It will be great if you can provide details on why we should avoid this? This is FMCG business and can have a potential to grow. What is your anti thesis?

Posts in category Value Pickr

Srivari Spices and Foods Limited (21-02-2024)

Please avoid this stock , I can’t write beyond a point .i am from Hyderabad this co also from same place .

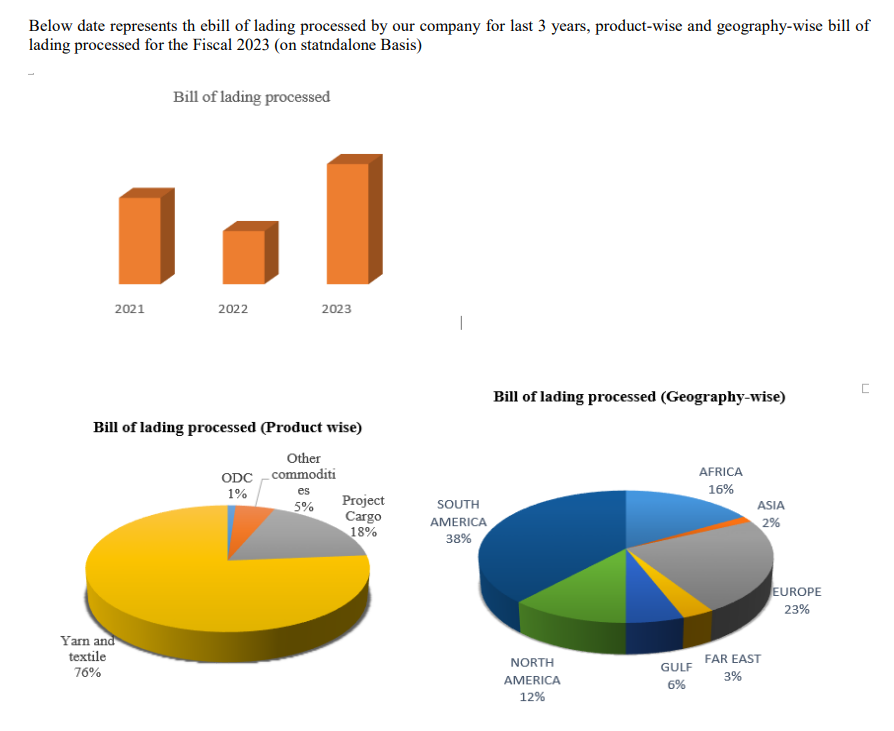

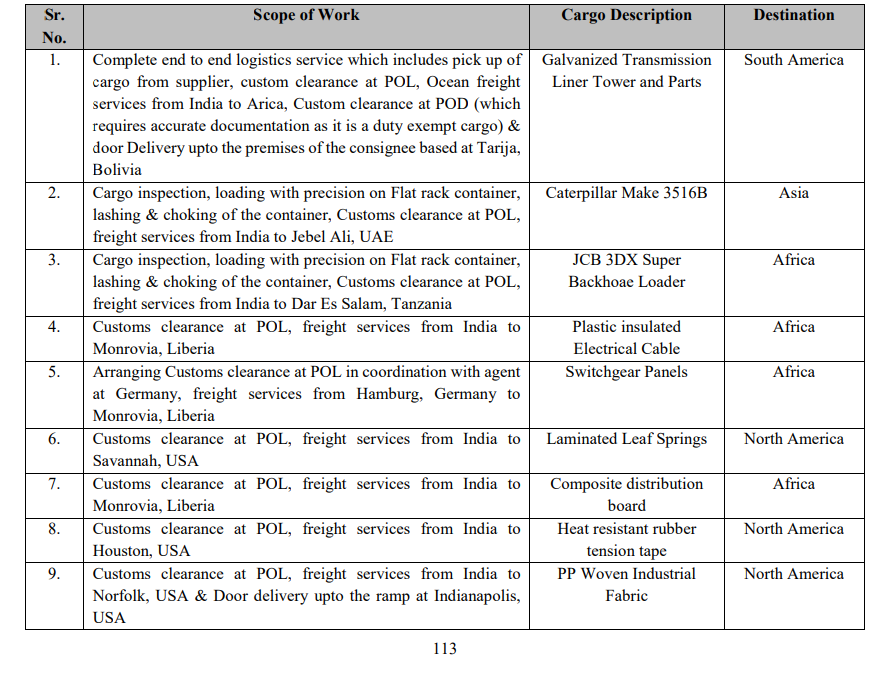

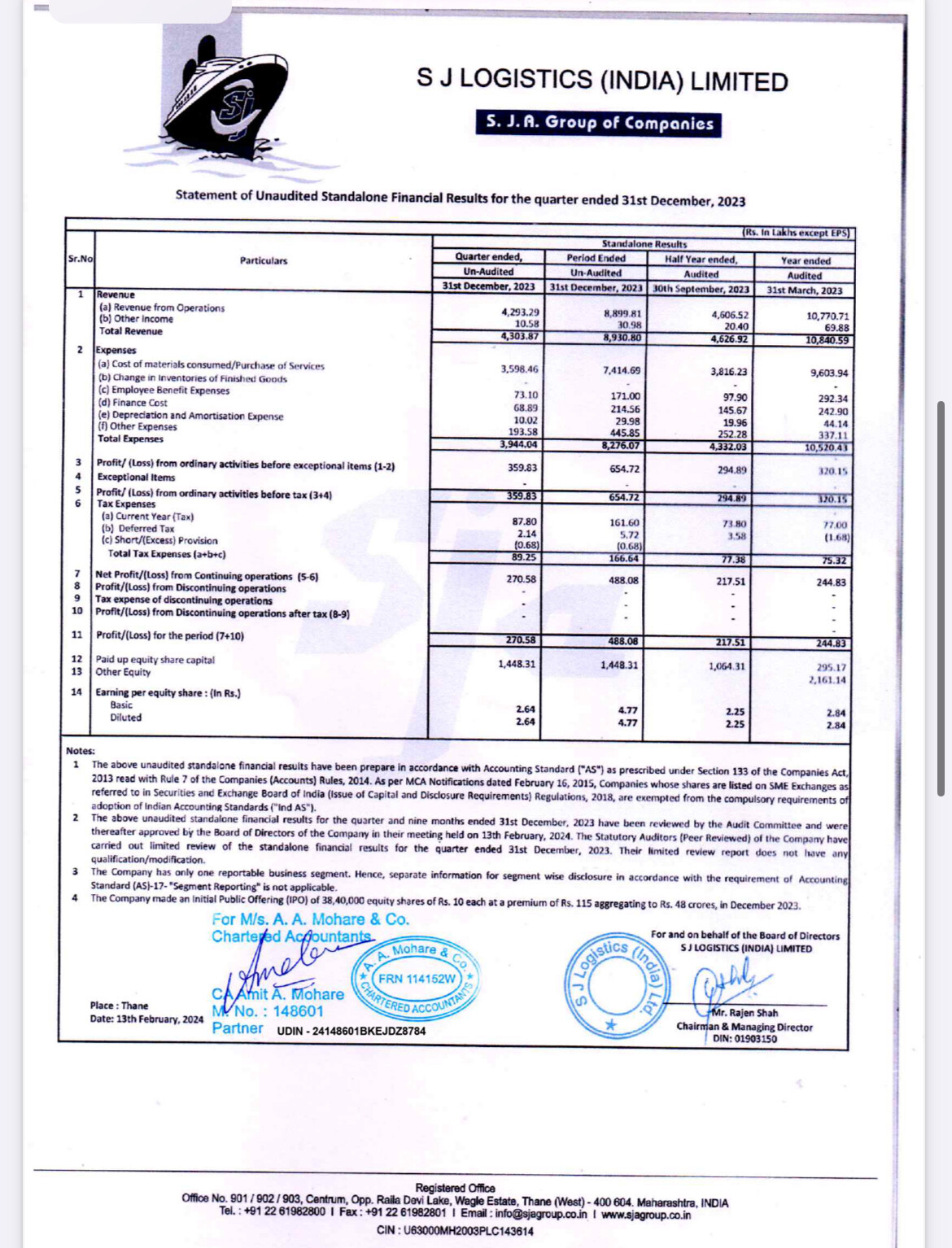

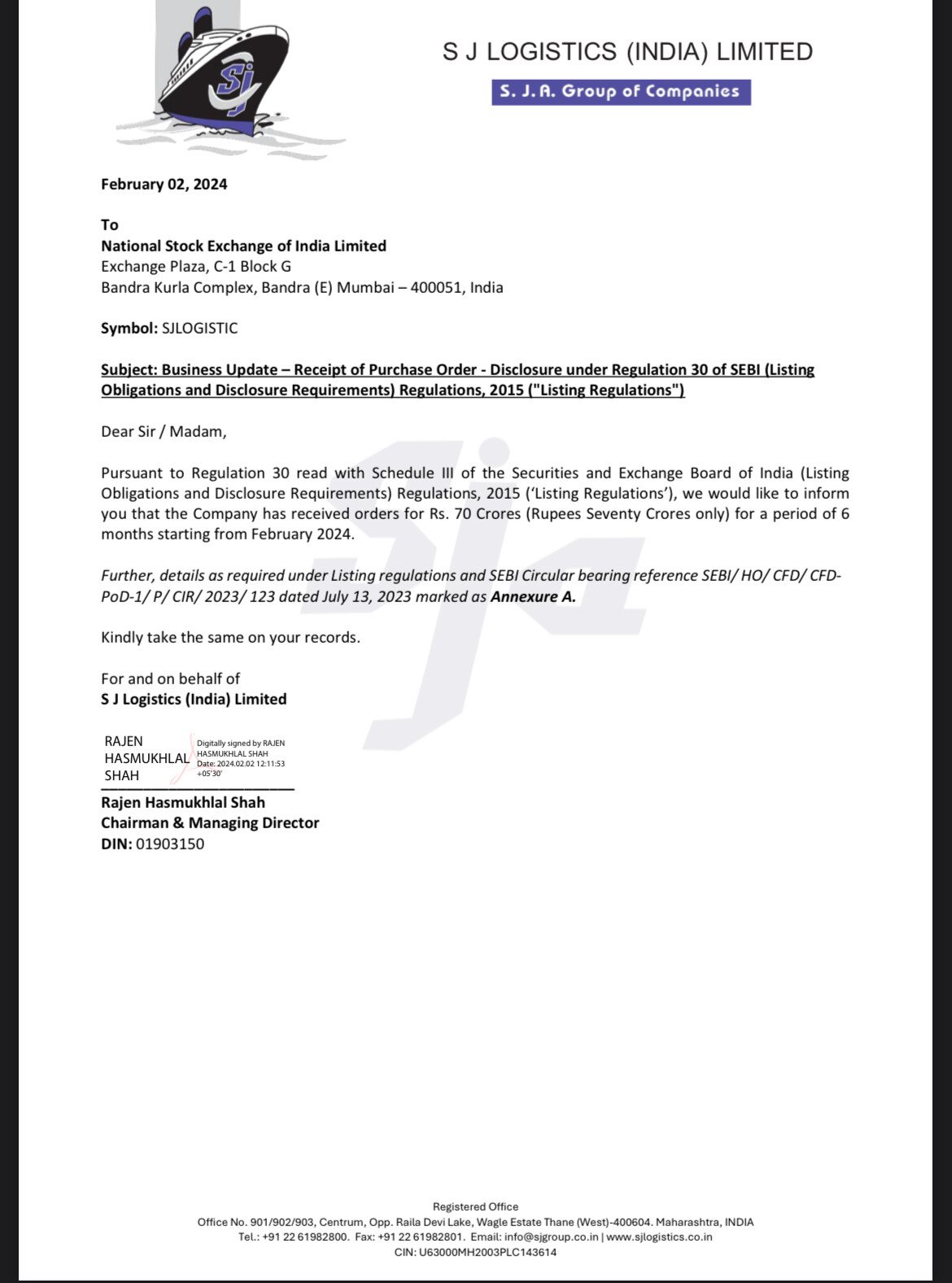

SJ Logisitics- Dark Horse (21-02-2024)

