & put together into charts at Yogya Capital for the investor community.

You can see charts for all index with option of sorting data by date which i couldnt find free. So here’s the link –

Yogya Capital

Make the best use of it ![]()

Jupiter life line hospital- fairly valued (22-02-2024)

Hi Ravi,

Thanks for commenting.

Jupiter is currently 70 PE and with a market cap of Rs 9700 Cr.

Assuming net profit margin more than 15% would be to much optimistic outlook. Narayan hyudaya has 15%, Max has 20% and apollo has 4% net profit margin. so 15% expectation is itself on higher side.

CAGR coming negative because I am not valuing year 2026 and 2027 at 70 PE droping PE at industry level which is 50. so PE valuation is dropping price by 30%.

In Future, rise in share price will have to be totally on earning basis, not from PE expansion. Hence giving multiple of more than 50 is very risky.

Aaron Industries Ltd- The Elevator Play (22-02-2024)

Aaron Industries installed steel embossing machine.

Steel Embossing machine impresses patterns on stainless steel sheets.Import substitute as 90% of such sheet was being imported to India.

Only company in India capable of offering more than seven varieties of embossing patterns on stainless steel sheets

AARON_22022024111733_PressRelease_22022024.pdf (1.6 MB)

Power Mech Projects – Not a typical Power Infra Company (22-02-2024)

Power sector and Railway sector’s beneficiary.

Tailwinds in Nuclear space should provide a push to Powermech.