Posts in category Value Pickr

Avanti Feeds (21-02-2024)

This is exactly why I have never gone full throttle on the company. I feel it always get squished between 2 more powerful forces. I do not expect anything from Govt anyway (whatever comes will most likely be short term) and increasing feed prices would push farmers to move to fish farming. Pretty difficult situation in my opinion. I still have hopes tied to revival in the sector, let’s see.

Invested.

Avanti Feeds (21-02-2024)

This is exactly why I have never gone full throttle on the company. I feel it always get squished between 2 more powerful forces. I do not expect anything from Govt anyway (whatever comes will most likely be short term) and increasing feed prices would push farmers to move to fish farming. Pretty difficult situation in my opinion. I still have hopes tied to revival in the sector, let’s see.

Invested.

Cupid Ltd – Helping the world play safe! (21-02-2024)

Did anybody attend today’s EGM? I logged in but was able to only see the speakers and could not hear anything, as if everyone was on mute. Was anybody able to hear the proceedings?

Cupid Ltd – Helping the world play safe! (21-02-2024)

Did anybody attend today’s EGM? I logged in but was able to only see the speakers and could not hear anything, as if everyone was on mute. Was anybody able to hear the proceedings?

Medi Assist Healthcare Services Limited (21-02-2024)

I would see this company in a different view. Majority are seeing it as proxy to Indian health Insurance sector. I would say, it is rather proxy to Indian corporate sector.

Rationale –

After covid, people understood & taking separate health insurance policy which reflects sharp rise in Health insurance business etc. But here Medi Assist would not gain much (because majority of private Insurance company have In-house claim settlement team particularly for individual policy).

However, for group insurance business is mainly sources throguh TPA & also majority of PSU individual policy also.

So, as India will have more Organized sectors – They will opt for Group Insurance for their employees which will be source through TPA. So more & more Organized sector jobs (In any sector – IT, BFSI etc.) will lead to more business for such TPA indirectly.

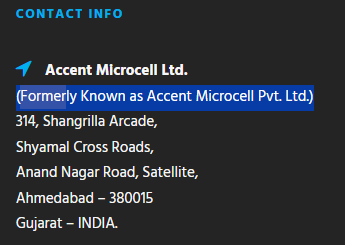

Accent Microcell Limited – A Niche Microcap with some puddles (21-02-2024)

The promoter is into the same business through Unlisted entity Accent Microcell Pvt. Ltd. (red flag) which is mentioned as competitor for MCC in RHP à what’s the need for the same?

Accent Microcell Pvt. Ltd seems to be a former name of this same public listed entity. After reading your analysis, I found it to be a major red flag so I tried to dig into their website for any info on this, in the career section of the website “Career – Accent Microcell Ltd.”, I found in the contact info – “(Formerly Known as Accent Microcell Pvt. Ltd.)” . So the report which you referred from while listing competitors may have made the mistake of referring some old database and hence listed it as a competitor (at-least that’s what I am thinking).

Disc : Taken some initial positions

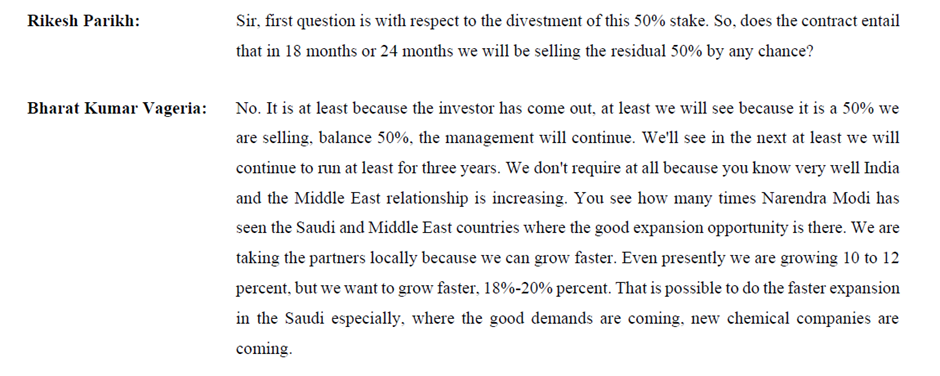

Time technoplast (21-02-2024)

Overall the management is not consistent. I have seen previously they used to over promise and under deliver. In my thesis, I keep that in mind. Invested from 75 levels. I think they have a good product opportunity but are not encashing it fullly.

Time technoplast (21-02-2024)

I don’t know if I am interpreting this correctly but…

Besides selling only 50 % instead of the earlier announced 80, and retaining management control Mr. Vageria now says this situation will remain for 3 years at least and then “We’ll see…”. The buyer is referred to as “investor” meaning one having only financial interest and not strategic. Mr. Vageria dwells at length on increasing potential in the region. Even with other overseas territories, Mr. Vageria has said (elsewhere) he is ‘not desperate to sell’. Overall, the language seems to indicate they will go slow on the overseas divestment plans, do it selectively while retaining management control and consolidating the numbers into TTL. If I remember correctly, earlier the stated intent was to sell 80 % and focus on “core business in India”, implying forget overseas. That may no longer be the case now.

Any views?