Company Analysis

S J Logistics– premier international logistics service provider, provides the services including freight forwarding, transportation, warehousing, Non-Vessel Operating Common Carrier & customs clearance.

Services Offered-

FCL Shipping

Project Cargo

Warehousing

Non-Vessel Operating Common Carrier

Inland Transportation

Door Delivery

Customs House Agent (Across borders)

Air Freight

LCL (less than a container load and describes sea shipping for cargo loads not large)

Major Focus on Project Cargo-The project cargos they have transported majorly includes earth moving equipment, transmission towers, ODC & break-bulk cargo and also undertake ODC (Over Dimension Cargo) which is out-gauge cargo that requires special handling, low bed trailer transportation

Major Clients-

Skipper- (Solid growth in numbers, FYI)

SW Solar

Areva T&D

Transrail

Sterlite

Company does repayment of loan amount and looking for expansion plans.

Recent Results- Solid Numbers are posted as 1 year PAT is achieved in 1 quarter…

Recently got order worth 70 cr

Key Risk Factors—

Breakdown, mishaps or accidents could result in a loss or slowdown in operations

They don’t have Custom House Agent license.

Their logistic and freight business is largely dependent on export of yarn and yarn commodities

DYDD, Study at your own in depth.

3B Blackbio DX Ltd (21-02-2024)

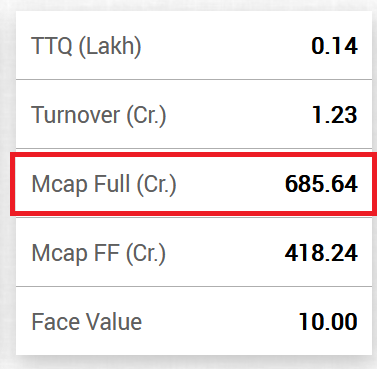

Couple of other things that are incorrect on the BSE website:

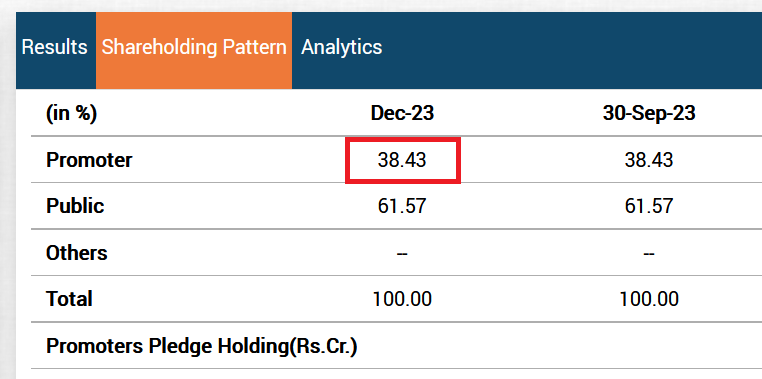

1/ Shareholding: promoter holding should be ~41% post amalgamation.

