Very well articulated Ayush .As usual a great multibagger find by you !![]()

Posts in category Value Pickr

NGL Fine-Chem (Animal Health + Human Health + Vet Formulations) (18-02-2024)

NGL Fine-Chem (Animal Health + Human Health + Vet Formulations) (18-02-2024)

Great research and insights .Please keep sharing !

Agree with what you said on adjacency .Anyway NGL strategy has been almost like “strengthen the core and grow more thru adjacency also ” .Rare to see such great allocator of Capital .Staggered capex of 140 cr thru internal accrual is an example (pay as you grow model type) .

Discl :Views may be biased bcos of my holding

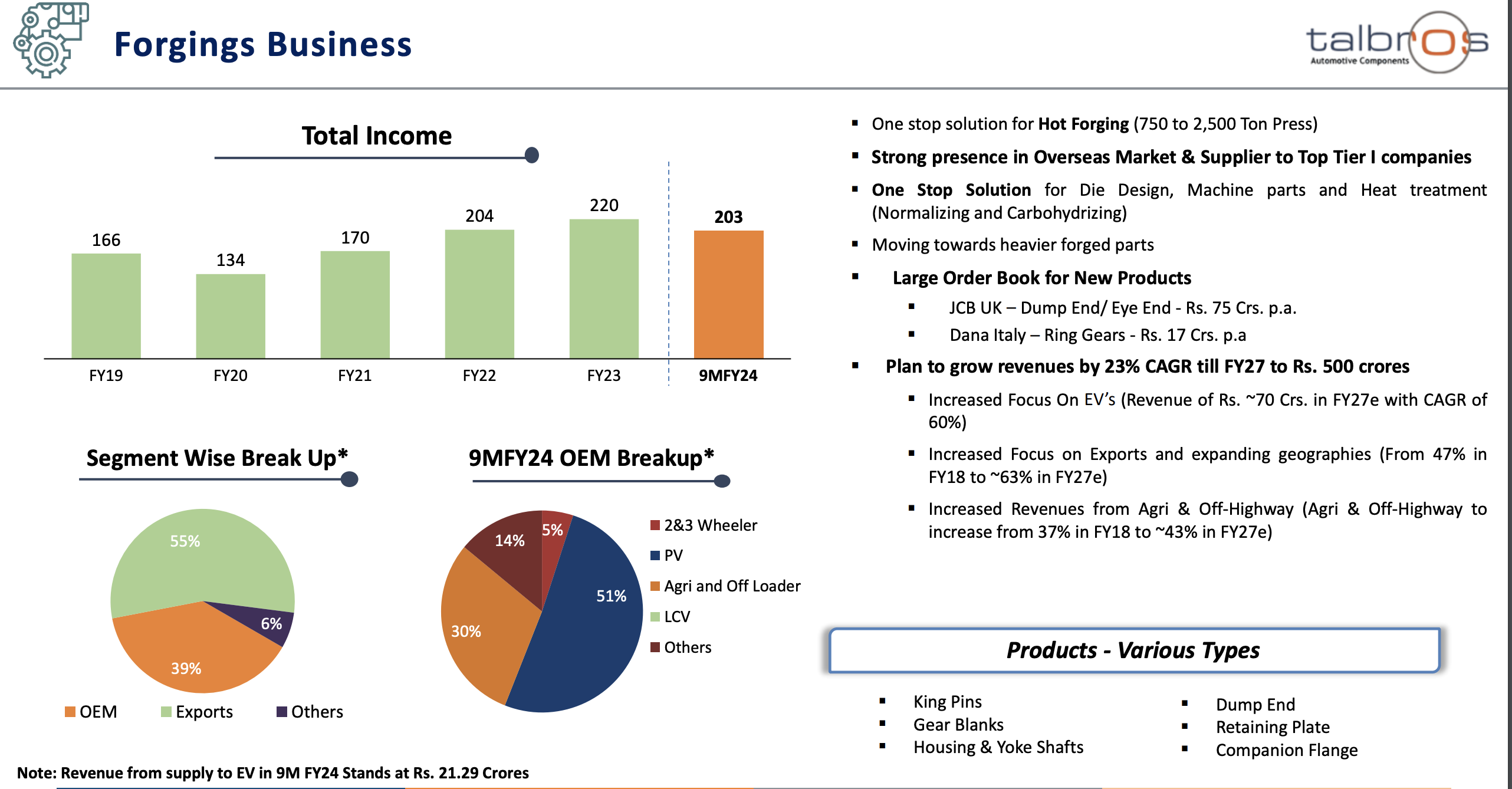

Talbros Automotive Components Limited (TACL) (18-02-2024)

They have given the breakup in the PPT how they will achieve 2200Cr on group level.

700 Cr from the Gasket business, 500 Cr from the Forgings business. Another 1000 Cr from the JVs where they have 50:50 partnership, so we can assume 500 Cr revenue from the JVs. So Talbros sales could go to 1700 Cr if they can deliver.

As they have guided for EBIDTA margin of 15-16%, if they achieve that, PAT margin can go as high as 11%. They have achieved 11.3% in last quarter. That gives us PAT of around 190 Cr.

I haven’t accounted for debt reduction, which can further add to the bottom-line.

If we take peers P/E, most of them are trading at 30+ PE. In best case scenario, if they get 30+ P/E, market cap could go as high as 5500Cr+. In worst case, it could still reach 2400-2500 Cr.

Atirek portfolio (18-02-2024)

I am writing it late than usual this month. Though today I found the time to write it down as writing helps in controlling my behaviour and knowing, why I took the certain decision in the past.

After we start writing regularly and updating the thesis against the company(I use samsung notes) we start seeing the benefits.

Completed the book Romancing with the Balance sheet.

Key learnings

- What is the operating leverage, financial leverage and how to calculate it?

- What difference between expenses and assets?

