#Midhani: Likely involved in supplying superalloys and titanium alloys for various platforms.

![]() Solar Industries & Premier Explosives: Potential suppliers of propellants for loitering munitions.

Solar Industries & Premier Explosives: Potential suppliers of propellants for loitering munitions.

Timeline: Contracts expected within 9-12 months.

#Midhani: Likely involved in supplying superalloys and titanium alloys for various platforms.

![]() Solar Industries & Premier Explosives: Potential suppliers of propellants for loitering munitions.

Solar Industries & Premier Explosives: Potential suppliers of propellants for loitering munitions.

Timeline: Contracts expected within 9-12 months.

As per latest concall, Management is expecting a high R&D expense in Q4. Paracetomol & Metformin Sales Price declining. They are keeping the margin but topline is reducing for top products. New facility Commercialization maybe in FY26. They are introducing new Products (FD) in US & applying for approvals in Europe.

Management is not giving guidance. They are talking about a lot of Capex and I can not get a clear picture on how & when it will improve revenue.

I have a small position now but do not have a clarity to increase investment. Any Opinions on how you are tracking thier performance?

Do check Rane Madras. Have updated the thread

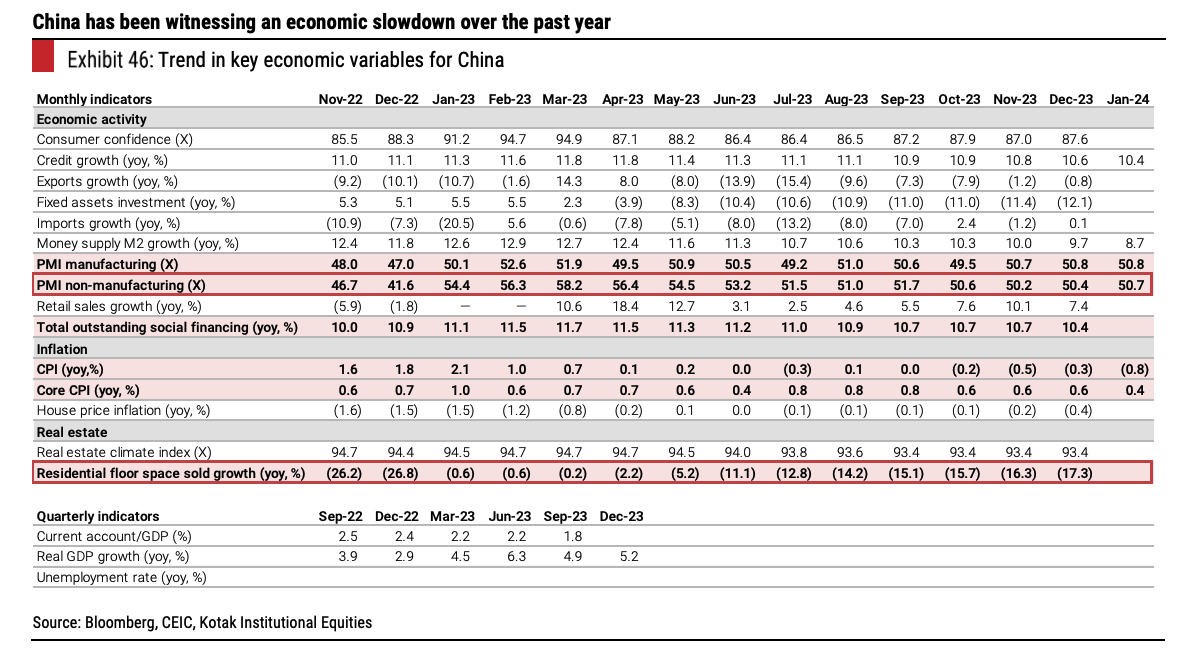

Fitch Downgrades UPL Corp to ‘BB+’; Outlook Negative

UPL’s weak performance mainly reflects sustained pressure from overcapacity in China.

UPL expects channel destocking, which has affected demand, to subside by 1HFY25. However, the outlook for capacity in China is more uncertain. We assume UPL’s product prices and margins to rise meaningfully from 4QFY24 on supply rationalisation in China in response to weak profitability. However, there is risk that the glut will persist for several years and constrain UPL’s EBITDA margin improvement.