2/ Market Cap is incorrect: it doesn’t reflect the effect of amalgamation correctly – based on today’s price of 913 it shows a mcap of 685 CR. I believe it should be 815 CR instead (i.e., 685 * (75/89)) because the number of shares should have increased from 75L to 89L post amalgamation

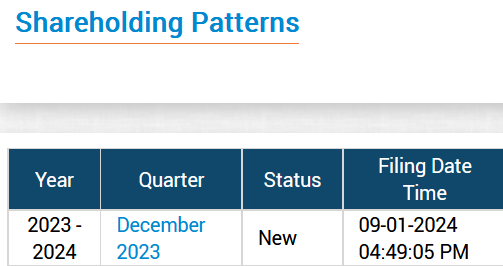

The amalgamation formalities completed in Dec’23 so I am not sure why it didn’t reflect in BSE’s shareholding pattern data which was published on Jan 9th 2024:

Shivalik Bimetal Controls Ltd (SBCL) (21-02-2024)

Any indications when will growth start again?

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (21-02-2024)

(post deleted by author)

Shivalik Bimetal Controls Ltd (SBCL) (21-02-2024)

Hi Friends,

I see promoters remuneration is in higher side compared to other big companies

Does this is normal,please educate me…Thank you

Sanghvi Movers (21-02-2024)

Nicely put!

Apart from the missing EPC piece, one other angle imho is cash profits.

(Disc: not a valuation or accounting expert, could be wrong, feel free to correct) –

Cranes have useful life of 35-40+ years. Depreciation in P&L is pretty aggressive. Therefore, if we don’t use cash to value this company, we will be undervaluing it.

Earnings power value

What is the static value of this business assuming no change (no growth, no cyclicality, persistent demand)?

Cash profit / WACC = 370/13% = ~2800cr

Enterprise value is around 5000cr…

The difference can be explained by growth expectations of market. However, we need to check if growth is value accretive or diminutive.

Value of growth

Someone in one of the above posts calculated Return on incremental CAPEX. Using similar method:

Yield on new cranes (more expensive): 1.7-1.8% (20% annually, payback period of 5 years w/out accounting for OPEX)

Revs to cash conversion: ~55% (based on latest PPT)

Post-tax return on incremental capex = 20% annual yield for new crane * 55% = ~11%

Cost of borrowing = ~9%

Assuming new capex will be funded by debt, growth looks marginally value accretive (11%>9%)

However, mgmt. indicated that they will be conservative wrt. Debt to Equity ratio (0.3) unlike past cycles that could set a ceiling for growth

Return on Invested Capital (proxy for ROE for such companies)

~370cr cash profit capability on current gross block; based on Q3 PPT

~2500cr gross block (Q2 transcript 2485 + some addition in Q3; 90% useful)

ROIC = cash profit / useful gross block = 370/2500 = ~15%

WACC could be close to 12-13%, marginally value accretive (15%>13%)

Yields

Mgmt. has indicated that 2.5-2.6 may not be achievable now, but they are confident of ~2. This may be a drag on valuation in long term

Tying it all

Since the value of growth is only marginally accretive, it cannot itself explain the huge gap between EV (~5000cr) and EPV (~2800cr). Looks like the rest of the growth baked in is EPC based (as per market).

On the surface, looks tightly valued or may be overvalued, especially if cyclicality of core biz is taken into consideration. However, the expectations around EPC biz could be providing some stability into valuations, not sure. Need some estimates around EPC valuation to put the final brick in the puzzle. Need help with that, thanks.

Disc: Tracking position, Evaluating

Shivalik Bimetal Controls Ltd (SBCL) (21-02-2024)

There are many end applications where SBCL products are used. Can anyone tell if it is a small or big company. Those who use Shivalik products

Lazycap’s Portfolio – Feedback (21-02-2024)

Update

Exhausted all the cash for now, built up HDFC Bank to 11% on cost basis with Avg price @1390 levels. Also added PVRINOX today with 7-8% allocation on cost basis with 1390 avg as well (Used up all the cash to buy it in a sense)

Rational for adding PVR is beaten down in my view with good risk reward, could go wrong. In expansion mode, most of the capex is front ended. ROCE might improve going ahead if new screens start yielding results. It could be a good bet from a very long term point of view not sure how long I will hold. Easily available & reasonable bet in current market for me at the moment