- What is the cost of funds?

- How to find the liquidity profile of the company?

- What is contribution margin?

It takes me nearly a month to 2 to complete a 300 page book as I read few pages everyday instead of reading all on one day.

Ordered the book by unseen value though I am not liking it. Still trying to read it.

Let us talk about losers in my portfolio.

Out of 8 stocks that I hold, 5 in Indian and 3 in US, I am in loss in Alibaba and Kama Holdings.

Loss Stock No 1 – Alibaba – Near to 15 percent loss

- Alibaba is one of the reasons I opened my US stocks account on Indmoney as I found it cheap near sub 100 level. Though I have mentioned it earlier, opening the US account brings in a lot of tax complications and I hate complications especially related to government entity like taxes.

- This is one of the reason I have been honestly filing my taxes and this year selected the new tax regime as it is more beneficial for me in terms of amount saved and less complications.

- Though as I have not incrementally put more money in the US stocks and as Alibaba has not given me any profit, hence it has become near to 2.5 percent of my net worth.

- One important thing I have observed is that all the breakout given by Alibaba fails as currently China is in bear market. Hence I am not sure whether to add the stocks on breakout works in bear market or not. Even in the book “how to make money in stocks by william o’neil”, it was written how the technicals might not work well in bear market. Hence bear market seems to be unknown territory. I sometimes use technicals for the entry in fundamentally strong stocks with tailwinds.

Loss Stock No 2 – Kama Holdings – Near to 7-8 percent loss

-

I have mentioned earlier, Kama Holdings I added first in my mother portfolio. As it started increasing, I added more which brought average price near to 2700. Later I added it my portfolio and last month, I added more which brought even my average price more than 2700. Thanks to the last month addition, it has become 4 percent of total portfolio. My last addition was at price 2590.

