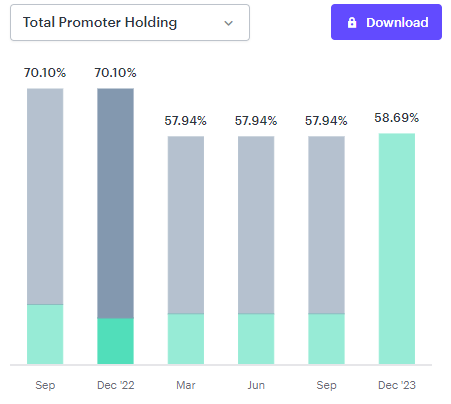

My initial impression was that the company is doing too many acquisitions in a short span of time. But looks like there is a very clear strategy of seismic shift of focus towards mixing solutions, coz it opens up more avenues for the firm. I had a question on valuations – seems like there is a downwards trend in the stock since the last six months or so. Part reason is clearly the slowdown in mother industry for their largest revenue segment – chemical and pharma. Is there something else the market is factoring in?

Also – besides expanding avenues, is the focus on mixing solutions a part of managements plan to be less dependent on cyclicality in pharma and chemicals?

Expert views awaited – cheers!

Posts in category Value Pickr

GMM Pfaudler: A safe way to play the Pharma/Chemical cycle (18-02-2024)

Companies with 20%+ growth guidance for next few years (18-02-2024)

Jyoti Resin and Adhesive – Company guided 25% CAGR growth for next 3 years as per their investor presentation https://euro7000.com/wp-content/uploads/Investor-Presentation-Q1FY24.pdf . Over the last 5 years, Company have grown at CAGR of 38%, 103%, 113% on Revenue, EBIDTA, PAT. They are number 2 in white glue(product Euro 7000). Not sure if any of you have used their product. Management is conservative and going into 1-2 new state every year. All ratios are excellent. ROCE 70%, ROE -50%, 0 debt, last 5 years sales growth > 50%, OPM 23%.

I am not sure why this stock keep going downward irrespective of good numbers and available at 25 PE for such high growth company. Is there anything I am missing/not seeing which market is seeing. Currently I have 2% allocation, but I want to make it to 6% as soon as stock moves to upward trajectory.

Companies with 20%+ growth guidance for next few years (18-02-2024)

Jyoti Resin and Adhesive – Company guided 25% CAGR growth for next 3 years as per their investor presentation https://euro7000.com/wp-content/uploads/Investor-Presentation-Q1FY24.pdf . Over the last 5 years, Company have grown at CAGR of 38%, 103%, 113% on Revenue, EBIDTA, PAT. They are number 2 in white glue(product Euro 7000). Not sure if any of you have used their product. Management is conservative and going into 1-2 new state every year. All ratios are excellent. ROCE 70%, ROE -50%, 0 debt, last 5 years sales growth > 50%, OPM 23%.

I am not sure why this stock keep going downward irrespective of good numbers and available at 25 PE for such high growth company. Is there anything I am missing/not seeing which market is seeing. Currently I have 2% allocation, but I want to make it to 6% as soon as stock moves to upward trajectory.

SJVN Ltd – Hydroelectric power (18-02-2024)

I read in May 2019 concall that SJVN had installed capacity of 2015 MW. It planned to increase it to 5000 MW by 2023. However, as per the latest concall, its installed capacity is 2227 MW only which is very slight increase to its 2019 capacity. In the last concall also, ambitious targets (25000 MW by 2030) have been given.

Could someone please try to reconcile such staggering variance between ambitious goals and actual growth?

SJVN Ltd – Hydroelectric power (18-02-2024)

I read in May 2019 concall that SJVN had installed capacity of 2015 MW. It planned to increase it to 5000 MW by 2023. However, as per the latest concall, its installed capacity is 2227 MW only which is very slight increase to its 2019 capacity. In the last concall also, ambitious targets (25000 MW by 2030) have been given.

Could someone please try to reconcile such staggering variance between ambitious goals and actual growth?

Jindal Stainless (Hisar) (18-02-2024)

Good News

Promoters unpledged Fully

Jindal Stainless (Hisar) (18-02-2024)

Good News

Promoters unpledged Fully

Atirek portfolio (18-02-2024)

I have similar opinion about the book. Almost finished Section 1. IMHO the beginning of the book was dull with two many statements and quotes but no case studies/data supporting those. So far I have liked Chapter 3 where author discusses biotech business with analogy from Peter Thiel’s book. This chapter actually discusses some case studies and business models. Based on my experience so far, I am keep my expectations low.

Yes, the book has very high PE ![]()

Atirek portfolio (18-02-2024)

I have similar opinion about the book. Almost finished Section 1. IMHO the beginning of the book was dull with two many statements and quotes but no case studies/data supporting those. So far I have liked Chapter 3 where author discusses biotech business with analogy from Peter Thiel’s book. This chapter actually discusses some case studies and business models. Based on my experience so far, I am keep my expectations low.

Yes, the book has very high PE ![]()

HealthCare Global – the value unlocking story (18-02-2024)

2024 Feb – Q3FY24 Concall:

Floods in Chennai & Strategic decision of coming out of ‘shop-in-shop’ model led to a scale-back of operations in M S Ramaiah Bengaluru, affected revenue growth by 2-3% and also EBITDA by 30 bps for the quarter

Decline in Q-o-Q PAT is on account of depreciation for acquisitions of Nagpur and Indore

Q3 is generally a seasonally muted quarter

Overall ARPROB is increased to 42.8K INR, a15% Y-o-Y growth

Centers of excellence delivers 30% margins and ARPOB is above 70K INR

Increased 59 beds during Q3

Current total no. beds: 2000, occupancy at 65-70%

Adding a new 100-bedded hospital, a comprehensive cancer care in North Bangalore, Capital outlay about 90Crs, expected to be operational in 15-18 months

Going to add 350 beds over next 3 yrs with capex of 130 Cr (48Cr is already spent)

Net debt stood at INR367 crores as on Dec’23. Very comfortable with the current debt levels and project a better cash flow in the coming quarter

Decided to divest Milann division, will be done at max. value possible, more info to come

No comments made on CVC exit plans (no denial, at least)

Moving to a new facility in Ahmedabad due to capacity constraints

May not achieve earlier guidance of 20% Ebidta margin by Q1, Q2 FY25, due to drawdown coming from Indore acquisition, Whitefield project being functional and also increasing Govt. functions.

Generally, need for expansion arises once occupancy reaches late 70%, to keep remaining beds for day care.

Expecting ARPOB to grow at 5-7% Y-o-Y in coming years, lever are combination of high-end treatment, faster turnaround, lower ALOS.

Aiming to grow higher than market which is at 10-11%

List item