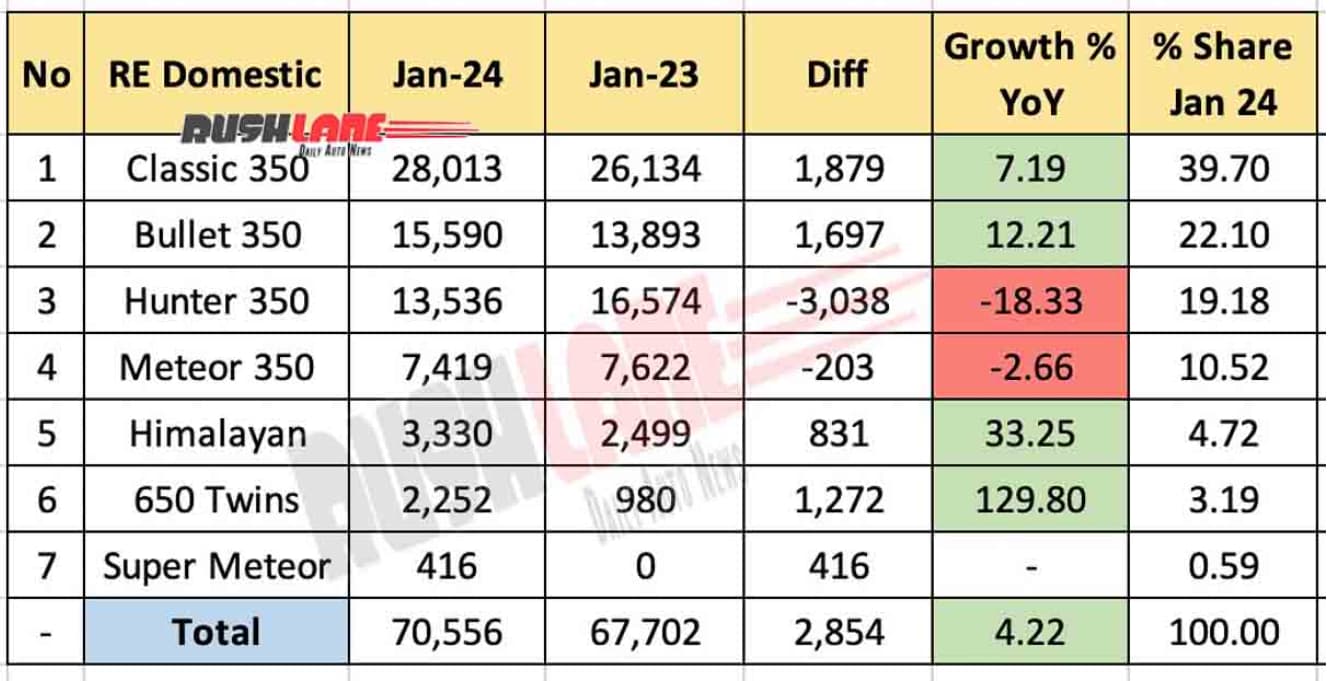

Good to see 650 cc segment growing .Its important to get good numbers in 650cc and 450cc because 350 segment now has cutthroat competition with all major manufacturers putting up a good show.

The way the market moves, and I am new to these things, it seems it ‘discovers’ a sector, and then moves from top to bottom companies. Within the sectors too, it searches for sub-sectors.

So, within the PSU rally, first it discovered Railways, Banks, Power, and Defence. Not necessarily in the same order. And many of them were really cheap. But to me now, the markets have a tendency of going bonkers. IRFC going 4 or more times in six months. SJVN jumping from 40 to 146 in the same time, to cite just a few examples, showed this discovery. The maness is also reflected in BHEL ROCE: 3.33 % and ROE: 1.70 %, being market’s darling.

I have tried to discover sane areas within the market’s frenzy, and here the Oil PSUs fit in. Chennai Petro is still at 4.8 PE. ROCE is 45.5% and ROE is 77.9 %.

In the case of OIL, P/E is 9.14. ROCE is 25.4%, ROE is 25.2 %.

PE of RVNL is already 38.6. P/E of IRFC is 34.6.

So, clearly, now the Railway PSUs are expensive, though today again there is a move in the RVNL etc. The Oil PSUs, and I have mentioned only two, are clearly cheap. There are many negative factors, like regulation, in the case of PSUs, but to me they appear cheaper despite these factors.

SKIPPER-RE-BE show in Console. However, nothing has been called for as yet – no intimation from the bank.

Anyone else have updates?