-

As it is falling in last few months, it seems that I might be trying to catch the falling knife. One of the reasons, I added it initially in my portfolio as on one day when I saw many stocks falling, the kama holdings was able to hold its price at near to 2800 and hence I started adding it as I thought it has a better relative strength. Other reason was that its parent company SRF has been holdings its price now for few years and I thought Kama holdings might be able to do the same. Also, there were initial fundamental triggers already present. Though as per SOIC, if we want to put money in falling knife, we should only do it after it has stabilises and hence I have stopped putting money in it and also one more reason is that it has already become 4 percent of my net worth.

-

The reason I selected the SRF vs other agrochemical companies was that because SRF is a market leader, its agrochemical business(more than 30 percent of business and more percentage of new capex is coming here) is not dependent upon china and hence less things to track.

-

One more reason is that stock market is a betting game until and unless good amount of real money flows to your account and it keeps growing like here in this case, Kama Holdings provides good dividend due to holding company leverage on dividend of the SRF.

Portfolio updates

Addition of more of Neuland in last month and recent run of in it has made it nearly 8.5 percent of my net worth at the current price level.

Added more of Kama holdings making it 4 percent of my networth at the buy price level.

Added few shares of NH also. As NH has crossed my comfortable PE level of 35, not adding it anymore now.

Other updates

Last month I was hoping that stock market might give a correction as many people were telling to come in cash and predicting a correction but again market keeps surprising everyone. I will keep holding more than 20 percent in fixed assests(gold and arbritage) just to limit my drawdown(to drawdown I can handle) and my requirements of funds in short term.

This is the first time I have asked questions in concalls this quarter(Q3FY24). I have asked one question in Protean, two questions in Neuland and one written question in NH concall.

There was reduction in the Intermediate count in api under commercialisation in Neuland QoQ even though it was noted in Q2FY24 concall that no patents will expire till 2030. I need to ask Neuland, how to understand this change.

Few things important was noted by Neuland in last concall

-

If it is a molecule which is already generic, right, if it is not in the patent. Then you could actually file an alternate source and get an approval within 1 to 2 years. However, if it is a molecule which is still in the clinic being tested on humans, then companies can easily add an additional source at that point, provided that it doesn’t delay their filing timeline.

-

But once they file, until they get the commercial approval, companies will not add an additional source unless there is a significant problem. Once it gets approved, then companies will add an additional source. But like I was saying earlier, that to take easily between 1 to 2 years based on the complexity of that molecule and in some cases, even go up to 5 years.

-

It is the first time I think they have given some kind of guidance –

Now as we look into our future from where we stand today, we have much better visibility of

our business. We expect it to grow at around approximately 20% annually over the next 4 to 5

years. As the quality and size of our business grows, we’re getting a better visibility for our

future.

We will continue to commercialize molecules over the next 1 to 3 year time frame. We continue

to create capacity, keep ramping up with specific molecules in mind. As it stands today, FY25

looks like it will be a year of modest growth with some normalization of margins and operating

expenses rise due to inflation and ongoing investments.

Beyond FY25, which is FY26, FY27 and so on. We see a quicker growth on the back of both

existing molecules and new ones yet to be commercialized from the capacity that we’ll be

creating in FY ’25.

-

They said that FY24 has been a favourable year due to various factors like raw material prices, increase in utilisation of Unit 3, etc and hence might not be considered as a base year and also put doubts on sustainability of 30 percent margins.

-

GDS Specialty and CMS business margins are similar

-

Unit 3 utilisation at 57 percent.

-

For commercialised drug under patent – Typically, if you want to do that, I think it’s possible, the key

is, the complexity of the process, not just for the API, but for the finished dosage. And also the

regulatory strategy, depending on how many countries that drug has been filed in. And

depending on the situation, it could probably take a minimum maybe 2 years and maybe it can

take even 5 years.

In short if any company want to add a new supplier(considering the new supplier has already FDA approved facility) for their commercialised molecule under patent then there needs to be

- tech transfer(takes few months atleast)

- raw material supply chain security for the API

- supplier research plus the validation by the pharma company(takes few months atleast)

- a regulatory filing with the new source to prove that the API made by new supplier is equal to the old supplier.(takes few months atleast and depends upon in how many countries the molecule has been commercialised)

- Contracts obligations by existing supplier(Neuland hinted at it in the concall)

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (18-02-2024)

Raw material for polylactic acid is Sugar. Wouldn’t this be vulnerable to govt directions to restrict sugar usage in case of production shortfall…thus risking the project in such a period.

Raman’s Portfolio – Review Appriciated (18-02-2024)

Current update on portfolio –

Sold Ion exchange – recent promotor’s selling made me uncomfortable, (already low promoter holding). Though it is a good business. May enter again in future.

Added tracking position in following stocks –

Riba Textiles – Wanted to enter into textile sector which seems to be breaking out (most of the stocks entered into stage 2). A microcap with good brand, Very low valuation (7 PE). Good profit growth in Q3.

DMR Hydro – Infra play. Just taking bet on a very small microcap into growing infra sector. Promoter seems to be good with long aspirations. Nothing much info available.

Added some more Frog cellsat.

Rest of the Portfolio is same.

PayTM (One 97 Communications Ltd) (18-02-2024)

I have one question on merchant side UPI.

Let’s say I am merchant on Paytm and uses PayTM for business were I will be tracking all things. Does this have VPA like @paytm? and on soundbox if I change my bank account, as it will have new VPA then how it will affect soundbox QR?

I believe Soundbox QR code can remain same even though you change your account as paytm app will make that linkage but wanted to confirm.

Thanks!

Journey and Portfolio of a goal-based NEEV investor (18-02-2024)

As more or less confirmed by RBI in FAQ, scenario 1 should play out. I am almost sure that there is no salvation for paytm payment bank as tbh there is not much this bank doing other than acting as PSP for paytm and it was good idea as PayTM had reach ppl so ppl can take advantage of having account putting 2 lacs in FD (this is done in partnership in this case it was Indusind bank) in rural areas and it can’t lend so not much use of CASA. what is use of payment bank if you do not allow play it with different business modal like India post payment bank. To be sure, PayTM gave reasons for this action in terms of KYC loopholes. My gut feeling is also saying that disbursement number of PayTM somewhat made regulator uncomfortable and if you see since 2020 there are many new regulation, earlier RBI used to focus on deposits safety and aspects thereon but now it want to have A-Z tracking of 1 rupee that can’t be done without tracking payment provider so they had asked for PA license, PPI license and if you search online you will get number of new rules/regulations were launched – traditional banks operate in boundary so there is not much chance of accident so it will hurt most fintech player who play on edge but that’s what make boundary expansion – I do not think Bank can play role of innovator. UPI and Payment bank both was launched when Mr. Rajan was governor so you can get sense how it impact the industry who are the head of regulator. I can go on but I think i should stop now ![]() otherwise it will bore readers.

otherwise it will bore readers.

About PayTM specific, no option but to wait. At least we have light at end of tunnel as UPI will keep working.

Thanks!

Disc. Holding Paytm so may be biased.

BKasal’s Portfolio (18-02-2024)

Hi balaji, you started this thread in a good spirit to help new investors with your experience and learnings. Pls revive this thread and discuss about your screening criteria and studying business models. Also pls discuss about your recent readings etc.

Tracxn Technologies (18-02-2024)

Thanks for detailed note and appreciate your blog material. I have following questions

- is there any indication or metrics published on Tracxn customer satisfaction survey, whether their customer able to derive business value / outcome out of their subscription fee

- what is % of customer renewals or renewals revenue on their existing subscriptions say if it is for 1 year or 3 years?

- Is there any plan on fine tuning public LLM with their data like you spoke about ML is need of hour ? Are they hosting their platform on any hyperscalers or colo datacenters